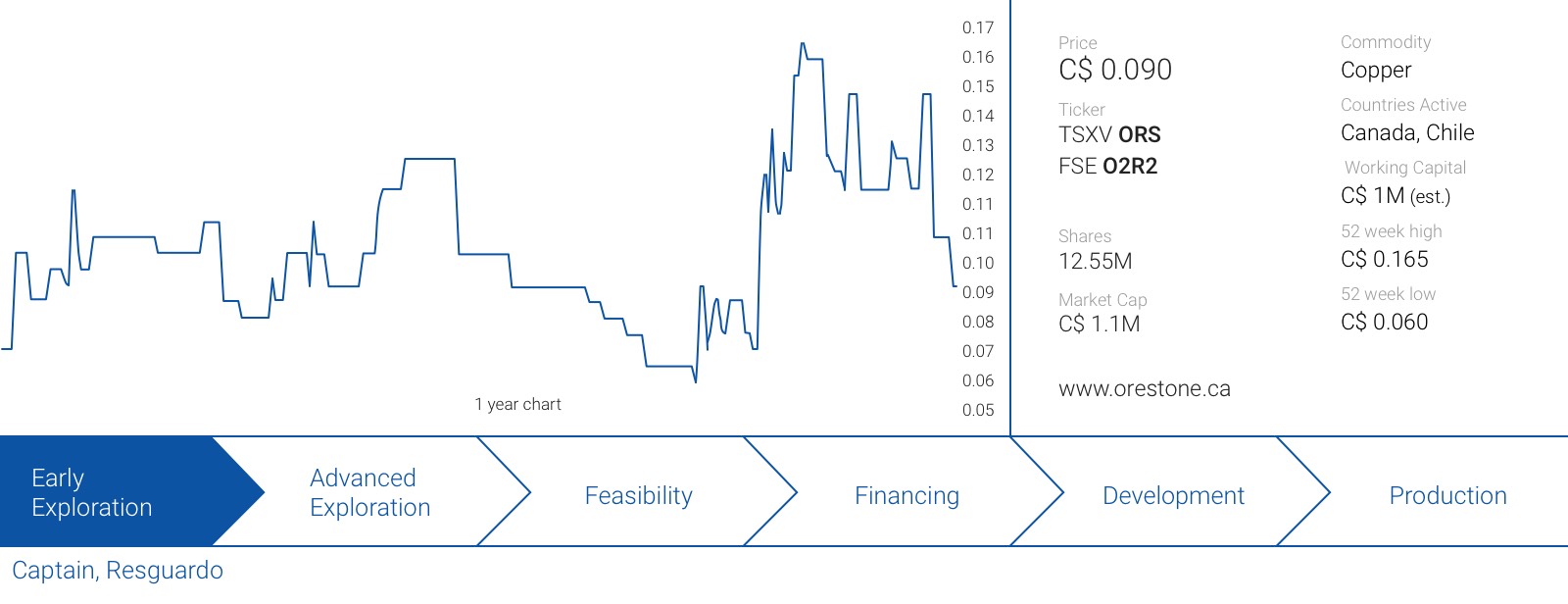

During the summer, we were introduced to David Hottman, a mining veteran and one of the founders of Eldorado Gold who was working on re-launching Orestone Mining (ORS.V). Orestone has recently secured an option to acquire full ownership of the Resguardo copper project in Chile and sits on a drill-ready large copper porphyry target in British Columbia. Both targets seem promising and although these early stage exploration companies are inherently very risky, the risk/reward ratio for a company with a market cap of just C$1.5M appears to be favorable.

A two-pronged approach with projects in Chile and British Columbia

Orestone Mining isn’t just focusing on one project as it added the Resguardo project in Chile to its portfolio. Both projects will be drilled in the coming year.

Resguardo, Chile

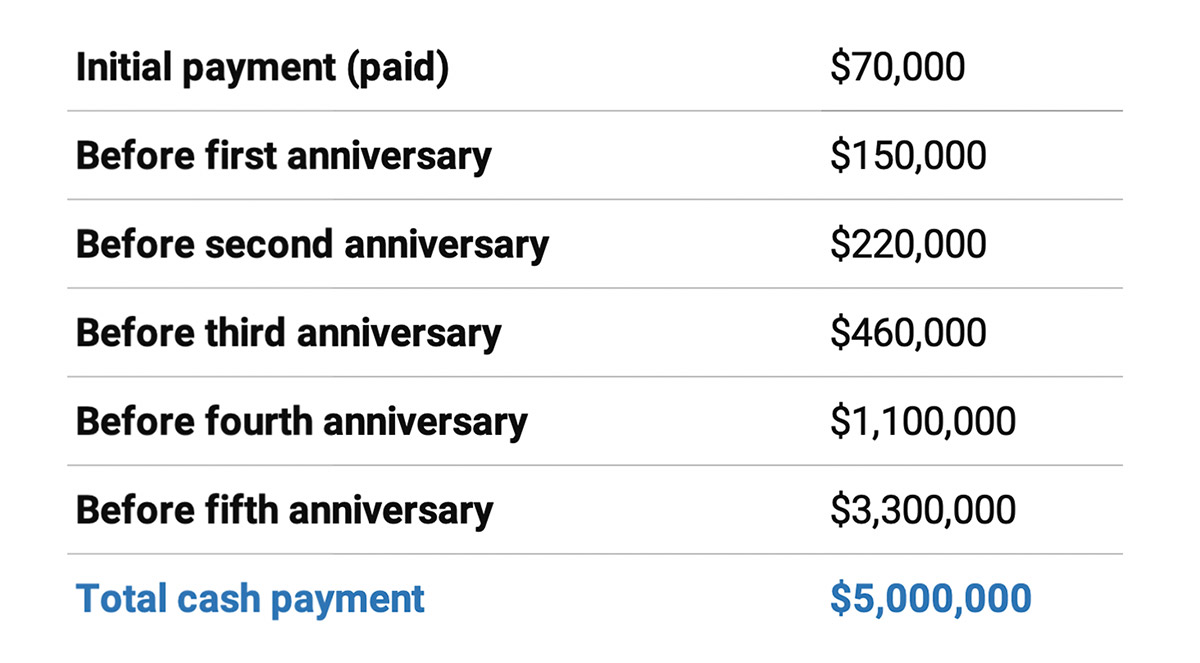

Earlier this year, Orestone Mining secured an option to acquire the Resguardo project from a local Chilean vendor. The option allows Orestone to earn a 100% interest in the property during a five-year period by making US$5M in option payments as well as committing to drill a minimum of 2,000 meters on the project. The cash payments are relatively benign in the first few years of the option agreement. This will give Orestone plenty of time to assess the merits of the property in the first few years before forking over the majority of the cash. The following table shows the current schedule of the cash payments to the optionor.

After completing the earn-in deal, Orestone will issue a 1.5% Net Smelter Royalty to the property vendor, which could be repurchased by ORS for US$6M in cash before the 7th anniversary of the option agreement.

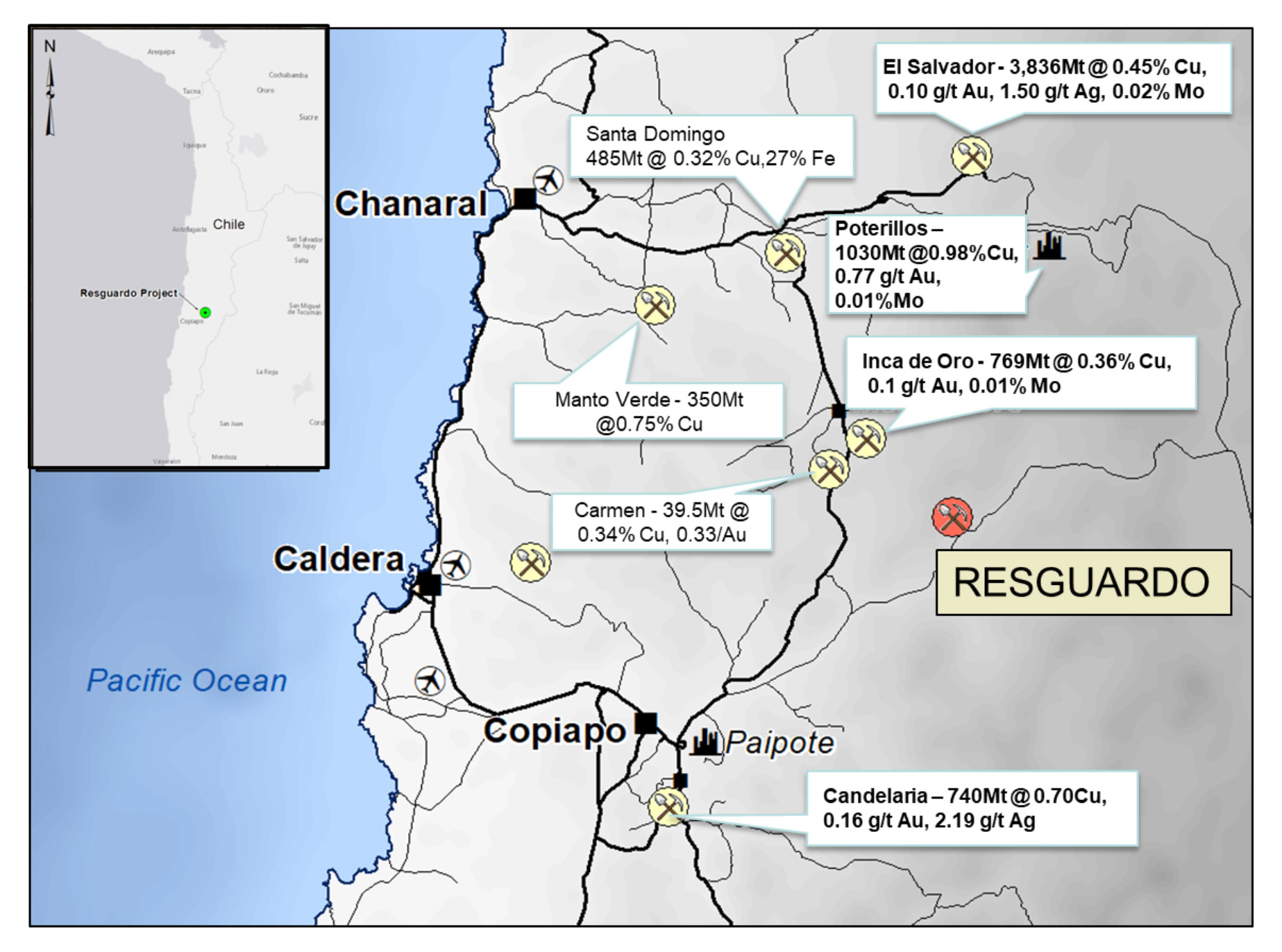

The Resguardo property is located approximately 100 kilometers north of the city of Copiapo which is one of the epicenters of copper mining in the country. The project has a surface area of approximately 2,900 hectares (just over 29 square kilometers) and is located within a known and proven copper district. The project is located on the north/south Domeyko fault line which hosts several of the world’s largest copper deposits and is in close proximity to several fault systems originating in the Maricunga Gold Belt which host numerous gold mines and deposits. Within a 100-kilometer radius from the Resguardo project, other operators have discovered approximately 8 billion tonnes of copper mineralization with a total copper content of approximately 35 million tonnes (77 billion pounds).

On top of that, Kinross Gold’s (KGC, K.TO) Marte and Lobo projects contain a gold-only resource of 185 million tonnes at an average grade of 1.2 g/t gold for a total content of just over 7 million ounces. So as far as location goes, Orestone Mining’s Resguardo project is located in the right place in a very prolific mining district.

Captain, British Columbia

Captain property is located in the so-called Quesnel Trough, a Northwest-Southeast Trough that hosts several multi-billion pound copper projects (of which Mt Polly, Kemess, Red Chris, New Afton and Mt Milligan are probably the best-known large mining deposits).

The Captain property is located just 30 kilometers south of the Mt Milligan mine which is currently owned and operated by Centerra Gold (CG.TO) after its acquisition of Thompson Creek Metals (which was about to go down due to its heavy debt load) a few years ago. Mt Milligan is one of those typical BC copper-gold projects and contains approximately 470 million tonnes at roughly 0.19% copper and 0.3 g/t gold in the proven and probable reserve categories. Low-grade? Absolutely. But Centerra is making it work thanks to the economies of scale associated with a huge project like Mt Milligan (and also because it’s high-grading the asset as the average gold grade in the first nine months of the year was approximately 0.69 g/t).

Looking at the detailed operating results of the Mt Milligan project in Centerra’s Management Discussion & Analysis, the total operating cost was approximately US$48.8M. Considering the company milled 3.75 million tonnes of rock, the total operating cost was just US$13/t. Applying a 75% recovery rate for the copper and the gold (note: Centerra’s recovery rates were 81% for the copper and 64% for gold), a project grading 0.3% copper and 0.3 g/t gold (the 0.3 + 0.3 as average grades is the rule of thumb in British Columbia) has a recoverable value of just over $23/t using a gold price of $1250/oz and a copper price of $2.80/lbs. The margins are still low, but because these BC copper porphyry deposits are massive earth-moving exercises, a 50,000 tonne per day operation would still generate $180M per year in operating cash flow (pre-tax, pre-interest payments and obviously excluding capital expenditures).

Orestone obviously isn’t nowhere near developing a mine (let’s start with figuring the size of the mineralization) but the Mt Milligan case is just meant to explain what to expect from a typical British Columbia based copper-gold porphyry system. The grades will be low, but due to the size of these projects, they are viable. On top of that BC copper concentrate is usually pretty clean and highly sought after by Asian copper smelters to blend it with inferior products.

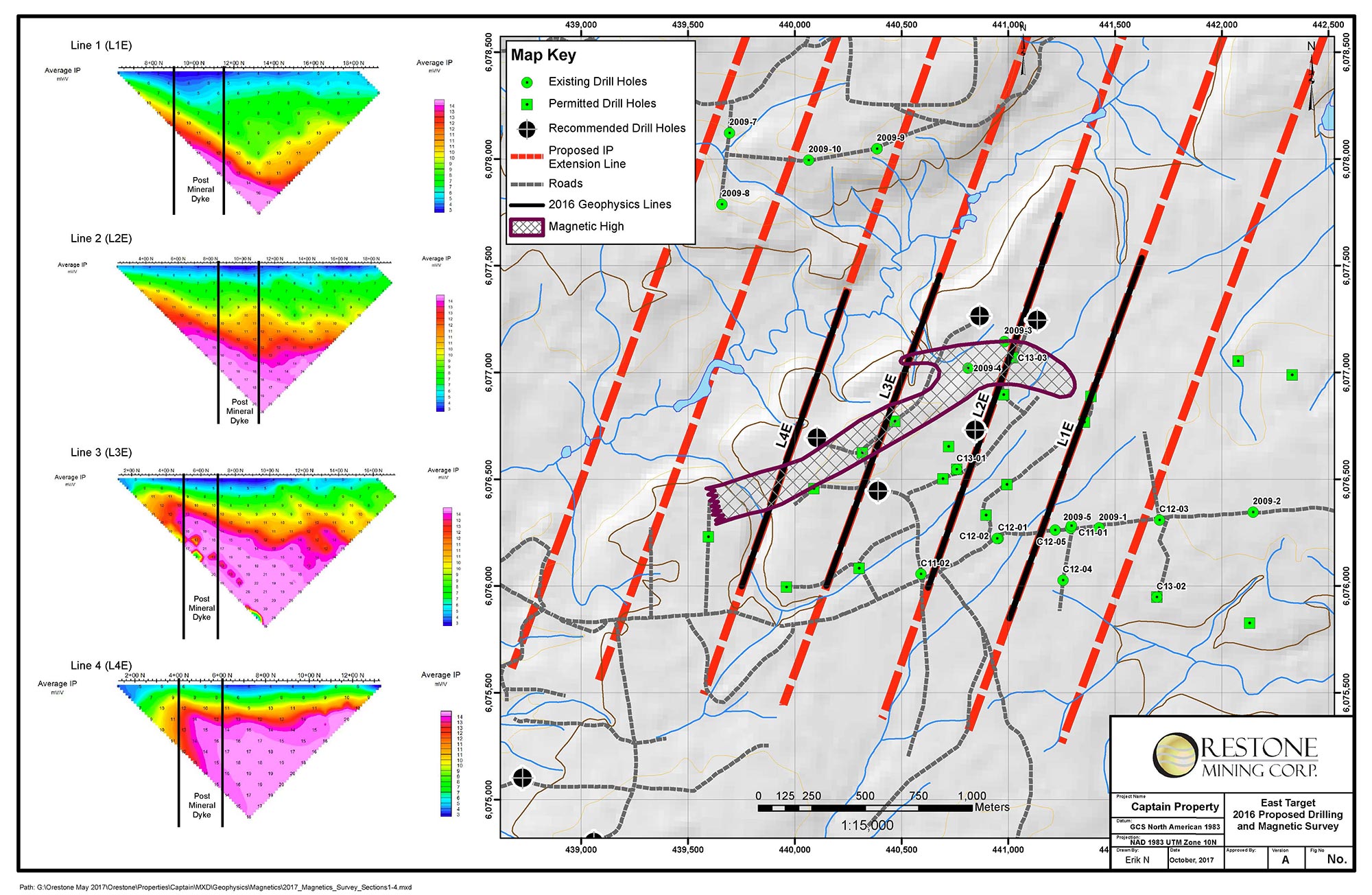

Several previous owners have spent a total of almost C$5M on exploration at Captain, which includes almost 150 kilometers of ground magnetometer programs as well as 44 line kilometers of IP. On top of that, 11 holes were drilled for in excess of 2,800 meters of drilling.

The last hole intersected three meters of 0.23% copper and 1.9 g/t gold. Encouraging, but it was clear the drill targets needed to be fine-tuned even further.

Back in 2016, when the resource sector came back to life, Orestone Mining conducted a more precise IP survey of 8 line kilometers (4 lines of 2 kilometers each) as well as detailed magnetics, and this has helped to further define a high-priority exploration target of 2000 meters by 1000 meters that is believed to be the source of the three meters of 1.9 g/t gold and 0.23% copper.

We are talking about a very large system here that could easily contain 200 million tonnes of mineralized material. This doesn’t mean there’s any guarantee to discover a new mine, but Orestone is clearly hunting elephants.

The company has designed a US$225,000 exploration plan for the Captain property. It will be a small program to get a better understanding of what might be hiding under the surface, and for now, Orestone’s limited exploration plans include a 3-hole, 900-1000 meter HQ drill program to drill-test the IP anomaly.

It’s also interesting to note Rob Pease, the former CEO of Terrane Metals (who developed the Mt Milligan mine before it was acquired by Thompson Creek Metals) is an advisor to Orestone Mining.

A closer look at the Chilean project

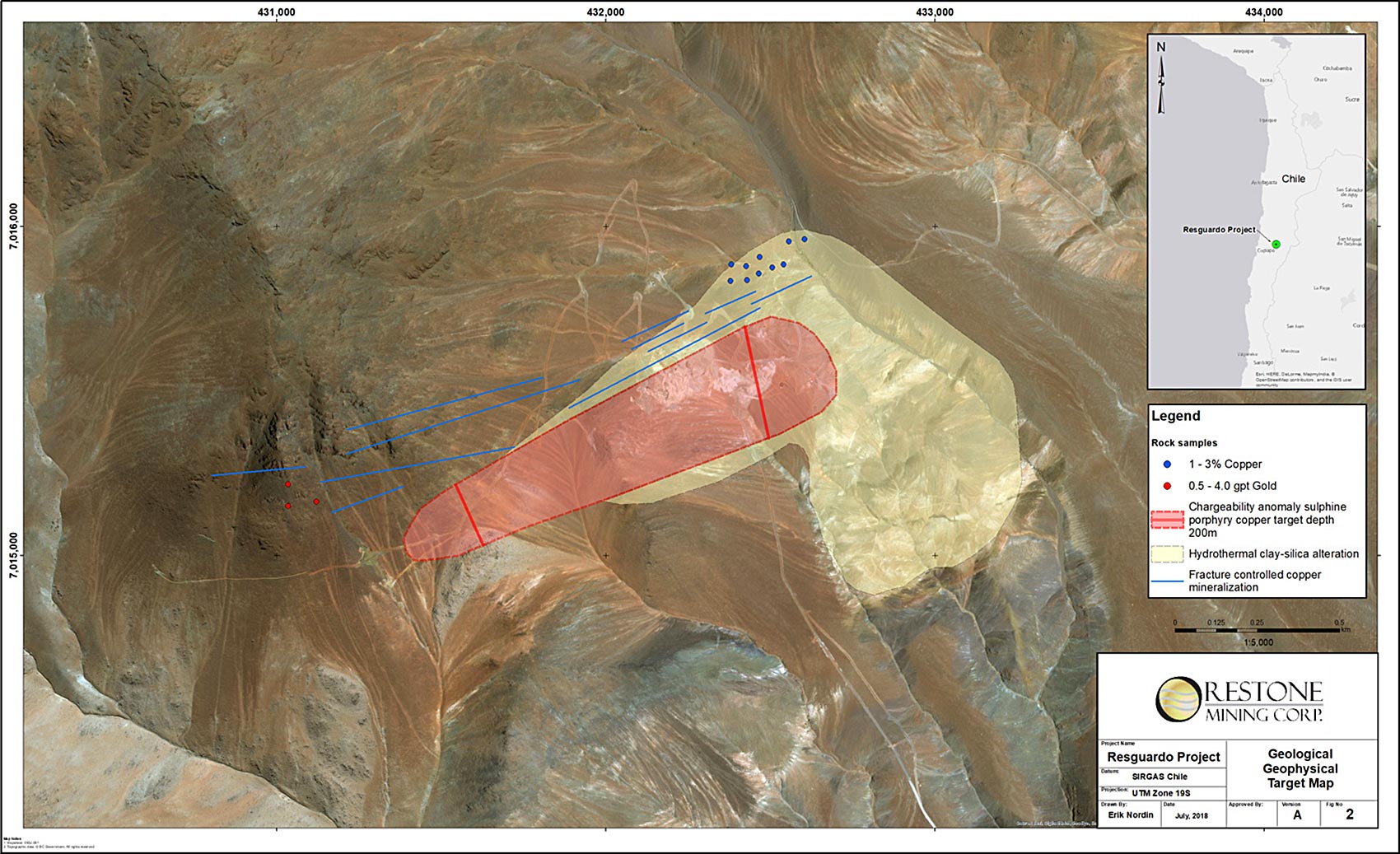

The Chilean project is actually quite interesting. There have been some historical mining activities on the property from a shallow open pit of 60 by 150 meters (which means perhaps 1-1.5 million tonnes have been taken out) at an average grade of 0.6 g/t gold and 1-2% copper. Additionally, the artisanal miners went underground and excavated a little bit higher grade rock as well.

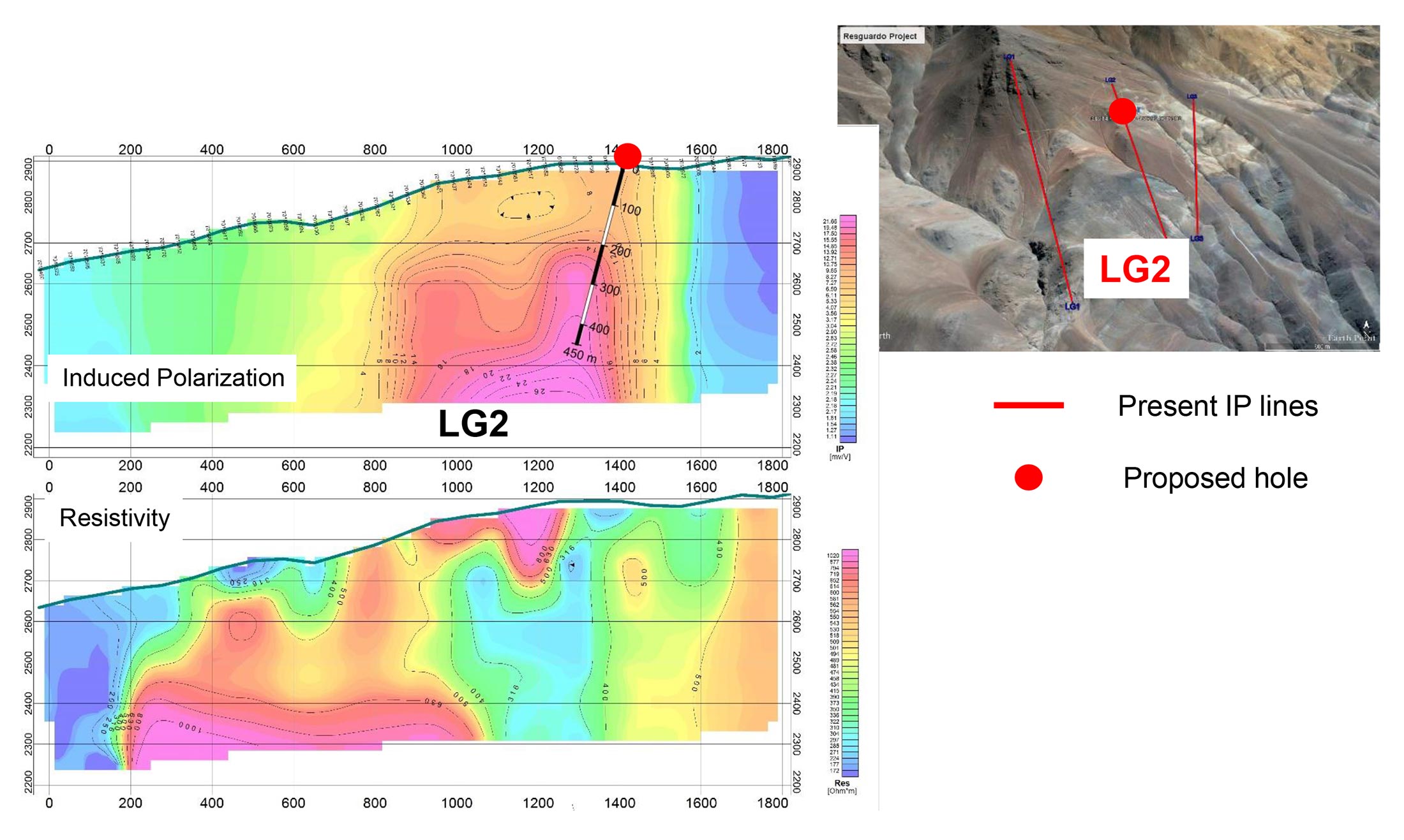

Below this oxide zone, there’s a large IP chargeability anomaly with a total strike length of 1000 meters and widths of 300-600 meters for a currently known surface area of 450,000 square meters. And this could still expand as the anomaly remains open to the southwest. This anomaly could indicate the presence of a large sulphide system starting at a depth of approximately 200 meters.

There’s no certainty there’s a large mineralized body there, but this is exactly how the Candelaria copper mine (currently majority-owned by Lundin Mining (LUN.TO) and a bit further south-southwest of Resguardo) was discovered. The original discovery of the Candelaria mine was based on an IP anomaly that was subsequently drilled.

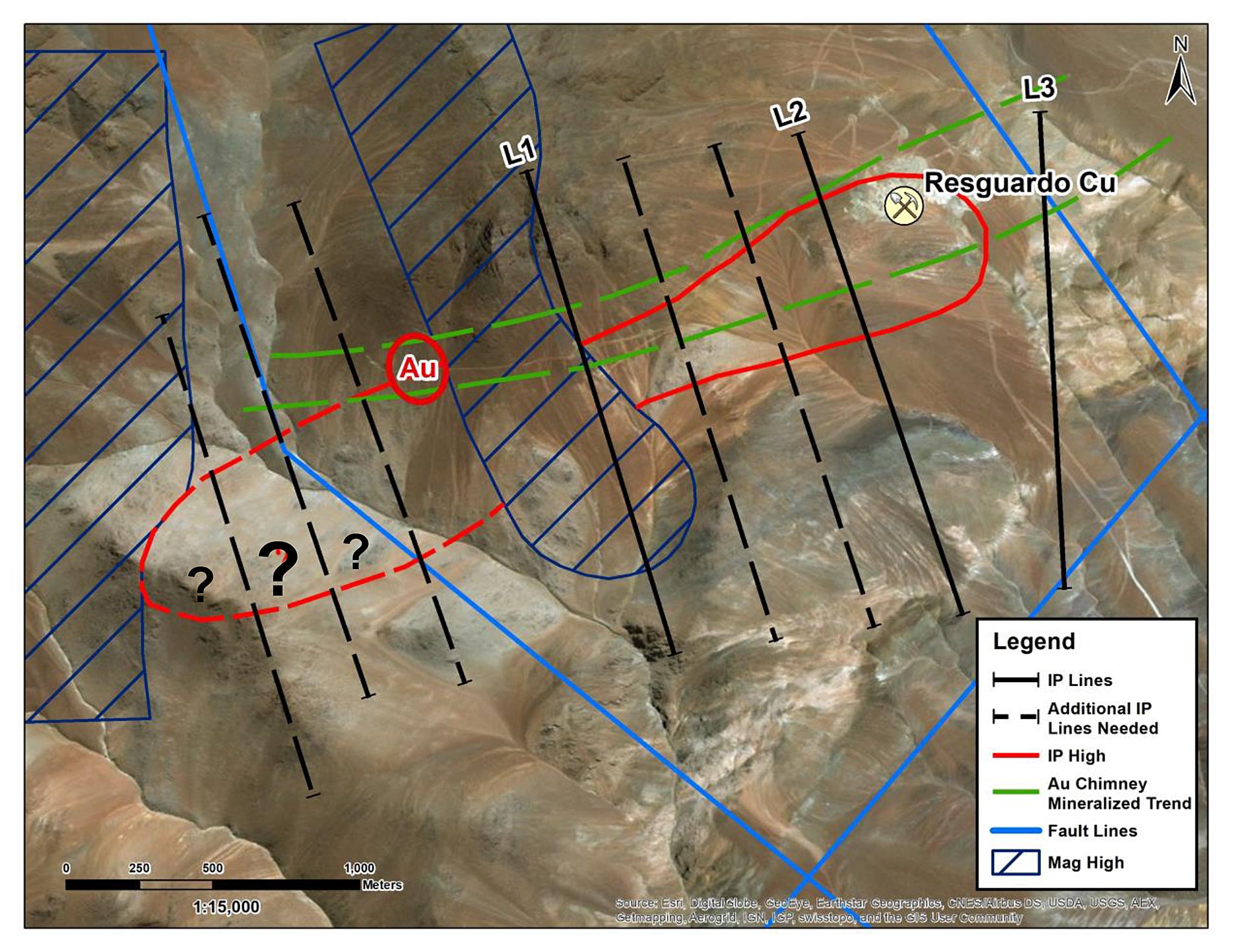

Once Orestone raises the money (see later), it will immediately complete an additional IP survey focusing on the resistivity levels of the deeper zones. This will allow the company to pinpoint high-priority locations for its drill program. And you shouldn’t think Orestone will spend its entire cash position on this initial exploration program; the total cost of the IP survey and the 3-hole drill program (targeting a depth of 300-350 meters per hole) is estimated at just over C$250,000. There’s no guarantee Orestone will hit economic grade copper mineralization in those two holes, but an exploration program of a quarter of a million dollar could best be described as a ‘low-cost but potentially high-impact’ investment in the property.

Downside protection in Chile?

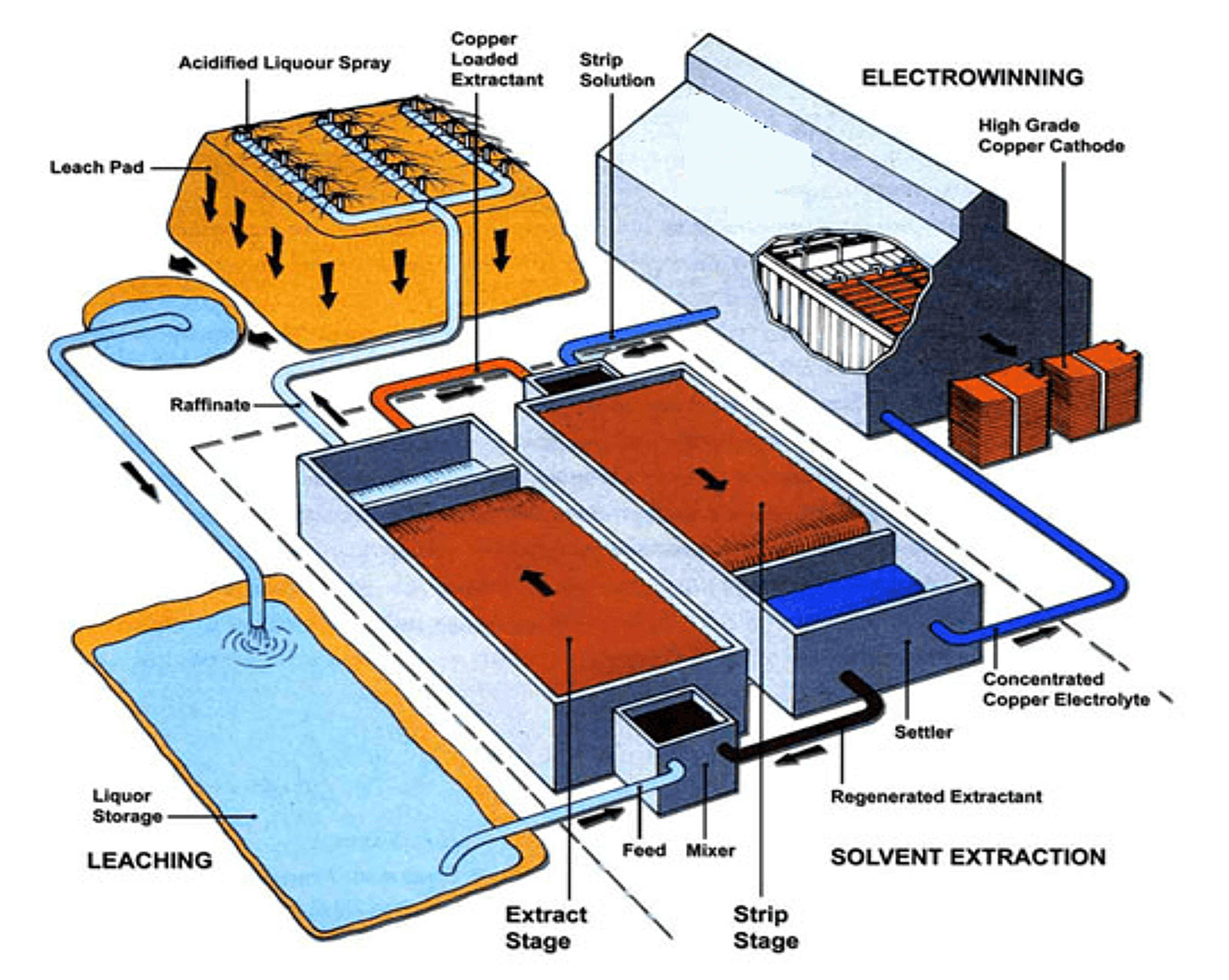

It’s important to realize this isn’t ‘just another’ copper-gold porphyry project, as the mineralization appears to start at surface and has been oxidized. This means it should be possible to recover the copper through a simple heap leach process on-site. A good example could for instance be Deep South Resources (DSM.V) which recently published a Preliminary Economic Assessment on its copper heap leach project in Namibia that has a lower grade of 0.31% copper (and no by-products):

This also means there’s an interesting ‘Plan B’ on the table at Resguardo. Should the first few holes targeting the large IP anomaly come up dry, Orestone Mining could start looking into mining and processing the oxides at surface which is the low-hanging fruit in this case. Again, there’s absolutely no guarantee an oxide mining scenario could be profitable, but we consider it to be an interesting option to consider should the first drill holes not yield the eyed results.

Raising money to drill in Chile

Orestone Mining is currently raising money to fund its upcoming exploration program in Chile. The company plans to issue 7 million units to raise a total of C$1.0M, as the units will be priced at C$0.10 with each unit consisting of one common share in Orestone Resources as well as ½ of a warrant. This capital raise doesn’t come as a surprise as Orestone had just over C$100,000 in the bank as of the end of its second quarter in July.

Each full warrant will allow the warrant holder to acquire an additional share of Orestone at C$0.15 for one year after the closing date of the financing.

Assuming Orestone will be able to raise the amount it’s eyeing, the share count will increase from 12.55 million shares to 22.55 million shares, while additional warrants will be added to the current warrant count of 4.5 million. At 22.55 million shares, Orestone’s market capitalization would still be just C$2.3M based on the PP price, and just over C$2M based on the most recent closing price.

That being said, the majority of the 2019 warrants are now in the money. According to the most recent financial statements, Orestone has 500,000 warrants expiring in June with an exercise price of C$0.15, but we care more about the 3.99 million warrants with an exercise price of C$0.10 as those have a better chance to be in the money and will most certainly be exercised should Orestone Mining be successful in the upcoming exploration program. This would add C$400,000 to the cash position, and would also increase the share count to almost 26.5 million shares, which is still very reasonable.

Management

Perhaps the best way to describe the Orestone Mining management team is ‘been there, done that’. David Hottman (CEO) and Gary Nordin (director and senior consulting geologist) were the founders of Eldorado Gold while Hottman also founded Nevada Pacific Gold (sold to McEwen Mining (MUX, MUX.TO)) and Nordin was a founder of Bema Gold (sold to Kinross Gold).

Orestone has been dormant for a little while but rather than running the company’s treasury dry, expenses were cut, and CEO Hottman takes a very moderate salary of just C$5,600/month (which is currently being accrued). This does give us the impression the Orestone team is doing what it takes to make this company successful (most other management teams would just keep a full salary and just let it accrue or convert it into cheap stock.

David Hottman – President & CEO

Mr. Hottman has 30 years experience in corporate finance and management of resource companies. He is a founder of Portal Resources, Eldorado Gold (TSX, NYSE) and Nevada Pacific Gold acquired by McEwen Mining (NYSE) in 2007.

Gary Nordin – Director

A leading exploration geologist with a proven track record of identifying and developing important resource projects. He’s founding team member of Eldorado Gold (TSX, NYSE) and Bema Gold which was acquired by Kinross.

Julia Aspillaga – Director

Ms. Aspillaga has more than 30 years of minerals industry experience in Chile and other Latin American countries. In the 1990’s she was manager of Bema Gold in Chile and played a key role in the development of the 5.4 million-ounce Refugio Gold Deposit. Julia was also responsible for bringing the Cerro Casale project to the Bema Group, now in excess of 23 million ounces of gold. She currently participates in the IMT Exploraciones Chile Fund as a Member of the Advisory Team.

Mark Brown – CFO

Senior financial management professional acting as CFO and director to several public companies. Mr. Brown is a founder of Galileo Exploration and managed the financial departments of two TSE 300 companies, Miramar Mining Corp. and Eldorado Gold Ltd.

John Kanderka – Director

Mr. Kanderka has 40 years of experience in the minerals and oil and gas sectors. His corporate experience spans acting as an officer and as a director in both the private and public sectors in various roles, including strategic planning, corporate finance, management and administration. He has been a company founder and company builder with a wide array of experience in asset purchase and sale transactions, mergers, buyouts, and reorganizations.

Patrick Daniels – Director

Mr. Daniels is a senior mining engineer with 30 years of experience. Patrick has worked in multiple commodities spanning 13 countries and over 50 projects. At Caterpillar’s Global Mining Consulting Group, he helped lead mine operational assessments and production studies throughout the Americas and Africa. As Engineering Manager for Gustavson Associates, he authored and managed a variety of project technical studies.

Orestone also has also two mining veterans on its advisory board:

Marc Blythe – Advisor to the Board

P.Eng., Advisor to the Board – Marc has extensive international mining and mineral exploration experience for gold, copper, silver, nickel and zinc. He has evaluated projects worldwide, providing advice on transactions and the associated debt and equity financing, to buyers, sellers and financial institutions. Mr. Blythe has managed mines for both Placer Dome and WMC Resources (formerly Western Mining Corporation) during his 22-year mining career. He has a strong understanding of mine feasibility and led two feasibility studies which resulted in successful operating mines the Raleigh Mine and the Bullant Mine, both located near Kalgoorlie, Western Australia.

Robert Pease – Advisor to the Board

Mr. Pease was previously the founder, CEO and a Director of Terrane Metals Corp., which owned the Mt. Milligan project until it was acquired for $700 million in 2010 by Thompson Creek Metals. He is also a former Director and Strategic Advisor to Richfield Ventures Corp., a junior gold mining company in British Columbia which was acquired by New Gold Inc. through a plan of arrangement valued at approximately $550 million. Previously, he was employed by Placer Dome for twenty five years, most recently as General Manager, Canada Exploration and Global Major Projects.

Conclusion

Even after taking the impact of the current capital raise on the share count into account, Orestone’s market capitalization will be just C$2-3M with approximately C$1M in cash on the bank. This indicates the leverage on a potential copper discovery could be enormous, but it’s also important to emphasize everything depends on the exploration success of the team on the ground.

The Chilean exploration program will start immediately, but its successful outcome will depend on the cash Orestone is able to throw at the project (you shouldn’t assume Orestone will immediately hit the proverbial mother lode). Any early stage drill play is per definition speculative and that’s how you should look at Orestone Mining: as a high risk / high reward exploration play.

Disclosure: The author currently has no position in Orestone Mining but will participate in the announced placement. Orestone currently isn’t a sponsor of the website, but could become one. Please read the disclaimer