An important update from Tocvan Ventures (TOC.C) hit the wires last week, as the company entered into a definitive agreement with Colibri Resources (CBI.V) to consolidate the ownership of the Pilar project in Mexico’s Sonora state.

As you may remember, Tocvan and Colibri initially had a 51/49 joint venture on two central/core claims, and after the initial exploration success, Tocvan expanded its area of interest by staking claims on a 100% ownership basis. The agreement with Colibri to now consolidate the entire area is a positive development as it makes the story easier to comprehend.

As Tocvan Ventures is also in the middle of a 20,000 meter drill program, we thought this was a good opportunity to touch base with CEO Brodie Sutherland.

Consolidating the ownership of the flagship Pilar project

Not only is it a positive development to see Tocvan consolidate the full ownership of the project, it is also great to see the terms are quite straightforward. No shares will be issued, and Tocvan acquires the 49% of the Main Zone claims for cash payments totalling C$3.6M and issuing a 1% NSR.

The initial C$2M cash payment will be completed on the closing date (and as Tocvan raised C$10M in the first quarter of this year, the company has the required cash on hand), followed by a final C$1.6M cash payment due one fir first anniversary of the closing date.

Tocvan will also issue the aforementioned 1% NSR, and while that NSR covers the entire Pilar project (including the expanded area that is already owned and controlled by Tocvan), there is a buyback clause. Tocvan is allowed to repurchase that 1% NSR for a C$1M cash payment at any given time (no deadlines, no expiration dates). On top of that, Tocvan also obtained a Right Of First Refusal should Colibri try to sell the royalty to a third party. This basically means that if a third party steps up the plate and wants to buy the 1% NSR for, say, C$600,000, Tocvan will be able to step in and repurchase the royalty at the same terms). Note this is a possibility for Tocvan, but the company is not required to match any bids. That being said, although it’s not a mandatory repurchase, we would expect the company to gladly pay up to C$1M as it may be able to re-market a 1% NSR for a higher price once Pilar is more advanced.

The recent exploration results at Pilar are encouraging

While the attention was drawn to the agreement to acquire full ownership of Pilar, we also shouldn’t forget the company is pretty much in the middle of a 20,000 meter drill program at Pilar. Tocvan Ventures has now completed almost half of this fully-funded drill program, but only released assay results of just 2,400 meters. This means that assay results of an additional 4,000+ meters are still pending, and in excess of 85% of the planned 20,000 meter drill program still has to be reported on.

This means we expect a busy summer for Tocvan as assay results will be reported on a regular basis. Some of the anticipated drill results will be low-hanging fruit but we also expect to see more news from the three new mineralized zones that were discovered earlier this year.

While we of course hope to see thicker areas of mineralization and/or higher grade results, we are encouraged to see the aggressive step-out drill program is bearing some results. Not only is this a further testament to the widespread oxide-hosted mineralization, it also provides additional drill targets for Tocvan to focus on.

Sitting down with Brodie Sutherland, CEO

Topic 1: Acquiring full ownership of Pilar

Congratulations on entering into an agreement to acquire full ownership of Pilar, as we think it’s an easier story for you to pitch versus having partial ownership on the core claims. May we assume there has been a lot of back-and-forth between Tocvan and Colibri and that in the end it only makes sense for the asset to be combined?

Yes, thank you. Consolidating 100% ownership of the original two Pilar mining concessions (the core of approximately 105 hectares hosting the Main Zone) is a transformative milestone. It removes the previous 51/49 joint structure entirely and creates a much cleaner, simpler story for investors, partners, and future financing or development decisions. We’ve maintained a constructive relationship with Colibri throughout, and this transaction aligns incentives perfectly; it allows us to capture 100% of the upside from the central high-grade area while streamlining operations across the entire Gran Pilar project.

The terms look pretty good with C$3.6M in cash payments and a NSR which you can repurchase and have a ROFR over. When will the title of the mining claims take place? After your initial payment on the closing date, or after the second payment has been fulfilled?

The terms are very shareholder friendly. Total consideration is C$3.6 million in cash, a repurchasable 1% NSR and most importantly, no shares will be issued to Colibri, so we don’t create an overhang for ourselves.

The title transfer you enquire about is very straightforward: The mining claims (currently held by Colibri’s Mexican subsidiary) will transfer directly to Tocvan’s Mexican subsidiary upon closing. This happens after the initial C$2 million payment and satisfaction of closing conditions, which allows us to move forward with project permitting at a much faster pace.

May we assume that now you have secured a clear and straightforward path towards full ownership of the two original Pilar mining concessions, more exploration will take place on those claims in the near future? Or will the focus remain on the Greater Pilar land package?

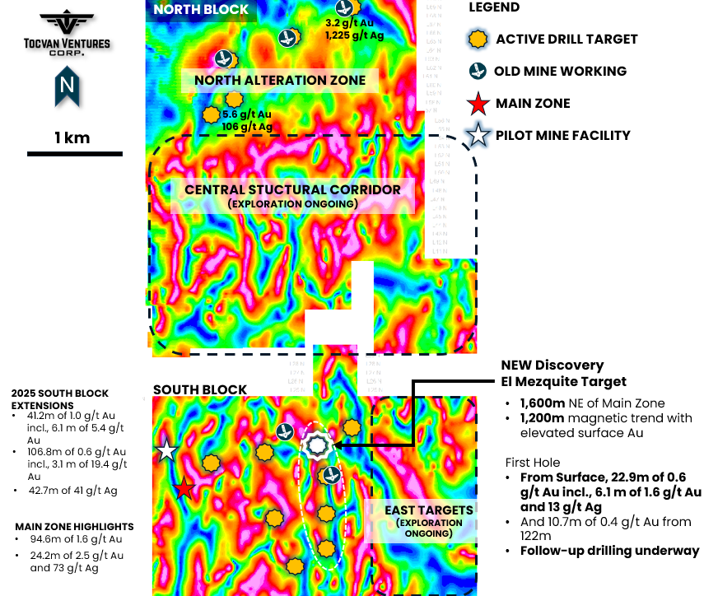

Full ownership of the core concessions simplifies and accelerates everything, including work on the original claims. There are numerous targets to follow up on there and there has yet to be a ‘deep’ drillhole (>200m) at the Main Zone. However, our strategic focus remains on the entire Greater Pilar land package (>21 km²). The original concessions host the Main Zone, which will anchor our maiden mineral resource estimate. At the same time, we are actively advancing high-priority expansion areas, across the North and South Blocks. Full ownership removes any JV friction and lets us move faster across the whole district-scale project.

How is the test mining phase going, any updates you can share?

The pilot mine is progressing well and remains on track for a 2026 start. As you may remember, we received full permit approval in August 2025 for a 10-year heap leach facility. The facility is designed to process 50,000 tonnes on the first pass with target parameters of ~1.2 g/t Au head grade and ~70% recovery. Development work (road construction, trenching, etc.) is already underway. Lab metallurgical test work continues to show strong leaching results. This pilot phase is designed to generate early cash flow (as we expect to recover 1,250-1,400 ounces of gold, subject to the actual head grade and recovery rates), de-risk the project, and provide valuable operational data while we advance toward a larger-scale operation. With gold prices well above US$4,000/oz, the potential economics look robust.

In March you also announced a collaboration with VRify Technology whereby the latter’s AI driven analysis should help to define additional exploration targets. Have you seen any good leads from this collaboration, or is it too early to tell?

We announced the partnership with VRIFY, to integrate their AI prospectivity mapping tool (DORA) and exploration intelligence software. The goal is to combine their AI with our extensive drilling, surface geochemistry, and geophysical datasets to generate and prioritize high-confidence new targets across our large land package.

It is still relatively early in the integration and analysis process, so we haven’t yet released specific new AI-generated targets publicly. However, we are optimistic about the collaboration’s potential to accelerate discovery. This work complements our ongoing field programs, including the new surface sampling results we announced on May 28, 2026, which outlined a promising new target area approximately 3 kilometers from existing zones. We expect VRIFY insights to help refine and expand our drill targeting in the coming months.

Topic 2: Corporate

While hindsight is always 20/20, you must be pretty pleased now that you raised C$10M in the February financing? We participated as well so while the share price has put in a disappointing performance since then, the cash allows you to do pretty much everything you want, including making the first payment to secure the Central Pilar claims?

We are pleased with the C$10 million bought deal financing (closed mid-February 2026 at $1.00 per unit). It was completed at an opportune time and has given us significant financial flexibility and a strong balance sheet. This capital directly supports the C$2 million initial payment for full Pilar ownership, our aggressive 2026 drilling campaign, pilot mine development, and general working capital, all while minimizing dilution. We greatly appreciate the support from long-term shareholders and are using the cash to advance and improve the Pilar project.

How much cash do you anticipate to have in the treasury after completing your 20,000 meter drill program and the initial C$2M cash payment to Colibri? We note you also received almost C$850,000 in March and April from the Sorbie settlement and some warrant exercises.

We entered 2026 in a strong financial position thanks to the C$10M raise plus ongoing positive cash inflows. The Sorbie sharing agreement has continued to deliver meaningful periodic settlements (including strong contributions in recent months), and we have seen warrant exercises that further bolstered the treasury. After funding the initial C$2M Colibri payment and completing the current phase of drilling, we expect to maintain a strong cash position into the end of the year. This will comfortably support ongoing exploration, pilot mine construction/commissioning, and general corporate needs. We are fully funded for our near-term catalysts without immediate financing pressure.

There were 1.7M warrants exercisable at C$0.90 that expired in June (and an additional 4.9M warrants at C$1.20 and C$1.30), have you seen any of those 90 cent’ers come in when your share price spiked in June?

There were warrants expiring in June 2026 (including a series with a C$0.90 exercise price). A total of 6.6M warrants expired. Total warrants that currently remain outstanding has now decreased to less than 20M.

During periods of share price strength earlier in June, we did see some warrant exercises across our outstanding warrants, which contributed positively to our treasury.

More catalysts are around the corner

What can we expect next from Tocvan?

Drill results, drill results, drill results. The company is now almost halfway its 20,000 meter drill program at Pilar, and it hasn’t released assay results in a while. With a backlog of thousands of meters of drilling, we expect Tocvan to step up the pace in publishing assay results from its drill program. The news flow should continue for the next several months.

With the activities related to the pilot plant picking up, we anticipate to see Tocvan publish more updates on this matter too. While 50,000 tonnes of rock to be processed doesn’t sound like much, it will (read: should) yield in excess of 1,000 ounces of gold which can be sold. But more importantly, it will get the company real-world data on its recovery rates and metallurgical expectations. We don’t care about the 1,000+ ounces, but the data from the met work is important.

Upon completing the drill program, Tocvan is expected to release a maiden resource calculation at Pilar, likely to be followed by a Preliminary Economic Assessment. We consider the maiden resource and PEA to be major milestones for the company, as this will be the first time something tangible will be published to determine a fair value for the company’s flagship asset.

But in any case, you should expect a flurry of drill results to be published in the near future.

Conclusion

We think Tocvan’s decision to consolidate full ownership of the Pilar project is a smart strategic move. Not only will this make it easier for CEO Brodie Sutherland and his team to tell the story, it also makes any decision making process easier. We expect this transaction to close soon, and the attention will then move to a continuous stream of exploration news and perhaps some updates on the pilot plant progress.

We are still hopeful to see a maiden resource after completing the current 20,000 meter drill program, but as we explained earlier, we think it is important to reach the critical mass to warrant further development at Pilar.

Disclosure: The author has a long position in Tocvan Ventures. Tocvan Ventures is a sponsor of the website. This post is for educational purposes only; be mindful investing in junior mining stocks is risky and you may lose your entire investment if things go wrong. Please read our full disclosure.