A few weeks ago, Integra Resources (ITR.V, ITRG) published its long-awaited feasibility study on its producing Florida Canyon gold mine in Nevada. This is the first Integra-provided study since the company acquired the mine in 2024, and provides additional data from the substantial drill program and operational knowledge acquired over two years of production. And drilling has shown to pay dividends for the company in terms of resource and reserve growth.

This increased the total resources, extended the mine life and will allow Integra to continue to hoard cash in the current price climate with gold still trading around $4000/oz.

In this update we will have a closer look at the feasibility study and what this means for Integra as a company in the next three years.

The key elements of the Florida Canyon feasibility study

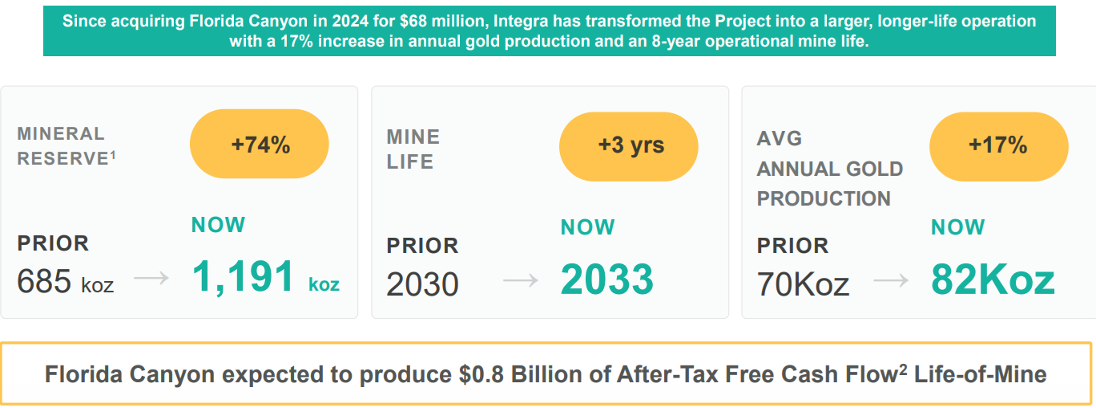

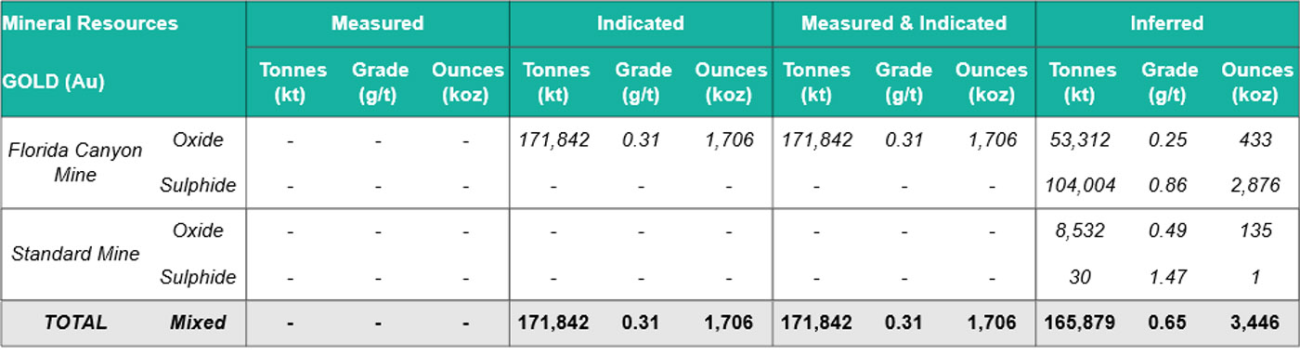

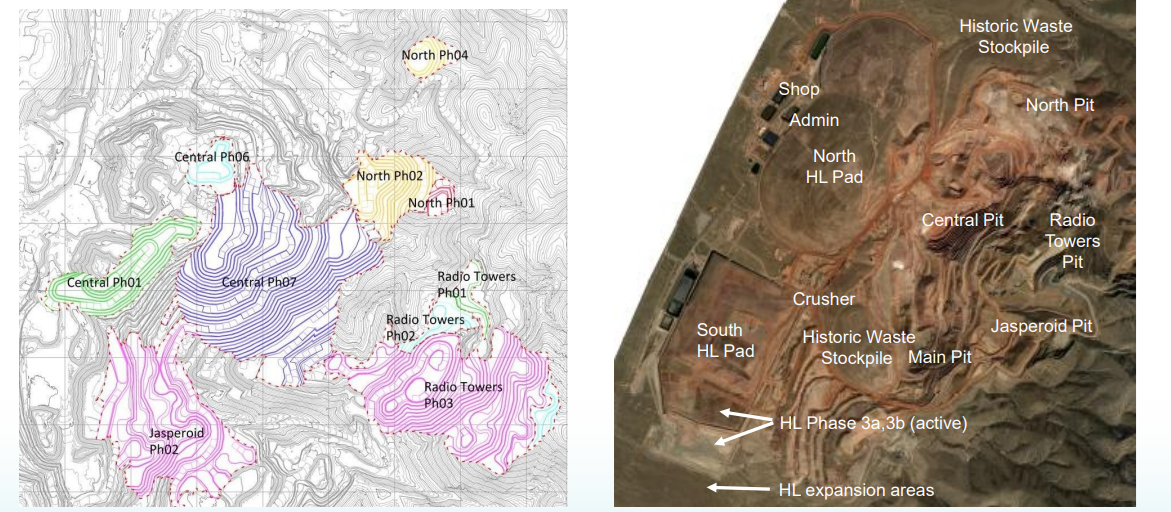

Integra Resources included the data from its drill programs along with updated geotechnical assessment and operating experience at Florida Canyon, resulting in a noticeable increase in the resources. The measured and indicated resources at Florida Canyon currently stand at 1.7 million ounces with an additional 433,000 ounces of gold hosted in oxide material in the inferred resource category. The updated resources now also contain a maiden resource on the past producing Standard Mine (located just 6 kilometers south of the Florida Canyon mine) with a maiden inferred resource of 135,000 ounces of gold.

The latter comes with an average grade of 0.49 g/t which is substantially higher than the Florida Canyon grades, so it will be interesting to see if and when Integra Resources is able to bring this resource into the mine plan. Integra will commence drilling at Standard in the next few weeks, so hopefully this will allow the company to further expand the existing resource there. The 2.9 million additional ounces of gold in the sulphides are not taken into consideration right now, as Integra continues to focus on the heap leachable material available at Florida Canyon and the 1.1 million ounces in the reserve category.

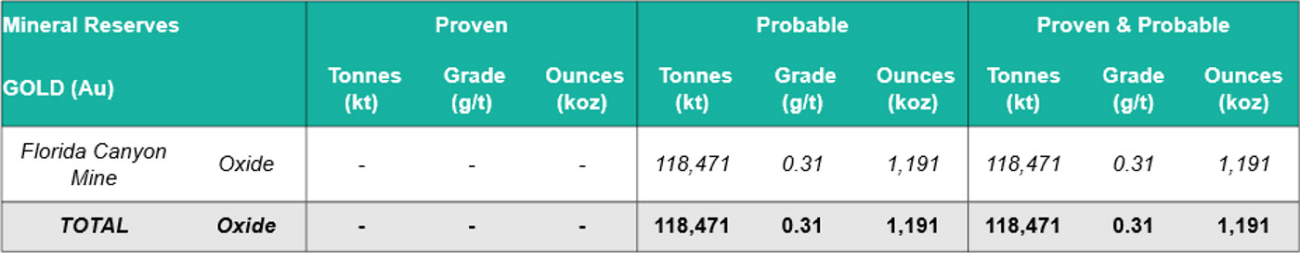

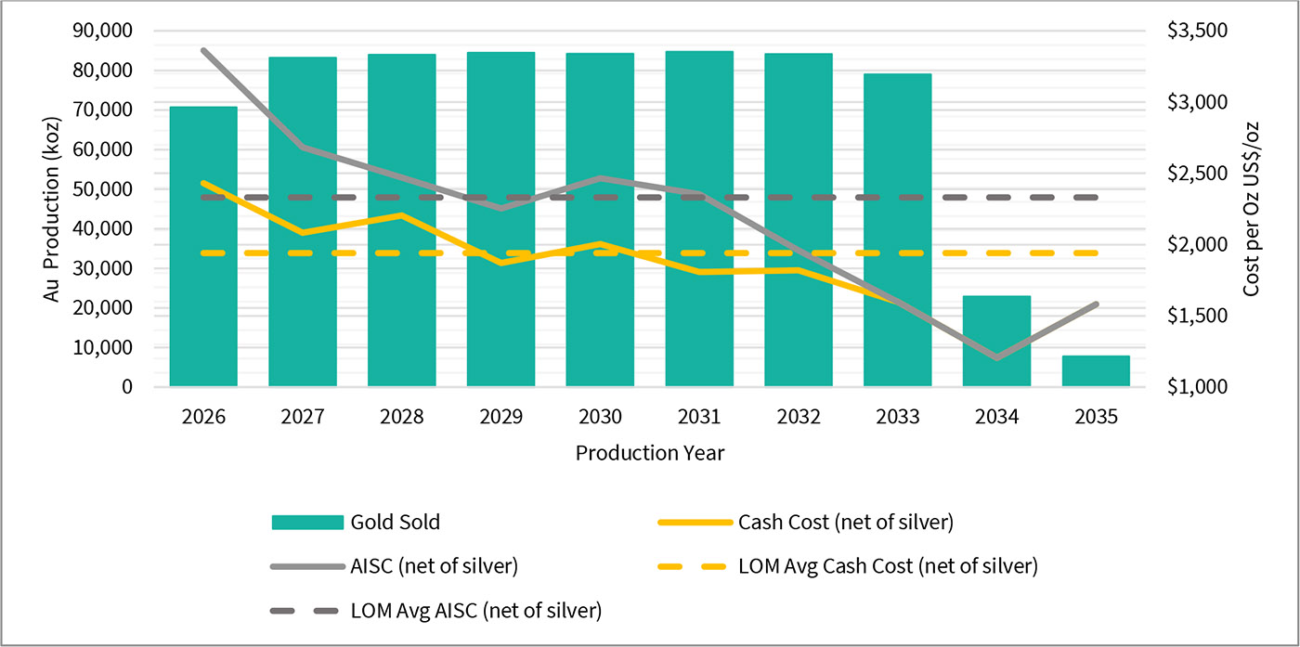

For now, the attention remains on the 1.7 million ounce measured and indicated resource at Florida Canyon, where the updated mine plan now anticipates an average production of just over 80,000 ounces of gold per year over an 8 year period. That gold is expected to be produced at a cash cost of $1940/oz and an average all-in sustaining cost of $2331/oz over the entire mine life.

As no initial capex is required (the mine is of course already in production), the economics look great. The mine is expected to generate a total net free cash flow of just under US$770M during its remaining mine life, and it is important to note Integra’s consultants used a degressive gold price. We should note that the significant cash-flow generation will come just as the company will be building its key asset, DeLamar. It can use this cash-flow to help fund the DeLamar mine construction, when it comes. And Nevada North thereafter.

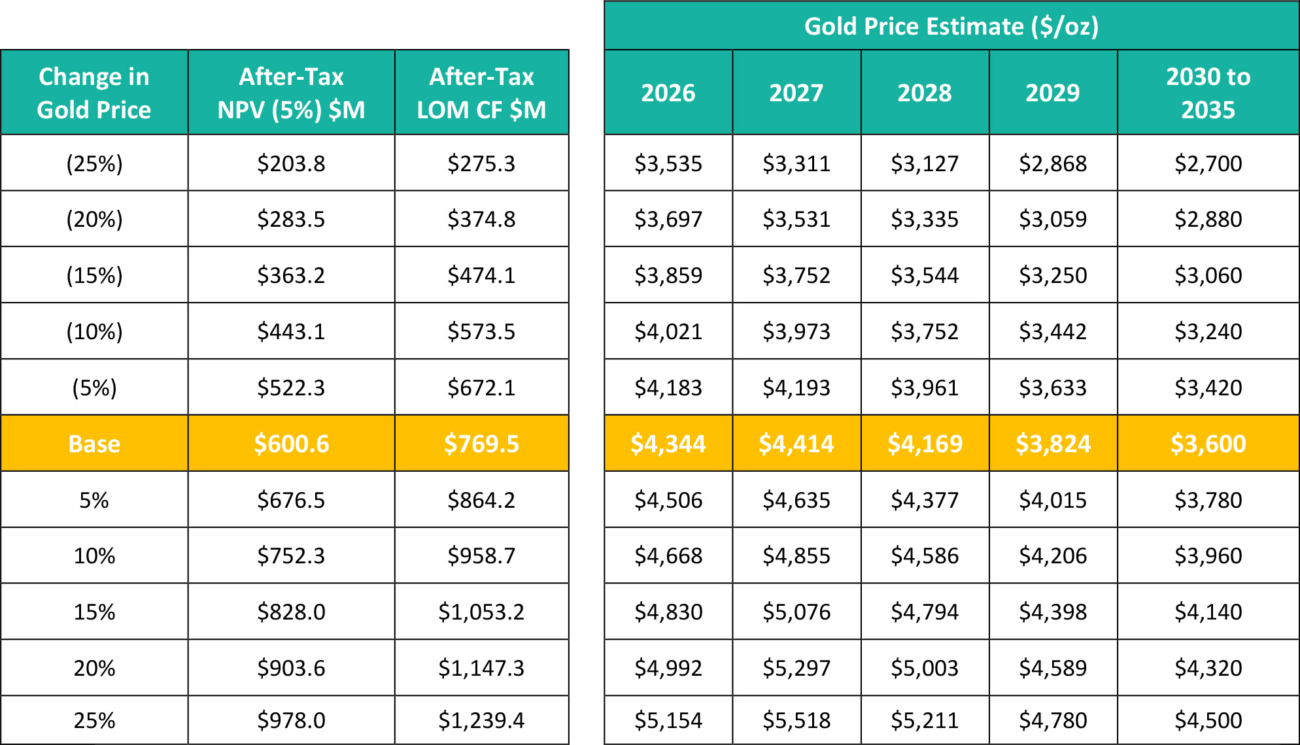

Whereas an average gold price of $4344/oz is used for this year and $4414/oz for next year, the anticipated realized gold price decreases by a mid to high single digit percentage, to land on a flat price of $3600/oz from 2030 on until the mine is exhausted.

As the mine is of course cash flowing right away, the ratio of NPV5% to net free cash flow is very high, at almost 80%. With an anticipated after-tax NPV5% of US$601M at the aforementioned average realized gold prices, the Florida Canyon mine represents a value of US2.96 per share (for a CAD-equivalent of C$4.20). Not only does this emphasize the point we made in previous coverage (Integra is fairly valued based on just Florida Canyon, and you get all other projects basically thrown in for free), the economics also hold up in a lower gold price environment.

The sensitivity analysis shows that even using a 10% lower gold price (which means a sub-$3300 gold price from 2030 on), the after-tax NPV5% of Florida Canyon would still be US$443M. And if you are a gold bull and expect to see a gold price closer to $5000/oz for the next three years, the +10% scenario indicates an after-tax NVP5% of US$752M, or C$1.07B for C$5.26 per share (US$3.71).

While an 8 year mine life sounds pretty short, remember Integra Resources acquired Florida Canyon in 2024 on the premise of a remaining seven year mine life. So now, two years later, the company has not only replenished the resources and reserves it has mined, it added another year to the active mine life for a net positive impact of three years (plus two years of residual leaching).

There are plenty of additional opportunities to further extend the mine life. The inferred resources at Florida Canyon and the Standard Mine could be low-hanging fruit (if even just half of that tonnage could make it into a mine plan, the mine life could be extended by another two years), while Integra Resources will kick off a 42,500 meter exploration program specifically focusing on exploration opportunities.

The study confirms the AISC will continue to trend down in the next few years

As this is the first economic study commissioned by Integra (the previous economic study was completed by the previous owner of the mine), there are some differences. In the previous segment we discussed the positive developments (a substantial increase of the mine life), but given the impact of inflation in the entire mining sector in the past few years, the operating costs will come in a bit higher than originally anticipated.

On the back of the publication of the feasibility study, Integra Resources also revised its all-in sustaining cost guidance for this year. The midpoint of the guidance increases from $2850/oz to $3400/oz (up 19%) with the updated AISC guidance providing a range of $3300-3500/oz while the production guidance remains unchanged at 70,000-75,000 ounces of gold.

It is what it is, and Integra should be happy the gold price is where it is. Also, Integra is choosing on its own accord to accelerate mine-site expenditures this year, as opposed to deferring until next year, so they can get into better grades, quicker, in the Central Pit area. It really is short-term AISC pain for longer term gain, better margins and lower costs. But the image below confirms one of the key elements we have been discussing for the past eighteen months. 2026 should be the final year of disproportionally high all-in sustaining costs as Integra Resources played ‘catch-up’ and has been able to deploy the ample incoming cash flow to complete all investments required to keep the operation humming along nicely.

But the key takeaway can be found in the image below. The gray line indicates the AISC per ounce of gold, net of by-product credits (there is a silver credit, but it’s quite negligible as it has an impact of less than $50 per produced ounce of gold).

You immediately see the expected decrease of the AISC to $2750/oz in 2027, on the back of a production increase to just over 80,000 ounces of gold. That’s a very substantial reduction of $650/oz, and this will be followed by further reductions in the coming years.

And just to give you an idea of the importance of the expected AISC decrease. Selling 70,000 ounces at $4250/oz in 2026 would generate a mine level net cash flow (pre-tax and pre-overhead) of approximately US$59.5M based on an average AISC of $3400/oz.

But even if we would use a lower realized gold price of $3750/oz in 2027, the combination of a lower AISC and higher production would generate a net mine site cash flow of US$80M, a 33% increase.

So, long story short, the AISC will be higher than anticipated in the next few years, but with gold holding the $4000 handle for now, the margins will remain robust and are set to expand in the next few years. And we will effectively see a noticeable and substantial reduction in the AISC, reaching just $2250/oz by 2029.

Conclusion

Integra certainly got a lot of “bang-for-their-buck” on the Florida Canyon asset acquisition, paying only $68 M for the asset (actually less, given the cash it came with) and projecting an 11x return on that purchase price according to the feasibility study.

At the end of the first quarter, Integra Resources had a net cash position (defined as cash minus the (in this case non-existent) debt) of US$106M and a positive working capital position of almost US$140M.

This means the fair value of the company based on the base case scenario for Florida Canyon in combination with the existing net cash position represents approximately US$3.5 per share (around C$5/share). Not only does this mean the current share price represents a significant discount to the fair value as per the official feasibility study and existing net cash position, it also means you still get all the other assets for free. And one of those assets, DeLamar, which just completed its 30-day public comment period as part of the NEPA process, is one of the most advanced permitting stage gold deposits in the US right now. As permitting advances, risk discounting of DeLamar should also decrease in lock-step.

And as a reminder, as per the official studies (a 2025 feasibility study for DeLamar and a 2023 PEA for Nevada North), the after-tax NPV5% on those projects is respectively US$1.15B for DeLamar at $3500 gold and US$463M for Nevada North at $1950 gold (how times have changed).

Disclosure: The author has a long position in Integra Resources and recently bought more shares on the open market. Integra Resources is a sponsor of the website. This post is for educational purposes only; be mindful investing in junior mining stocks is risky and you may lose your entire investment if things go wrong. Please read the disclaimer.