Integra Resources (ITR.V, ITRG) is a direct beneficiary of the current high gold price. The company was somewhat lucky to acquire the high-cost Florida Canyon gold mine in 2024 and now clearly benefits from the current gold price environment, resulting in an anticipated margin of in excess of $2,000/oz based on the anticipated All-In Sustaining Cost this year.

That cash flow is very useful to fund all exploration programs across the three main assets, while aggressively advancing DeLamar to become the company’s second producing asset. It has already been established the current administration in the White House likely created the best permitting climate in the USA in the past few decades, and Integra needs and wants to capitalize on that by completing the permitting process in Idaho.

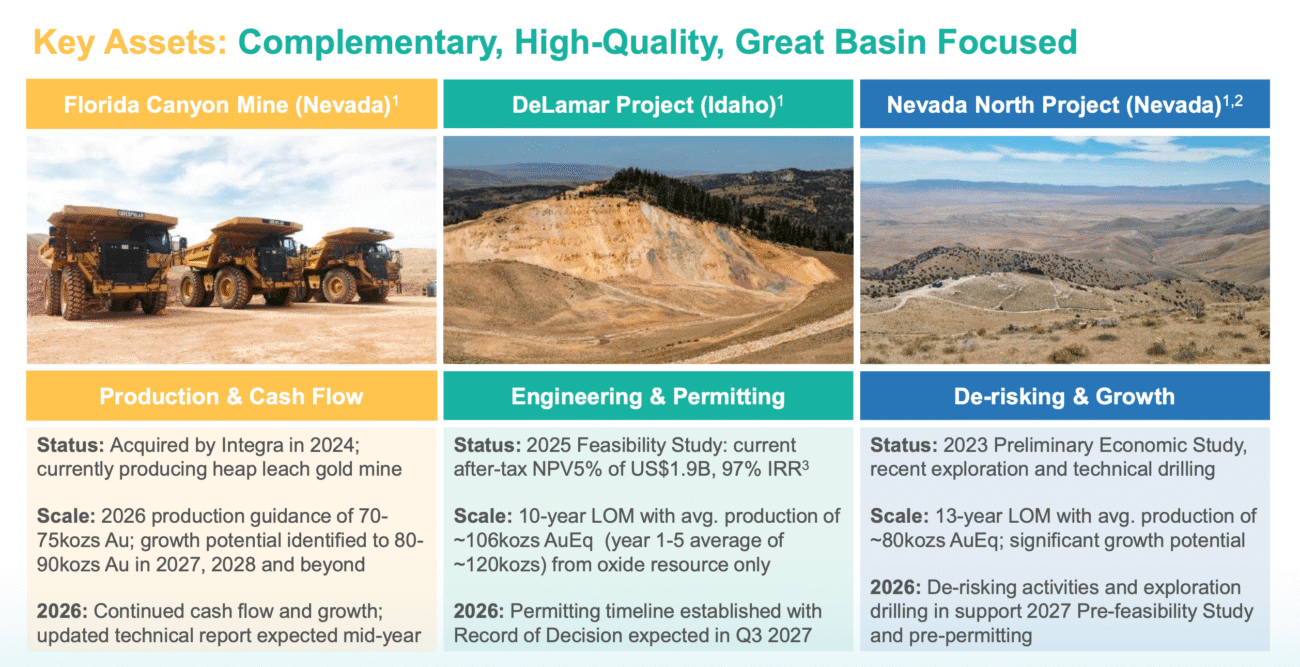

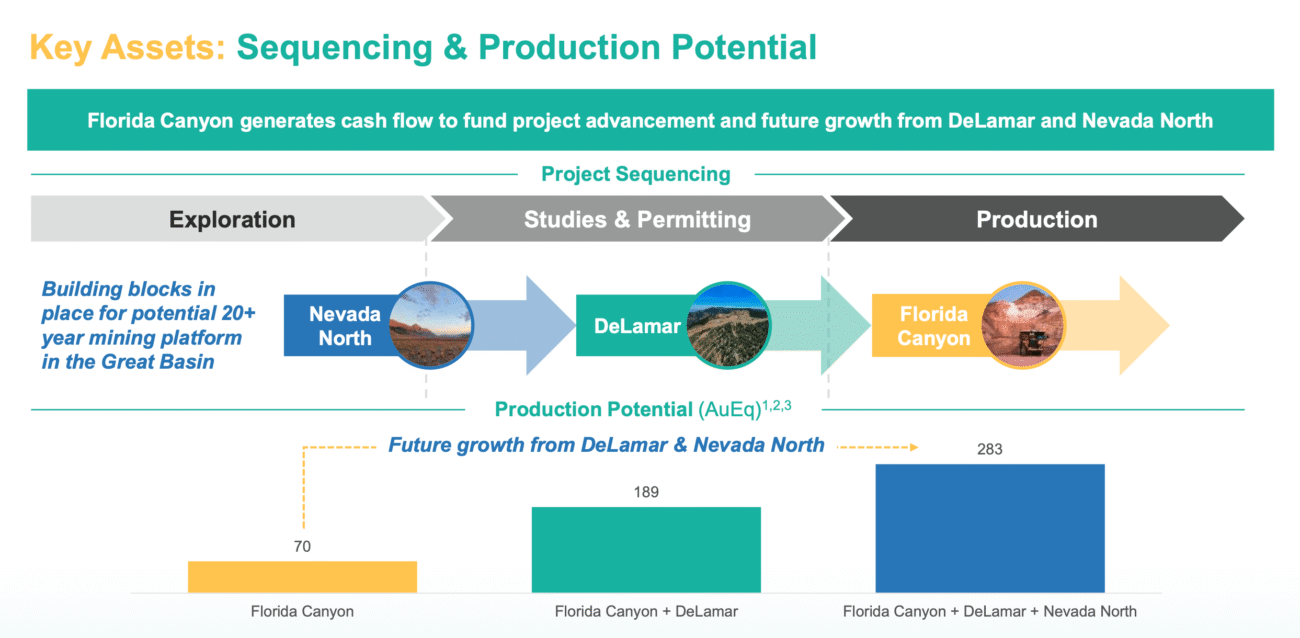

Meanwhile, exploration is ongoing at Florida Canyon (which should extend the mine life of the asset) while a recently approved Exploration Plan of Operations for the Wildcat deposit (part of the Nevada North project) will make exploration much more efficient ahead of a H2 2027 Pre-Feasibility Study.

Unless indicated otherwise, ‘$’ will refer to US Dollars.

The Q1 production was a bit light, but the full-year guidance remains unchanged

In the first quarter of 2026, Integra Resources produced 12,635 ounces gold, of which 12,518 ounces were sold. The average mining rate achieved a record volume at almost 77,000 tonnes per day as the company mined 3 million tonnes of ore and 3.9 million tonnes of waste.

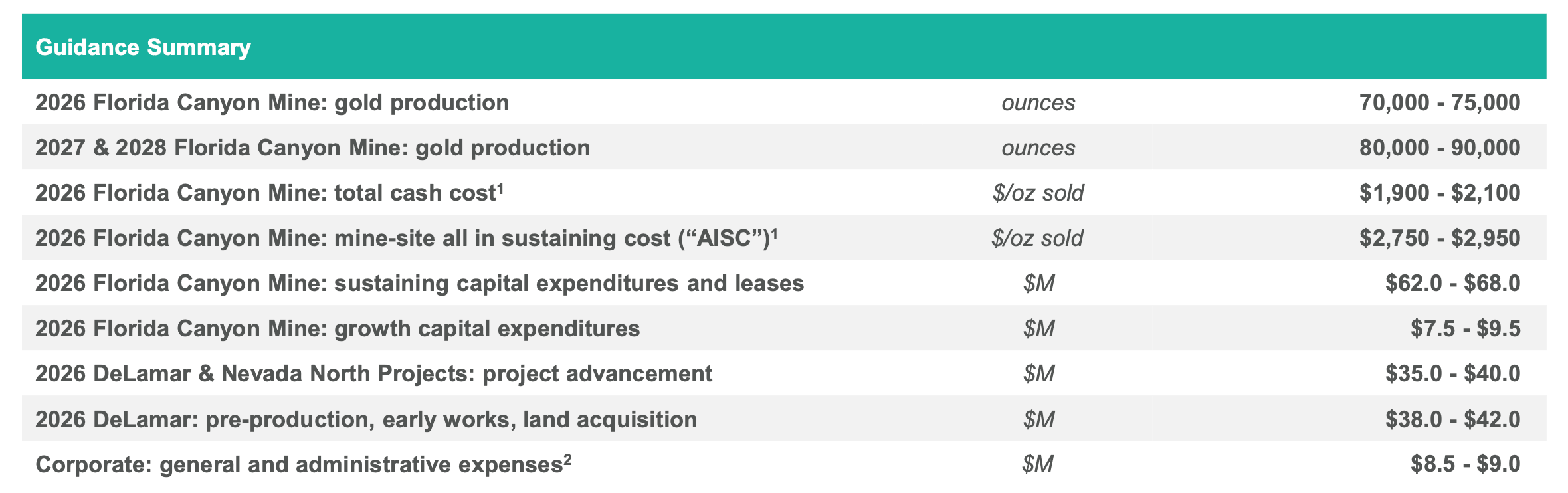

Although the company had been guiding for a lower production rate in H1 and a strong uptick in H2 (with a 45/55 breakdown), the Q1 production result came in below expectations. The company refers to 3,000 ounces of deferred production due to a temporarily reduced solution flow rate to one specific leach pad cell with contains fine ore from a newly opened pit. Integra’s technical team had to design a blending strategy to maintain nominal leach rates which means a delayed recovery of those 3,000 ounces of gold. Integra Resources has reconfirmed its full-year production guidance at 70,000-75,000 ounces of gold. In order to meet the lower end of the guidance, the average production rate in the next three quarters should be around 19,000 ounces.

Keep in mind the 45/55 breakdown is still valid. And assuming the lower end of the production guidance, approximately 38,500 ounces will be produced in H2 versus 31,500 ounces in H1 (of which 12,600 have now been produced). It will be interesting to see if the split changes, perhaps to a 40/60 ratio. While this would change the timing of the free cash flow generation, it should have no impact on the financial situation and the liquidity on the balance sheet. The $61M bought deal completed in Q1 ensures the company can handle any and all cash flow delays without having to postpone the planned investments at Florida Canyon.

But one thing is certain: the current gold price environment is very forgiving. Even if there would be a slight guidance miss, the financial impact would likely be limited while it would set up Integra for a much stronger 2027 on a comparable basis.

Diving into the numbers

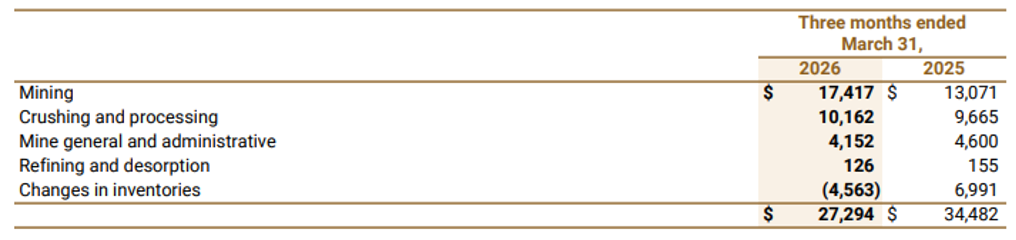

Integra reported a total revenue of almost US$62M and this resulted in a mine operating earnings result of just under $25M, which is more than 50% higher compared to the first quarter of 2025. Not only was the revenue slightly higher (despite the lower gold production), the total amount of operating expenses decreased on a YoY basis. Before getting too excited, the footnotes explain this is an accounting element as there was a $4.6M positive impact from the valuation change in inventories which almost reversed a $7M negative impact compared to a year ago. As the table below shows, the ‘pure’ operating expenses did increase on a YoY comparable basis, and that was of course to be expected as the total tonnage that was mined increased as well.

This is why it is always interesting to look at the cash flow statement, which we find more important and interesting for mining companies versus the income statement.

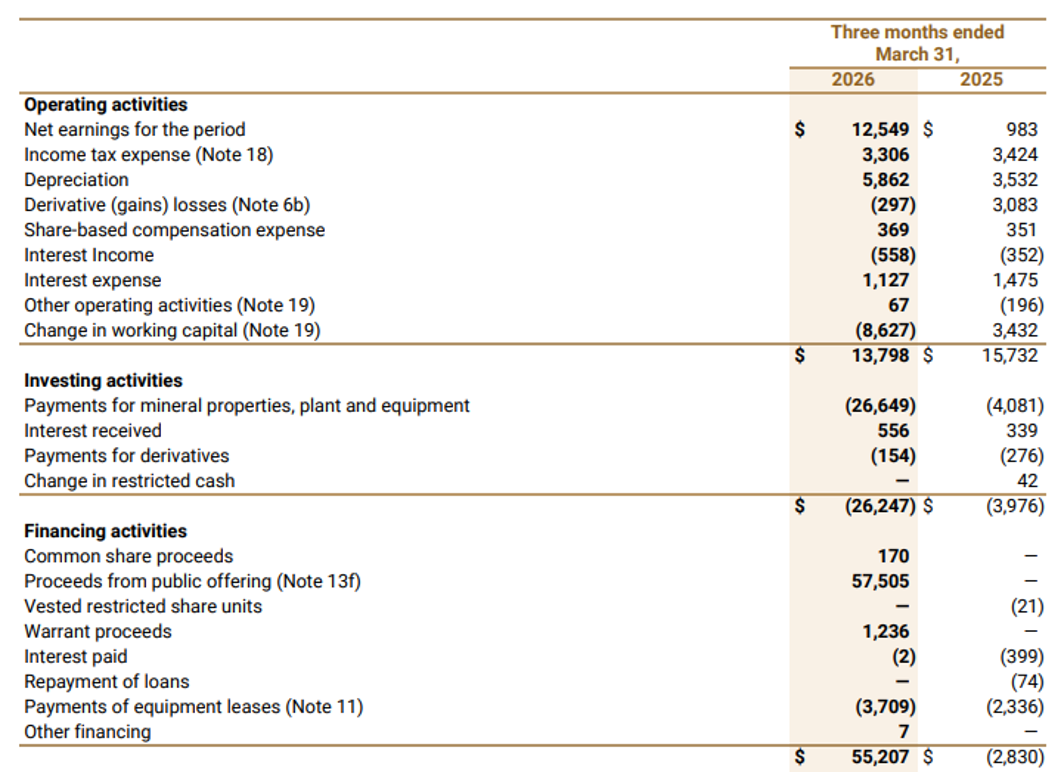

Integra reported an operating cash flow of $13.8M and after adjusting this for changes in the working capital and after deducting the $3.7M in lease payments while adding $0.5M in interest income, the underlying adjusted operating cash flow was approximately $19M.

This was not sufficient to cover the almost $27M in capital expenditures, but there are two caveats here.

First of all, Integra’s 2026 capex spend is front-loaded; a disproportional amount of the full-year capex was spent in the first quarter, and this of course skews the comparable basis. Adding to this, Integra also acquired a $12.5M land package in Idaho close to its DeLamar flagship project, and not only is this a non-recurring item, it also highlights one needs to make a distinction between sustaining capex and growth capex.

In its MD&A, Integra confirmed the sustaining capex came in just over $7M (excluding leases, which we already accounted for) which means the company was clearly cash flow positive on an underlying basis using the sustaining capex. This number is more or less in line with the anticipated $62-68M in full-year sustaining capex and lease payments.

Secondly, keep in mind about 3,000 ounces of production were deferred due to some issues. If those additional gold sales would have been realized in Q1, the net underlying free cash flow would have exceeded $10M for the quarter.

The balance sheet provides plenty of flexibility to rapidly advance DeLamar

Using the midpoint of the guidance below, Integra expects to spend $73M at Florida Canyon and $78M on DeLamar and Nevada North, for a total of $151M. However, just about 40% of that number is classified as a sustaining capex and the majority of the number is related to aggressively advancing DeLamar.

This also explains why Integra completed a financing in Q1, as this will give the company plenty of flexibility and breathing room to advance DeLamar at its own pace without being too dependent on the Florida Canyon cash flows.

As $26.5M has already been spent in Q1, the anticipated remaining capex will likely be somewhere in the $125-130M area. And using the low-end of the production guidance and the high-end of the cash cost guidance, Florida Canyon will produce approximately 57,500 ounces of gold at a cash cost of around $2050/oz in the remaining three quarters this year. This means that as long as the realized gold price exceeds $4,400/oz, Integra’s Florida Canyon cash flows will cover all planned investments, including the almost $80M in DeLamar related spending.

This means we don’t expect the cash position to increase by year-end, but we are also quite confident that – at the current gold price – Integra should be able to maintain that $100M in cash on the balance sheet throughout the year. There will always be some fluctuations due to timing (spending capex and generating revenue is definitely not a linear process), but generally speaking, we don’t expect the cash position to drop below $100M.

And this will put Integra in a very strong position to head into 2026. Whereas the production guidance for this year uses 72,500 ounces as its midpoint (but we are using 70,000 ounces in the base case scenario), the midpoint of the 2027 and 2028 production guidance is a more impressive 85,000 ounces of gold. This means that from next year on, the company will produce about 15,000 ounces gold more than this year. Combine that with an anticipated lower sustaining capex, and it is clear 2027 will be the year where we will see the cash position build (of course subject to the DeLamar construction schedule).

With $106M in cash and a positive working capital position of approximately $140M, Integra’s balance sheet is sufficiently robust to backstop all investment plans.

Advancing DeLamar and Nevada North

The Florida Canyon mine is just the cash flow engine for Integra Resources, and the main reason to acquire the asset was for Integra to avoid having to go back to the market every year to raise C$20-30M in order to maintain its pace on the development stage projects. And the mine is doing exactly what it is supposed to do, with the current strong gold price as an important tailwind.

At DeLamar, the company completed a strategic land purchase and paid a $3.5M deposit to Idaho Power. This was a requirement for the latter to start working on planning an upgrade to the existing power infrastructure that would link the mine with the existing power infrastructure.

The project’s permitting timeline was also posted to the FAST-41 project dashboard in January, and Integra will be designated a dedicated project advisor from the Permitting Council, which will monitor the advancement of the project. Not unimportant: the FAST-41 project dashboard highlights a 15 month NEPA permitting schedule from start to finish. This means the permitting phase should be completed within the current term of the Trump Administration, allowing Integra to also capture the political tailwinds we currently see in the USA when it comes to permitting and developing.

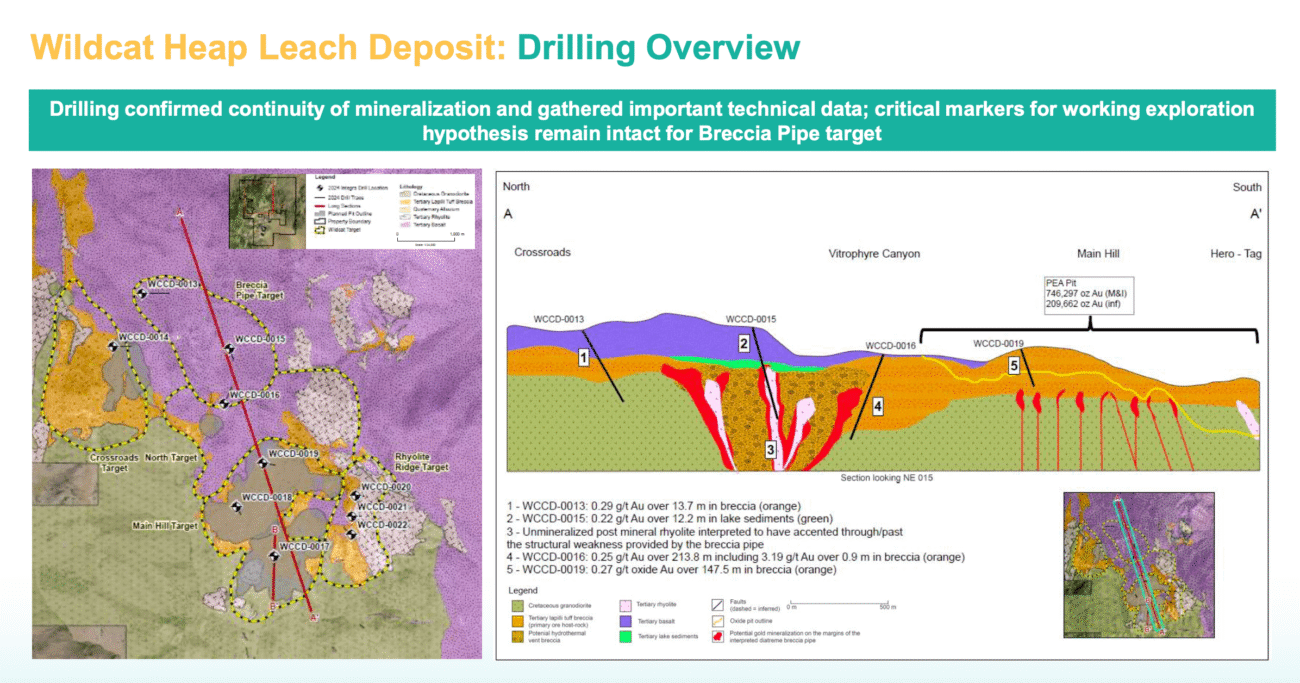

In Nevada, the company recently received the NEPA Decision Record and Reclamation Permit approving its Exploration Pan of Operations for the Wildcat deposit, part of Nevada North. This permit will allow for expanded exploration and development activities at Wildcat given the larger allowance for disturbance, including the ability to construct drill roads and drill pads on the project.

This will pave the way for all activities that are required to upgrade the 2023 Preliminary Economic Assessment at Nevada North to a Pre-Feasibility Study as the Mountain View deposit already went through these steps. The pre-feasibility study is expected to be completed in the second half of 2027 and it will be good to see an official update on the anticipated capex and opex, and the updated NPV and IRR using gold prices above $3,000/oz.

As Nevada North is located just over 40 kilometers west of the Florida Canyon mine, there likely will be synergy benefits when it comes to equipment (maintenance), staffing and shared overhead expenses.

Conclusion

Integra Resources remains on the right path to complete what should be the final capex-intensive year at Florida Canyon. The full-year production guidance remains unchanged at 70,000-75,000 ounces of gold while the all-in sustaining cost per produced ounce is still expected to come in at $2750-2950/oz. Given the light Q1 production results and notwithstanding the actual production of 3,000 ounces of gold was simply deferred to later quarters, it probably makes sense to expect the lower end of the production guidance and higher end of the AISC guidance (and then hoping to be positively surprised).

From a risk/reward perspective, Integra still offers great potential. 2026 is the last difficult year where a slightly lower production and a higher sustaining capex are putting the brakes on the Florida Canyon cash flow. Raising $57.5M in net proceeds from the Q1 financing is a solid proactive move and with a little bit of luck, this could have been the final equity raise for Integra as we obviously expect the majority of the DeLamar construction capex to be debt-funded.

From 2027 on, Florida Canyon should throw off more free cash flow as the total amount of sustaining capex and growth capex should decrease quite meaningfully. An updated mine plan and technical report will be published soon, and we believe that could be the next catalyst. We believe that an updated NPV calculation for Florida Canyon at $4000 gold may come in pretty close to or even exceed the company’s current enterprise value. In that case, investors get the exposure to DeLamar and Nevada North for free.

Disclosure: The author has a long position in Integra Resources. Integra Resources is a sponsor of the website. This post is for educational purposes only; be mindful investing in junior mining stocks is risky and you may lose your entire investment if things go wrong. Please read the disclaimer.