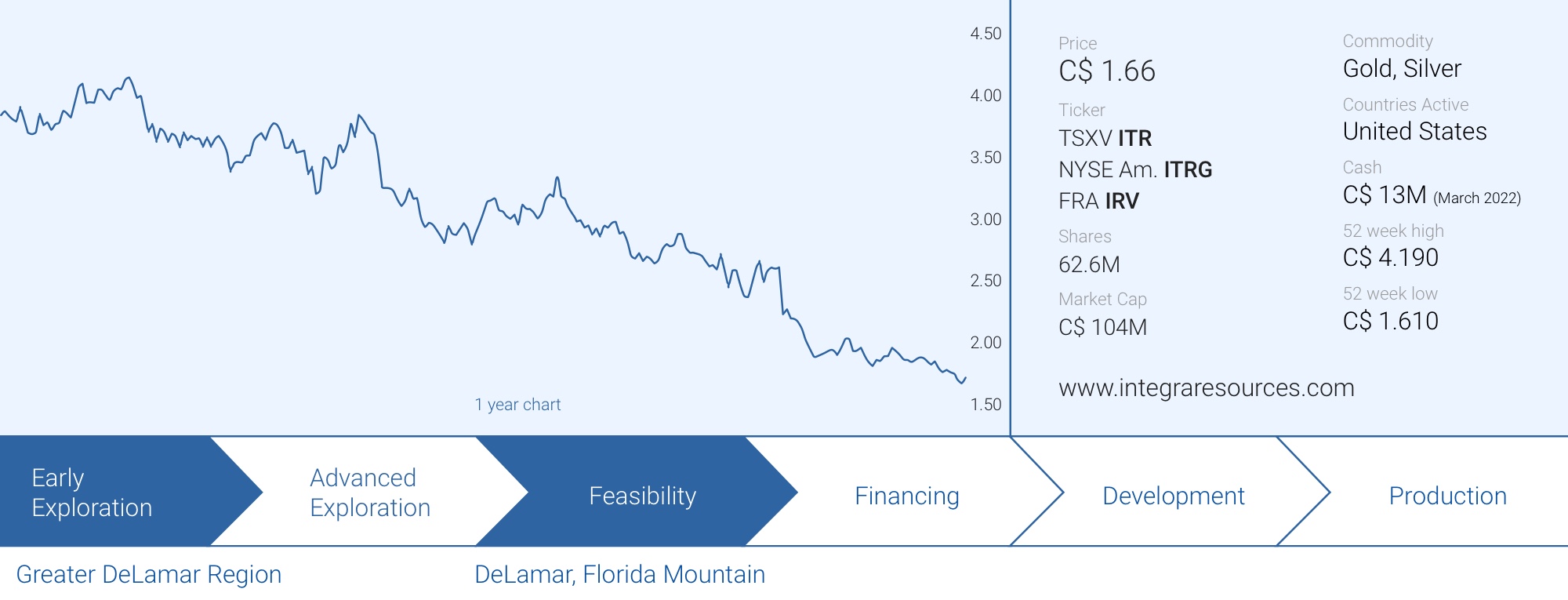

It has now been two months since Integra Resources (ITR.V, ITRG) released the results of its pre-feasibility study on the DeLamar project. After providing our ‘first glance’ opinion, we wanted to wait for the company to publish the entire technical report to see all the details.

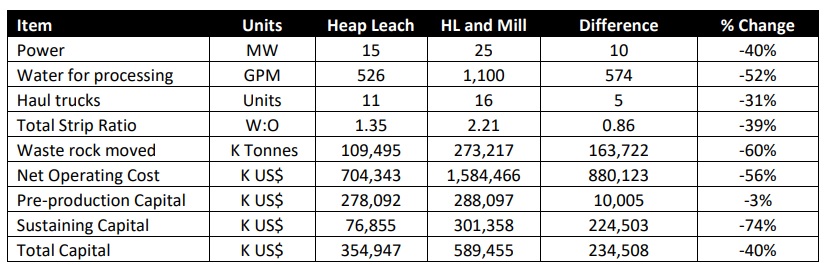

Our opinion hasn’t changed from a fundamental perspective: Integra released what appears to be a realistic study, taking all capex and opex inflation into account, and got punished for that. We think the market was predominantly disappointed with the value added by the milling scenario where a US$200M mill would only recover about 400,000 ounces of gold and 33 million ounces of silver. And let’s not sugarcoat it: in the current scenario that mill should not be built. When other companies use the word ‘optionality’, it usually means ‘it doesn’t work’ but in Integra’s case one needs to look at the project from the perspective of a non-revenue exploration company. A larger entity with more financial firepower likely would build a mill. But investors understandably got scared when they see a US$500M+ capex bill in the first three years of the mine life (consisting of the initial capex for the heap leach and the mill-related capex which was classified as sustaining capex).

But this is also where the market may be misinterpreting DeLamar: that mill does not *have* to be built and unless Integra A) can recover more gold and silver and/or B) the gold and silver price move up, we think the company and its investor base should focus on the heap leach phase of the project. That’s what we immediately said in February, and that’s an opinion we still stand behind.

That also is the set-up of this update report. We are applying the unconventional approach by just ‘forgetting’ about the mill scenario (for now) as the market is punishing Integra for it. While this completely changes the scope of the project and is a 90-degree turn from how DeLamar started out (as a heap leach oxide story with high-grade underground veins), it just makes the most sense to advance the heap leach phase, which is very economic with annual cash flows exceeding US$100M per year at the current spot prices, while Integra keeps working on the sulphide areas in the background. And looking at the company’s update published early this morning, that indeed seems to be the prioritized approach right now.

Damned if you don’t, damned if you do

Once a company completes a Preliminary Economic Assessment, the next logical step is completing a Pre-Feasibility Study. Integra Resources followed the normal course of action and did pretty much everything one could expect from a company in that specific phase: the heap leach scenario was refined and additional resources were added to the sulphide mine plan. But then two issues arose which partly derailed the milling phase of the project: first of all there was a last-minute curve ball related to the low gold recovery rates of the DeLamar sulphide which came in below 40% (but fortunately the recovery rate of the silver was approximately 75% which means the DeLamar rock is still viable) and thus resulted in a less efficient operation (and this is why the Albion process hopefully can add value to the project). And secondly, the impact of inflation was very tough to deal with.

Inflation is something all developers (or aspiring developers) will have to deal with so it doesn’t help to go sit in a corner and sulk. And Integra had the supreme misfortune of putting out the study in February, the very first PFS study of the year amongst the junior developers, at maybe what was the peak of an inflationary period. Since Integra’s release, other junior companies have also released updated economic studies, and we see cost increases all across the board. Indeed, increasing capital expenditures is now omnipresent, and other companies that recently released economic studies (Gold Standard Ventures, Montage Gold, Marathon Gold, …) all had to deal with the same impact. Steel prices are up by 25% while the cost for earthworks has increased by almost 70% mainly due to higher labor and fuel expenses.

While it’s understandable the market was underwhelmed, we think the report was one of the first released in this new inflationary environment and thus was potentially met with more of a reaction than expected (see above). As more Companies release (and build mines) in this environment, the effects of inflation on the industry will become more apparent. Though it is hard to compare the PEA (completed 2+ years ago) with a PFS (priced in this inflationary environment), not to mention the difference between a PFS (more advanced study) with a PEA (essentially a scoping study), investors reacted to the lower NPV5% at $1500 gold (US$203M versus US$466M) compared to the preliminary economic assessment in 2019. However, there are a few important distinctions to be made beyond the inflationary aspects.

So let’s forget about the mill scenario and only focus on the heap leach aspect of the project

While admittedly the headline results of the pre-feasibility study may not have met the expectations, ‘missing’ those expectations can be fully traced back to the milling scenario where a resource and reserve upgrade in combination with higher recoveries upon confirming the Albion process as a viable alternative could immediately drive the value, at sometime after the company is cash flowing with the heap leach.

But let’s take a step back. Let’s assume a scenario where Albion doesn’t work or is too expensive and where not a single additional ounce of gold can be added to the mine plan. An unlikely scenario given the huge exploration upside of the project, but let’s have a look at the heap leach only scenario and forget about the mill.

In that heap leach only scenario, Integra Resources is slated to produce 749,000 payable ounces of gold as well as 16.2 million payable ounces of silver. The initial capex indeed isn’t low at US$278M, again costed at the peak of inflation so perhaps some of these costs may come down a little bit, but the sustaining capex is low ($78M or just around $100/oz) and the all-in sustaining cost per ounce of gold is estimated at $570/oz.

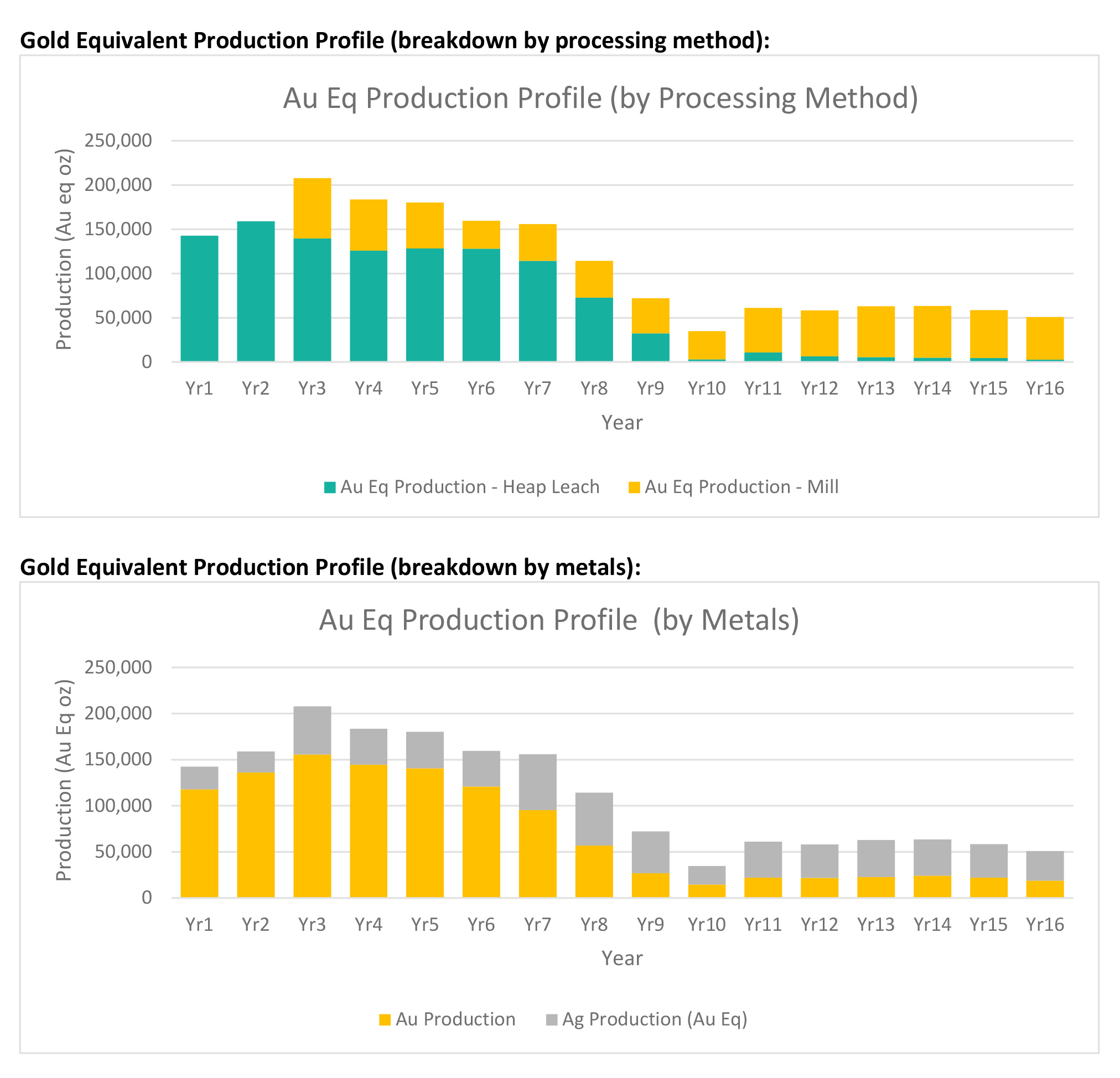

Integra Resources released a ‘heap leach only’ NPV and IRR in its update this morning, unveiling an after-tax NPV5% of US$314M and 33% using a gold price of $1700/oz and a silver price of $21.5/oz. At $1900 gold and $24 silver, this already increases to respectively US$435M and 43%. The breakdown of the heap leach component in the technical report also helps to figure out the exact production results. Keep in mind the table below shows the production results (ounces produced) and not the ‘payable’ production.

According to this heap leach scenario, the production rate will exceed 100,000 ounces of gold and around 2 million ounces of silver per year for a combined 125-130,000 oz AuEq for the first six years of the mine life and while the gold production drops really fast from Y7 on the silver production increases a little bit. Dividing the total amount of ounces gold-equivalent produced by the official 8 year mine life the average production rate is about 137,400 oz AuEq per year while the amount of payable ounces is approximately 119,000 per year. The anticipated AISC is US$570 per ounce of gold on a by-product basis (assuming the payable silver gets sold at an average price of $21.5. A higher silver price would further reduce the AISC per ounce of payable gold. If one would look at the DeLamar production schedule from a co-product basis, the AISC is estimated at just over US$810 per gold-equivalent ounce.

Trying to finance a mine with a mine life of just eight years poses its own challenges, Integra’s immediate focus should be on extending the mine life to keep the production at a rate of 100,000 ounces of gold (or a payable production of 119,000 ounces of gold-equivalent per year) for a longer period of time.That is not an issue that will have to be resolved right away as even just replenishing depleted ounces during the mine life is a valid strategy. And of course, there’s plenty of upside potential (including some low hanging fruit) on the property.

And another interesting feature is that a heap leach only mine should be easier and faster to permit. And once a heap leach mine is up and running, it may actually be easier to get the second phase of the project through the permitting phase as economics will start to play a role. The heap leach operation will create a few hundred direct jobs with several hundreds of indirect jobs being created as well. Once the permitting bodies see Integra (or a potential acquirer) are operating in a responsible manner, it should make subsequent permitting processes easier.

Additionally, the execution risk is lower: there tend to be less teething problems with a heap leach mine where a consistent ‘blanket’ of mineralization generally is less risky than high-grade underground systems with Pure Gold Mining being an excellent example of the latter. Managing the execution risk is important, and a specific focus on the heap leach portion of the project will help.

Where will the additional oxide-hosted ounces come from?

There are three potential sources for additional oxidized gold zones which could extend the mine life.

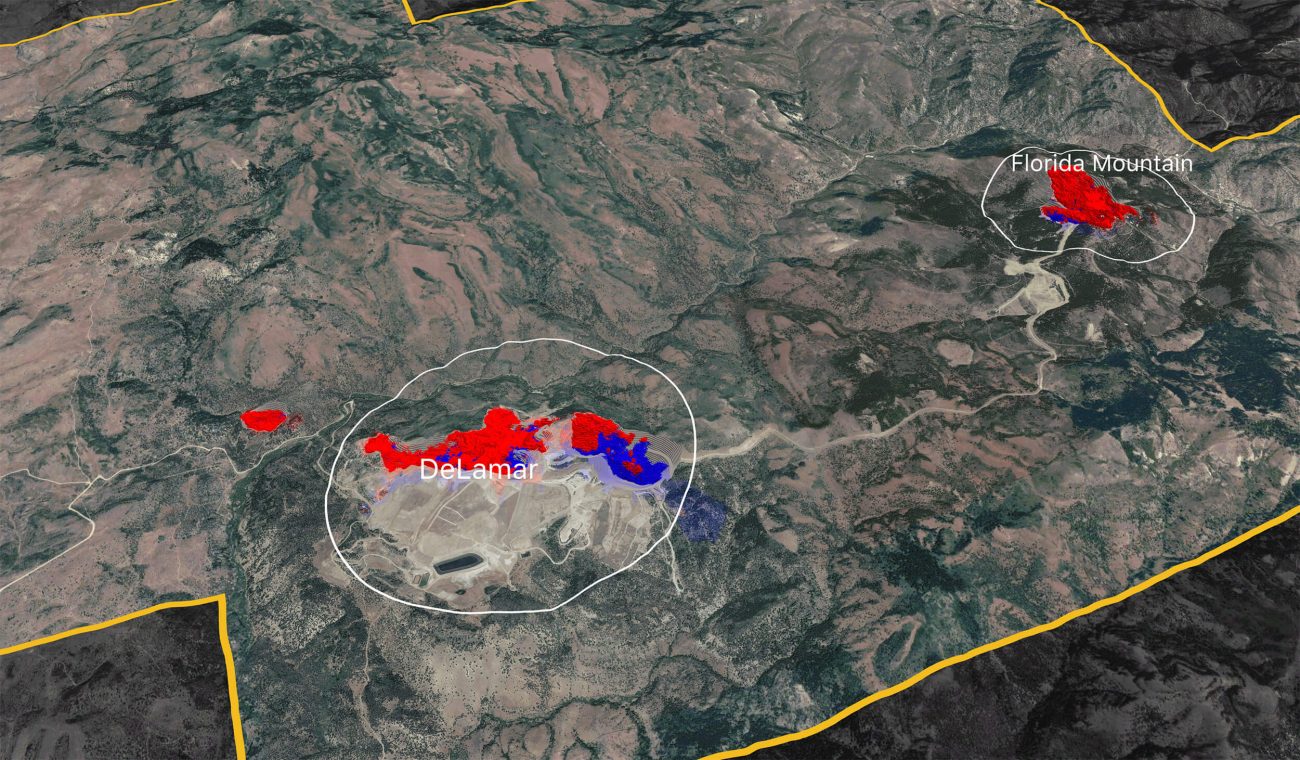

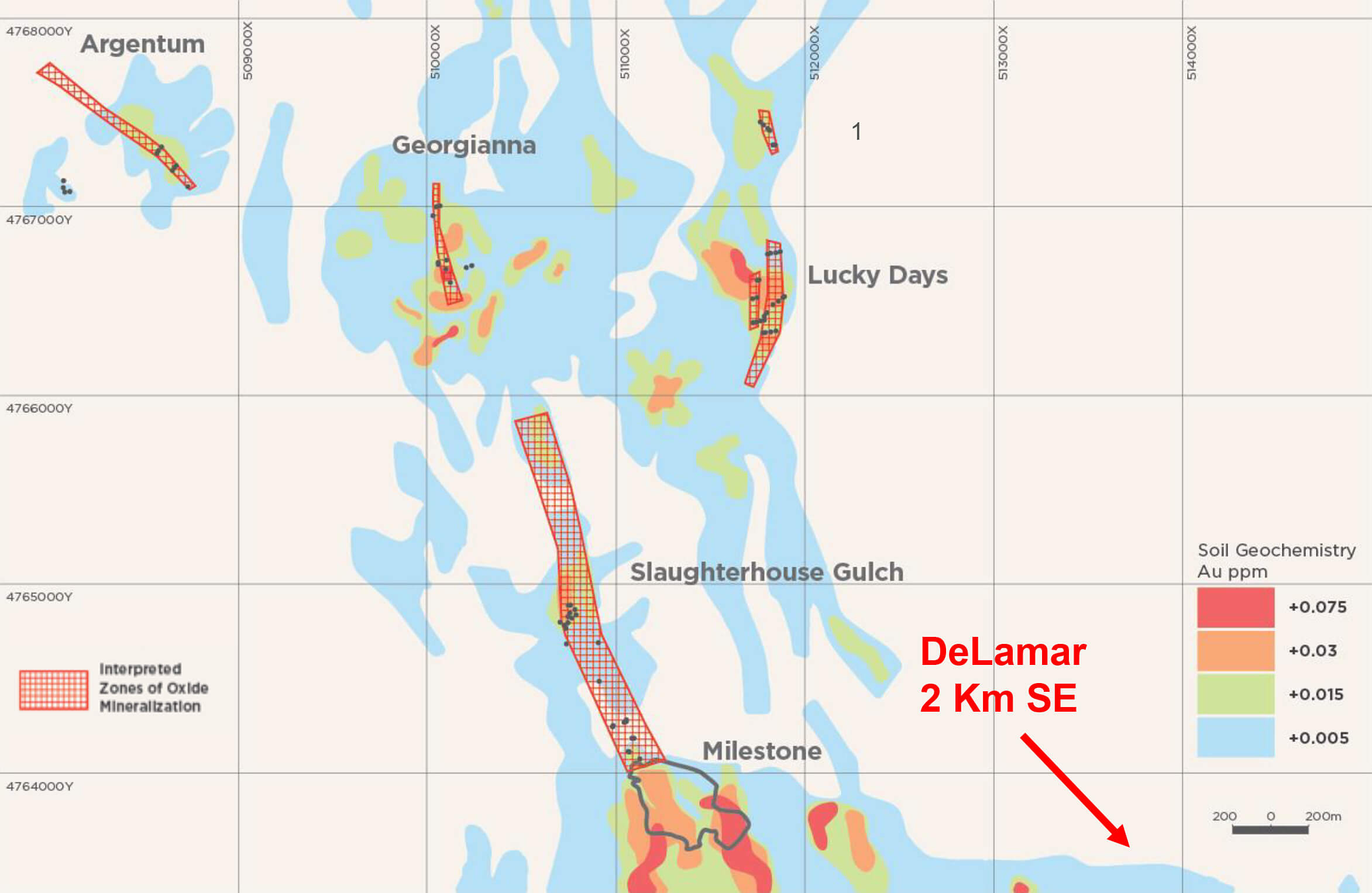

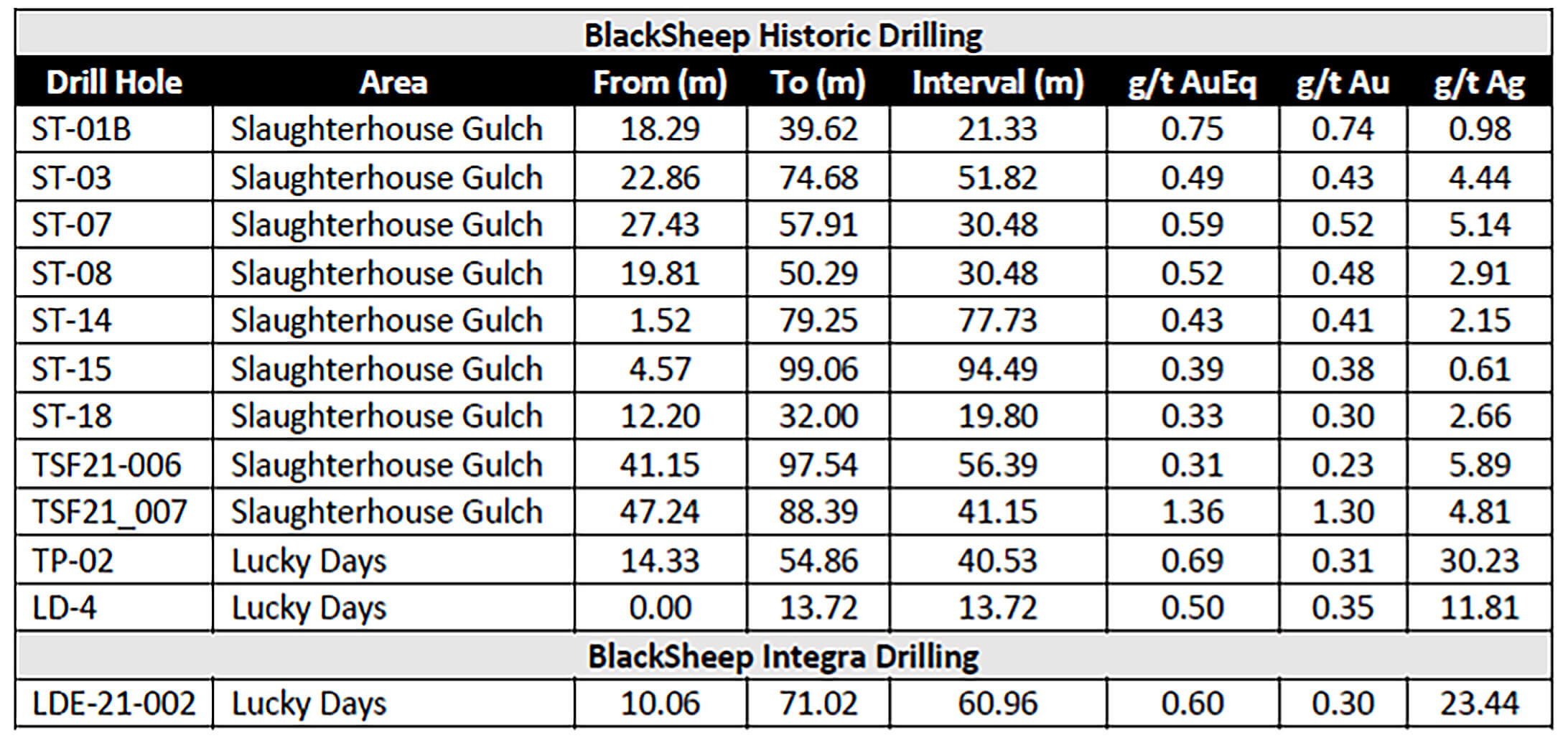

First of all, there’s the Blacksheep area, which is located within walking distance to the northwest from the planned DeLamar open pit. The image below shows the location of the oxide mineralization at the Blacksheep target and how Slaughterhouse Gulch may plan an important role here.

Historical Drilling has confirmed oxidized zones with gold mineralization very close to surface, especially in the Slaughterhouse Gulch area where it’s now starting to look like Integra will be able to rapidly build tonnes.

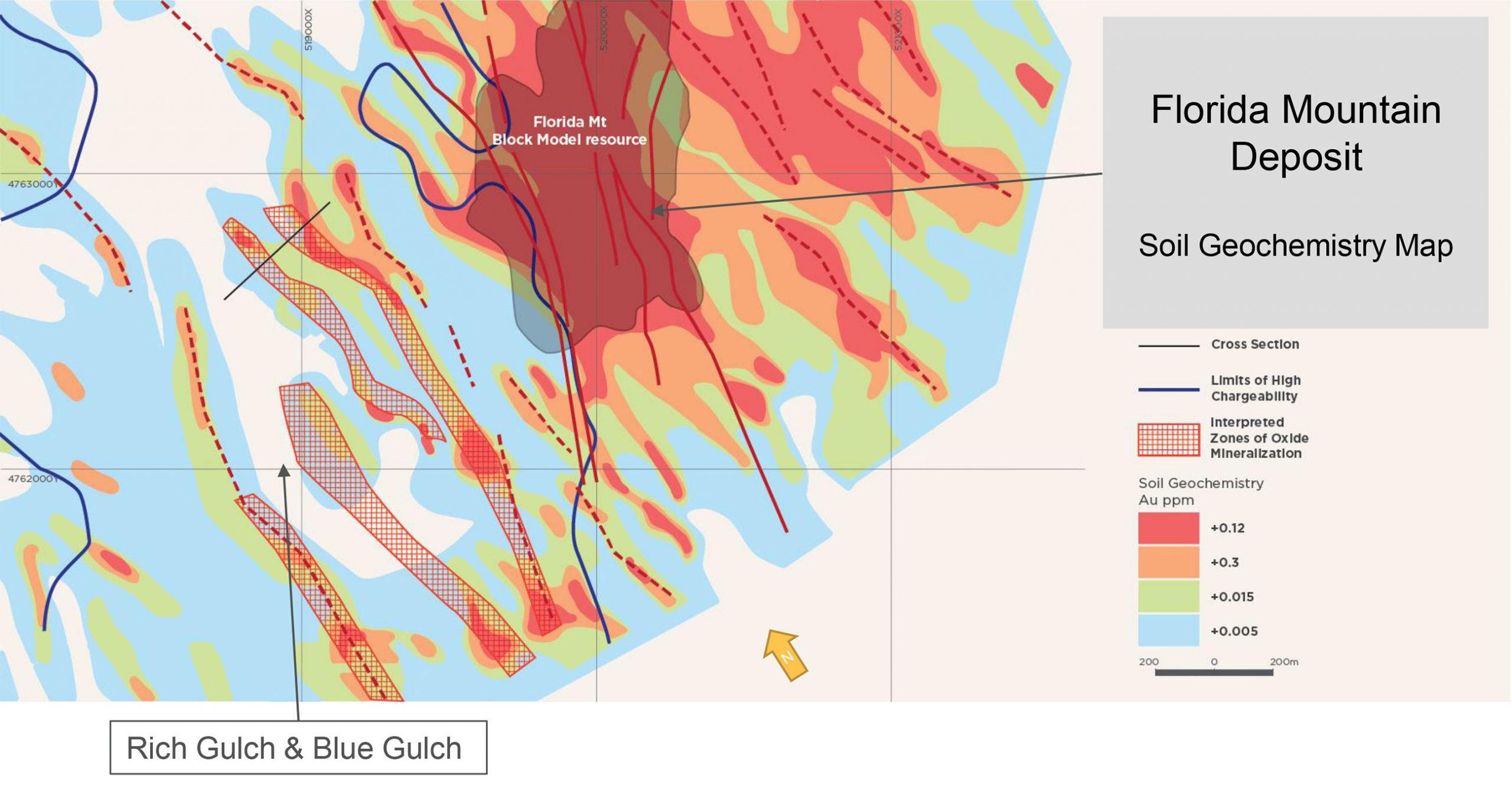

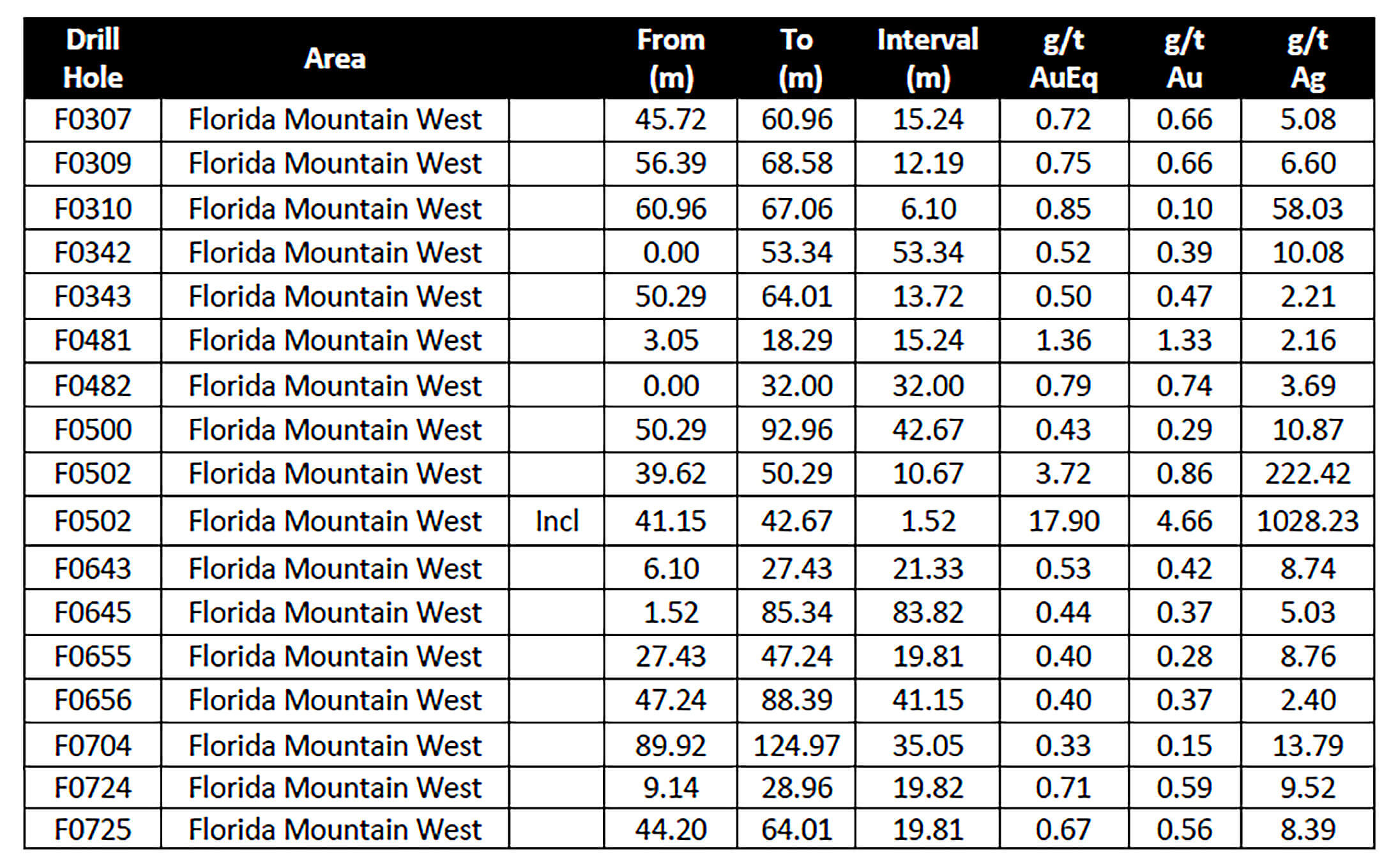

Additionally, at Florida Mountain there appears to be more low-hanging fruit as well based on a soil Geochem survey and historical drill results. Again, both the Blacksheep and Florida Mountain oxide targets are what they are: just ‘targets’ in this phase and more drilling will be needed to hopefully add a few hundred thousand ounces of gold (-equivalent) to the mine plan.

Historical drill results at this Florida Mountain West Zone have indeed encountered gold-bearing mineralization that would meet the cutoff grades for a traditional heap leach project.

A third area where Integra could source heap leachable material from are the old waste dumps from the historical mine operations by Kinross Gold (KGC, K.TO). This is also referenced in the technical report as a valid strategy to add ounces to the mine life. It is estimated (but yet to be confirmed) Kinross Gold excavated approximately 100 million tonnes of rock that were qualified as waste back in the day. As the gold price is higher and gold recovery techniques have improved, suddenly some of the tonnes that were previously thought to be waste now come into play again.

It appears there may be as much as 100 million tonnes of ‘waste’ on the DeLamar property, with an average grade of 0.30 g/t gold and 30 g/t silver. While this didn’t meet the cutoff grades back in the day, it would meet the cutoff grades for a heap leach operation in today’s reality. Of course it would be a pipedream to expect all 100 million tonnes to end up in a mine plan but even if we would just use 25%, or 25 million tonnes, an additional 241,000 ounces of gold and 24 million ounces of silver would be placed on the leach pad, equating to 2 years of mine life at a minimum. Note: in yesterday’s press release, Integra mentions about 60 million tonnes could be amenable for heap leach processing methods so we feel rather comfortable using 25 million tonnes (or 40% of that ballpark number) and we may very well be surprised to the upside. And as a rule of thumb: every additional 12.8 million tonnes that could get added to the mine plan extend the mine life by another year. So if for instance all 60 million tonnes could be added to a mine plan, the heap leach mine life would immediately be extended by five years.

Assuming the recovery rates are similar to what Integra outlined in its pre-feasibility study (we’ll use 72% for gold and 39% for silver), this would result in the recovery of an additional 174,000 ounces of gold and 9.5 million ounces of silver. The vast majority of these ounces should be payable resulting in an increase of 170,000 payable ounces of gold and just around 9 million ounces of silver, also on a payable basis.

This would increase the total payable production from 749,000 ounces of gold to just under 920,000 ounces while the payable silver production would increase from 16.2 million to 25 million ounces. Using the same 75:1 silver:gold ratio applied by Integra to calculate its gold-equivalent numbers, the total payable gold-equivalent production rate would be 1.25 million ounces, up from 954,000 ounces.

While a lot more work needs to be done on all three potential ‘mine life boosters’, there seem to be some legit options on the table to rapidly boost the amount of leachable ounces.

We would like to emphasize the mill scenario is not dead and buried at all. But as it currently stands, it does not make a lot of sense for a pre-development junior mining company to build a $200M+ mill to recover only 400,000 ounces of gold and a few dozen million ounces of silver. There potentially are some ‘easy’ fixes here. Boosting the recovery rate at DeLamar could easily add 100,000 ounces of gold to the mine life while we also shouldn’t forget the reserve calculation was based on the resource status from more than a year ago. As Integra continues to drill the high-grade zones and is able to upgrade those zones into mineable resources and reserves, the mill phase could potentially become interesting again. The only problem right now is the ‘sunk cost’ (= the initial capex) which is relatively high for the anticipated production of just 400,000 ounces of gold as this implies a capex intensity of $500 per ounce. Should the total amount of recoverable ounces increase to 700,000 (an arbitrary number at this point), the capital intensity drops to less than $300 per recovered ounce.

The key elements to further unlock value at DeLamar will be higher recovery rates (and hopefully the Albion process will indeed deliver the desired results) and perhaps a higher gold price.

Conclusion

The mill scenario isn’t dead, but can be and is being deferred by Integra. But we think it makes sense to focus on the heap leach scenario and we sincerely hope Integra will now indeed fully prioritize this. While encountering high-grade intervals at Florida Mountain are confirming the exploration theory, it is clear the market doesn’t care about this optionality… for now. Additionally, the permitting process for a heap leach only mine should be considerably easier than for a full-scale mill and tailings facilities.

And finally, the company’s executive team doesn’t seem to be too worried. Since the pre-feasibility was published insiders have spent almost C$150,000 on buying more stock with CEO George Salamis adding 45,000 shares to his position on top of the 38,000 shares purchased during calendar year 2021 at much higher prices while chairman De Jong added 20,000 shares and CFO St-Germain added 5,100 shares to her position after the publication of the PFS press release. And to top it off, COO Tim Arnold also added 11,500 shares at a price in excess of 10% higher than the current share price. If anything, these strong insider purchases are another convincing argument they are optimistic about the future.

Disclosure: The author has a long position in Integra Resources. Integra Resources is a sponsor of the website.