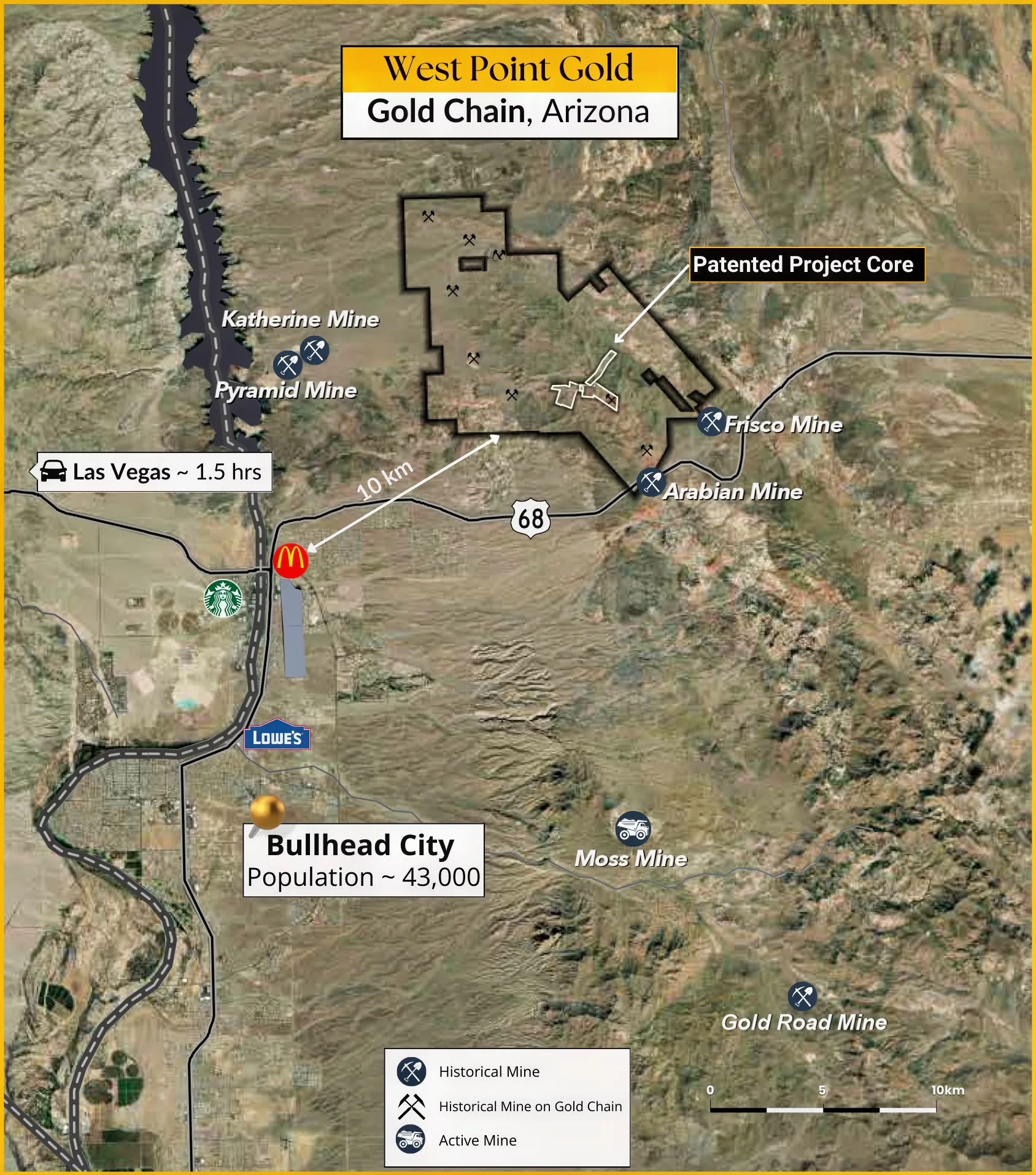

Since its recapitalization event in 2024, West Point Gold (WPG.V) has been working hard to rapidly advance its flagship Gold Chain project. The company tapped the market in the first quarter of the year, and this will allow it to continue its ongoing drill program, complete a maiden resource estimate on the Tyro Main Zone. On top of that, West Point Gold should be fully funded to also complete a Preliminary Economic Assessment at Gold Chain (we are assuming the maiden resource will be good enough to advance the project to the PEA stage).

While the low-hanging fruit can be found on the Tyro Main Zone, the company has also spent some time on some of the regional exploration targets. The initial results of the Sheep Trail Target are encouraging and we expect the company to continue to work on delineating its exploration targets.

The recent Tyro Main Zone results continue to add value

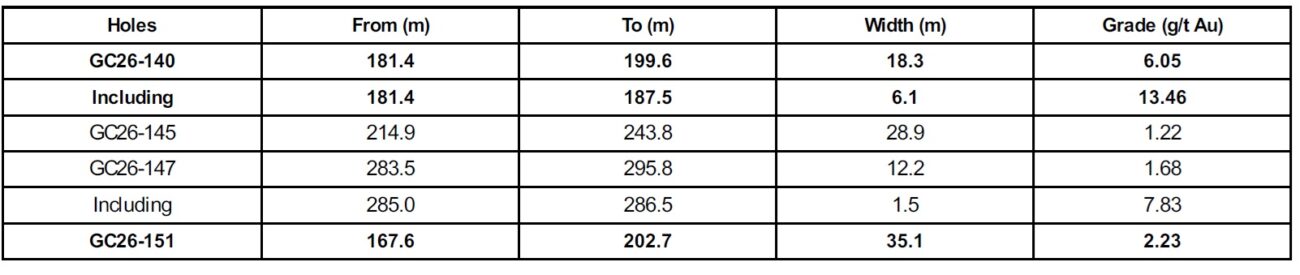

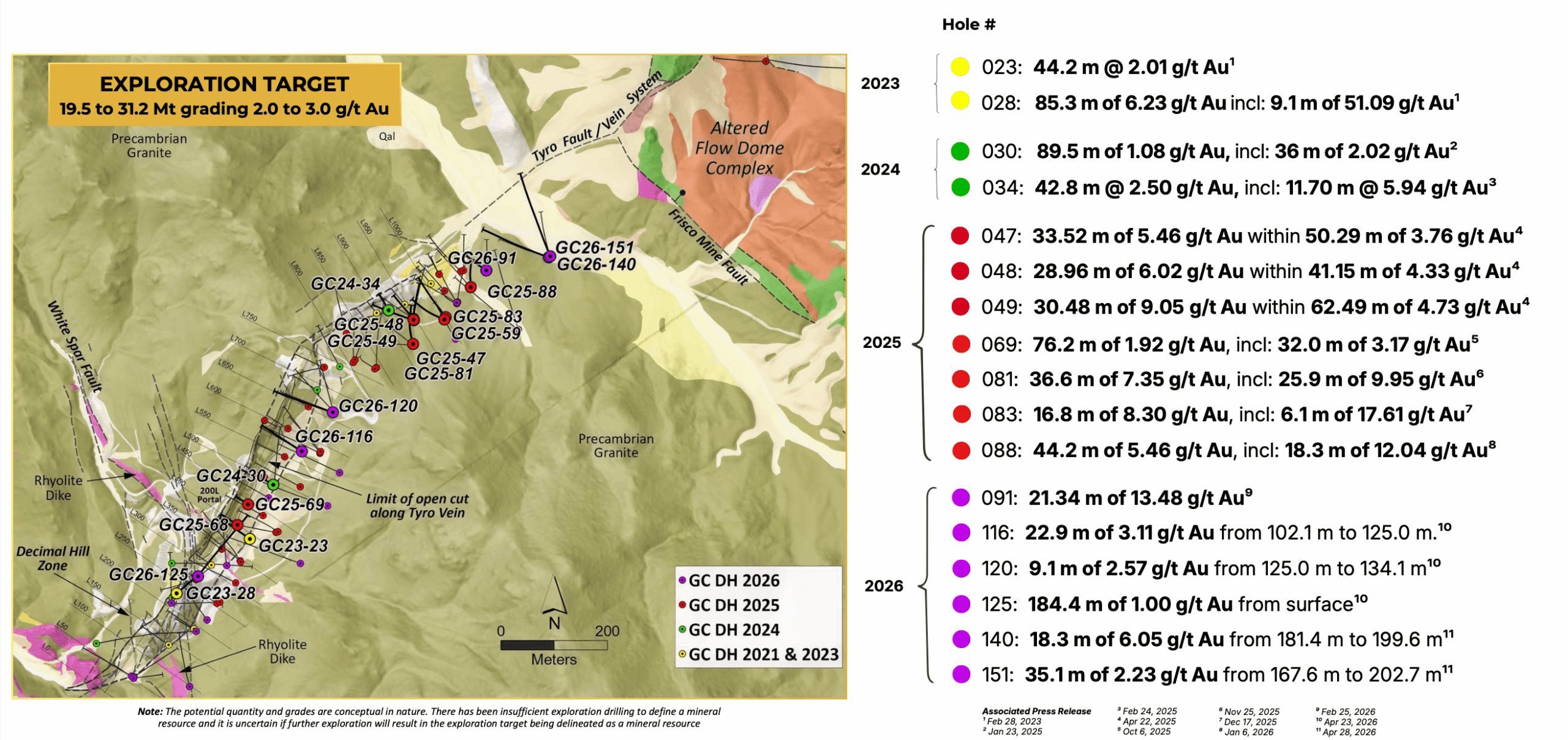

Earlier this quarter, West Point Gold released more strong drill results from the step-out holes that were drilled on the northeast part of the Tyro Zone, up to 140 meters to the northeast of previously reported results. That batch of assay results added about 100 meters of strike length (which now stands at 400 meters at NE Tyro) and 100 meters at depth to the mineralized volume as gold has now been intercepted as deep as 300 meters below surface.

And West Point Gold didn’t just find gold; it found high-grade gold. Assay results of 18.3 meters (17.5 meters true width) containing 6.05 g/t gold and 35.1 meters containing 2.23 g/t gold are excellent for what will eventually be designed as an open pit operation.

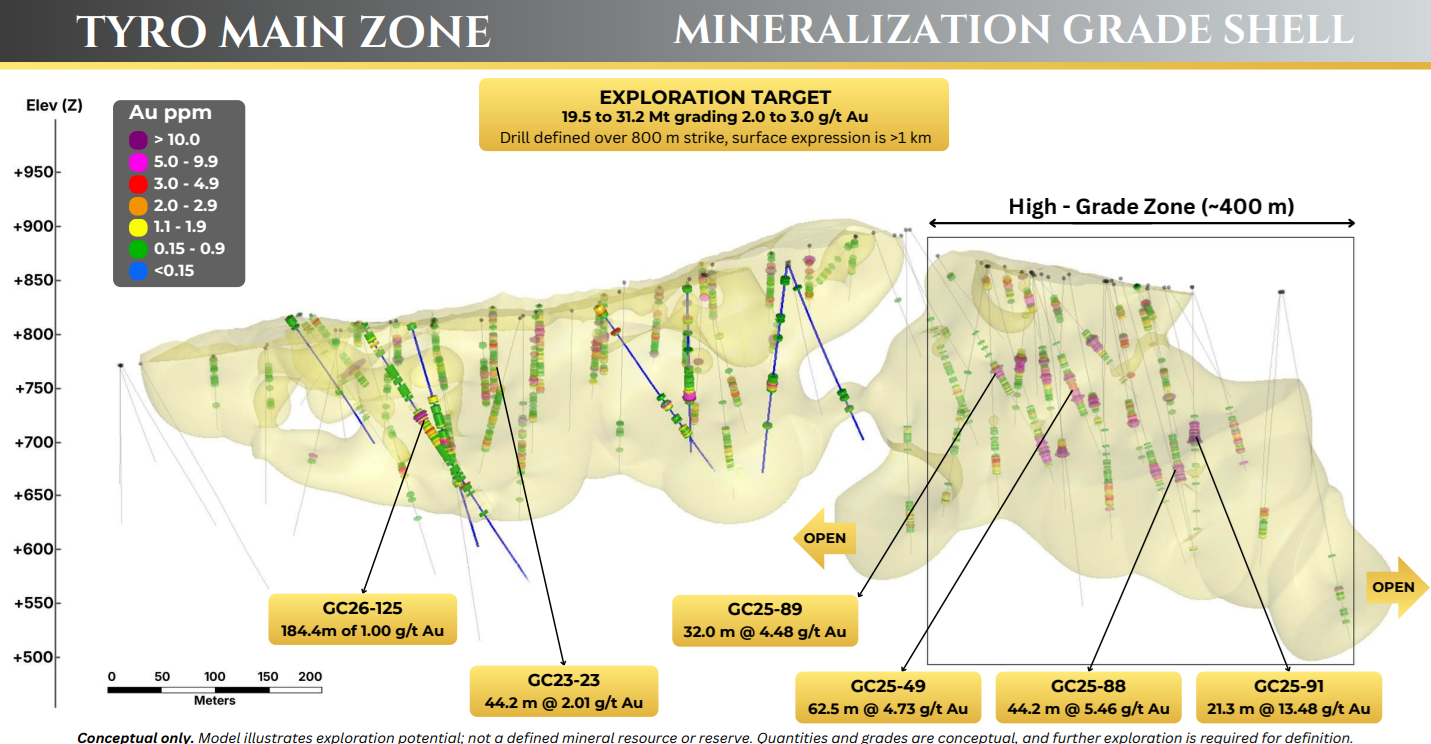

The expansion of the mineralization towards the northeast is of course a positive evolution before putting the resource together, but more importantly, the zone continues to expand towards the Frisco Graben.

Although the Frisco Graben will not be drill-tested this year, it remains an important exploration target offering blue sky potential. But as it’s a deep target and would require a few dozen drill holes to really get a better understanding of the mineralized structures, West Point is focusing on the ‘easier’ exploration targets in order to underpin its current valuation with a maiden resource calculation and subsequently, a PEA.

And the more drill results are rolling in, the more confident we are in seeing a maiden resource that may perhaps positively surprise the market. As mentioned numerous times before, the company is basically encountering underground-grade mineralization that should and will be open pittable in an economic scenario.

The recent drill results also validate the exploration target of 19.5-31.2 million tonnes at 2-3 g/t gold. We don’t expect the company to end up at the highest tonnage and highest grade, but 25-30 million tonnes at 1.8-2.2 g/t would result in a resource of 1.5-2.1 million ounces, and this would likely be a realistic target for a maiden resource.

The company is slowly ticking all the critical boxes in order to advance the project. Drill results are of course an important box to tick, but we are glad to see West Point Gold has also been making good progress on the metallurgical front. The next focus points (for us) will be on seeing an acceptable strip ratio (but the grade is of course very forgiving and at $4000 gold and an average grade of 1.5-2 g/t, even a double digit strip ratio should not be an issue) and more concrete development plans.

West Point Gold should be wrapping up its 20,000 meter drill program soon, and we expect assay results to continue to roll in throughout the summer. This will culminate in a maiden resource estimate at Tyro, which will contain a lot of useful data.

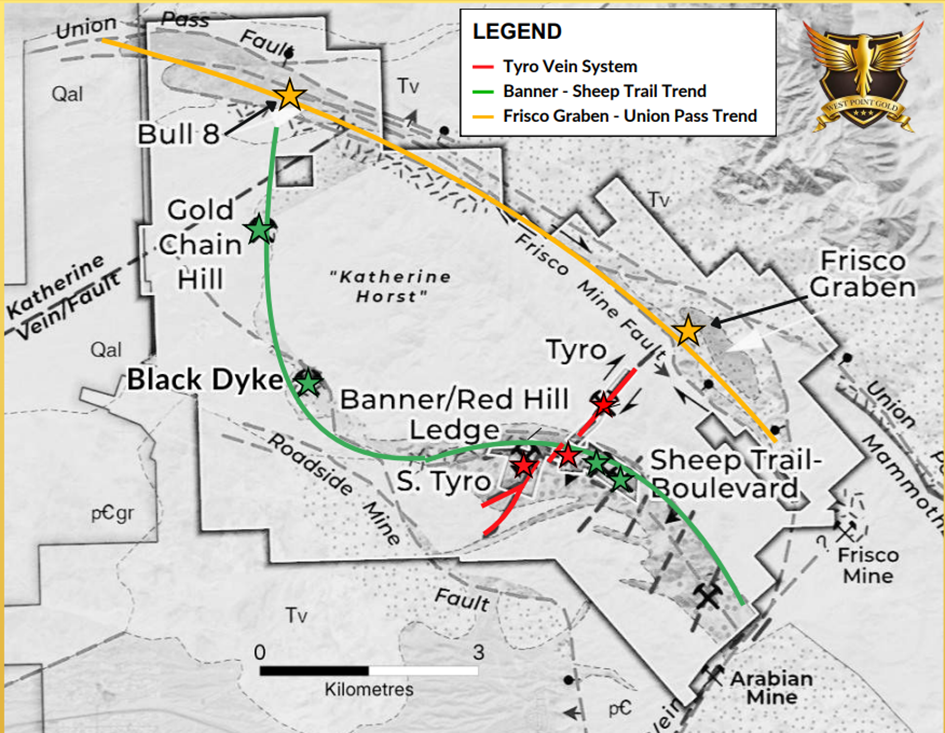

The Sheep Trail and South Tyro targets were confirmed with the newest drill results

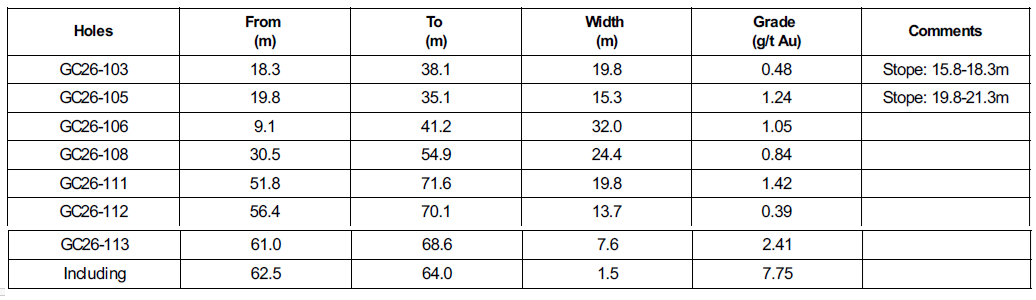

The company completed seven holes on the Sheep Trail target (which hosts the historical Sheep Trail mine which was discovered in 1865), and disclosed the assay results of those holes last month.

Those initial results are encouraging for a first pass drill program and at Sheep Trail, the drill bit encountered almost 20 meters of 0.48 g/t gold, 15 meters at 1.24 g/t gold and 32 meters of 1.05 g/t gold on the western part of Sheep Trail.

The three holes drilled on the eastern portion of the Sheep Trail target contained almost 20 meters of 1.42 g/t gold, just under 14 meters of 0.39 g/t gold and 7.6 meters containing 2.41 g/t gold including 1.5 meters of 7.75 g/t gold. As the table above shows, all seven holes encountered mineralization at very shallow depths. The company also completed nine holes on the South Tyro Vein system but did not encounter any meaningful gold results. The results indicate the gold deposition at South Tyro may have occurred at greater depths, and the company has ordered a geochemical analysis to figure out the next step at South Tyro.

Whole the grades encountered at Sheep Trail certainly are not as spectacular as the grades that have been encountered at Gold Chain, keep in mind these are still relatively high grade results for oxide gold assets in that part of the world. While the company isn’t close to putting a resource together at Sheep Trail, the first pass drill results definitely validated Sheep Trail as a good exploration target that could be considered to be a satellite to the Tyro Main Zone, further north.

We expect the company to continue to work on the exploration targets, but the near term focus should be and will be on pushing Tyro Main towards the maiden resource estimate.

Ticking another box: the updated metallurgical test work

One of the key elements before even thinking about putting an economic study together is of course completing a detailed metallurgical test program. It’s nice to sit on a gold deposit, but any deposit is worthless if you can’t get the gold out of the ground.

The company recently announced the results of a Phase 2 metallurgical test program on the Tyro Main Zone. The independent consultant tried out numerous potential processing possibilities and it has become abundantly clear that although Gold Chain is an oxide-hosted gold project, the ideal scenario is to work towards an economic model that includes a milling scenario.

While the anticipated recovery rates were between 39% and 69% in the HPGR crushed material and conventionally crushed material, the milled material reached recovery rates between 87% and 92%. The latter was achieved using a crush size of 0.075 millimeters and compared to recovery rates of 69% using a 1.7 millimeter crushing size, it should be clear that the smaller crushing size will make the most sense as gold recoveries are about a third higher.

Additionally, the milling scenario would also recover more of the silver (55%-83% versus the 27-68% in the HPGR scenario and 15%-62% in the conventionally crushed material scenario). While the recovery rate for the gold, which is the primary metal at Tyro Main, is more important, the Phase 2 metallurgical results appear to point in the direction of a conventional milling scenario. While CEO Derek Macpherson mentioned in his management comments that the multiple processing paths will continue to be tested, we think it is increasingly likely that by the time a decision has to be made, the milling scenario will make the most sense. Not in the least because the capex for a mill-based development should be reasonable given the project’s proximity to existing infrastructure while the high-grade nature of the project will allow for a reasonably ‘small’ mill without conceding too much on the output.

For instance, and this is purely arbitrary and not based on a potential scenario, putting 2 g/t material at an 85% recovery rate through a 5,000 tonnes per day mill would result in approximately 100,000 ounces of recoverable gold per year.

West Point is now fully cashed up

Although the company ended 2025 with a positive working capital position of in excess of US$5M (approximately C$6.5M), the management was smart enough to raise money in January, allowing it to bankroll all of its plans for 2026.

West Point Gold closed a brokered financing priced at C$1.10 per share (this was a warrant-free financing), raising a total of C$25M before fees, and approximately C$24.4M after fees. On top of that, the company issued 3.3 million shares related to warrant exercises, raising a total of C$1.4M. This means that in the first few months of 2026, West Point raised almost C$26M (net of fees). It still has approximately C$30M in cash on the balance sheet right now, so WPG shouldn’t have to go back to the market anytime soon.

There are still about 20 million warrants outstanding which would yield additional proceeds of approximately C$9-10M. 2/3rd of those warrants expire in 2026 with the remainder expiring in the first semester of next year.

Considering the share price is trading at about three times the highest warrant exercise price, we think it is fair to assume all warrants will continue to be gradually exercised, further bolstering the company’s cash and working capital position. This means the company won’t have to raise any money until (at least) the summer of 2027, unless of course a great opportunity arises and West Point Gold can capitalize on its high share price.

The C$1.10 financing will become free tradeable on June 20, but given the solid progress the company is making on its project, we don’t see this as a major issue as the stock was predominantly placed in strong hands. There may be some weakness around that date, but we expect any shares that would be sold will be absorbed by the market.

Conclusion

West Point Gold is diligently moving towards a maiden resource calculation on its Gold Chain project later this year and we expect that to be the basis for a maiden Preliminary Economic Assessment which should be completed in Q1 2027 (we expect to see a firm timeline guidance from the company once the resource will be published).

Given the high-grade nature of the project (an average grade of 1.5-2 g/t gold is to be expected given the higher grade pods in the mineralized system), Gold Chain could be a low-cost gold project in a Tier-1 mining jurisdiction and we expect the maiden PEA to reflect a high-IRR and high NPV to initial capex ratio.

The company took advantage of a financing window in January and raised C$25M and is now (more than) fully funded to complete the PEA on the project. We expect the NPV number at $3000 or $3250 gold to confirm the company is still trading at a relatively attractive valuation despite the strong run of its share price in the past year or so.

The next 12 months will be crucial to determine the strategic direction of the company. But the more high-grade drill results are rolling in, the more confident we are in West Point Gold’s prospects and potential.

Disclosure: The author has a long position in West Point Gold. West Point Gold is a sponsor of the website. This post is for educational purposes only; be mindful investing in junior mining stocks is risky and you may lose your entire investment if things go wrong. Please read our full disclosure.