When District Metals (DMX.V) acquired the Viken polymetallic deposit in Sweden, it didn’t come as a surprise to see that this alum shale hosted a multi-billion ton resource containing about a dozen elements from the periodic table. As the Swedish government still had a ban on exploring for and mining uranium, the project came out of the gate as a vanadium deposit but since the Swedish government has lifted the moratorium on uranium exploration and mining it has become clear that this project could become one of the most important sources of uranium in the European Union.

Subsequent to releasing an updated mineral resource estimate in April 2025, the company worked towards putting an updated Preliminary Economic Assessment (PEA) together as the moratorium on uranium mining has been lifted. As per the initial study, the Viken project could produce approximately 3.3 million pounds of uranium per year which would fully cover the domestic demand in Sweden. On top of that, as there are very few economically viable uranium projects in the European Union, the Viken project could play a pivotal role in the EU’s plan to increase its independency from non-EU energy sources.

In this report we will have a closer look at the PEA and the implications for District Metals as a company, and Sweden as a nation.

The PEA: a first look

The company released the results of its PEA on the Viken project earlier this month, and we have to say the results are better than we had anticipated. While we are still waiting to see all the details in the technical report, the initial publication already provides plenty of data.

In our previous reports on District Metals we mentioned that the Aura Energy economic study on its Haggan alum shale deposit would be a good reference for what we might expect from district. Fortunately District elected to go for a much larger production scenario and now anticipates an average annual production of 3.3 million pounds of uranium per year.

The economic study also takes a very substantial by-product credit into consideration as SOP ( fertilizer) and vanadium (in the form of vanadium electrolytes and ferrovanadium) turn out to be two very important byproduct credits. Additionally, the project will also produce some zinc, some nickel and molybdenum which we consider to be the ‘secondary’ byproduct credits. Still important and a contributor to the NPV, but less important than the Vanadium and SOP related revenue.

The PEA is based on a production scenario with a 10 million ton per year capacity for an initial mine life of just under 13 years. Given the multibillion ton resource statement on the Viken project, readers are cautioned that the total resource included in the mine plan represents less than 3% of the overall Viken mineral resource estimate on the property. So while the IRR and Net Present Value look great, District Metals is still just barely scratching the surface and we should consider the PEA to be a starting point and a stepping stone more than a ‘limited’ production scenario.

It also makes sense to keep the phase one mine life limited to 13 years. Using a discount rate of 8% indicates the cash flows in the 14th year of the mine life would be discounted by almost 70%. This means that every $100M in net free cash flow would be discounted and only contribute $31M to the NPV. So keeping the mine life to 13 years does not profoundly impact the NPV in a negative way.

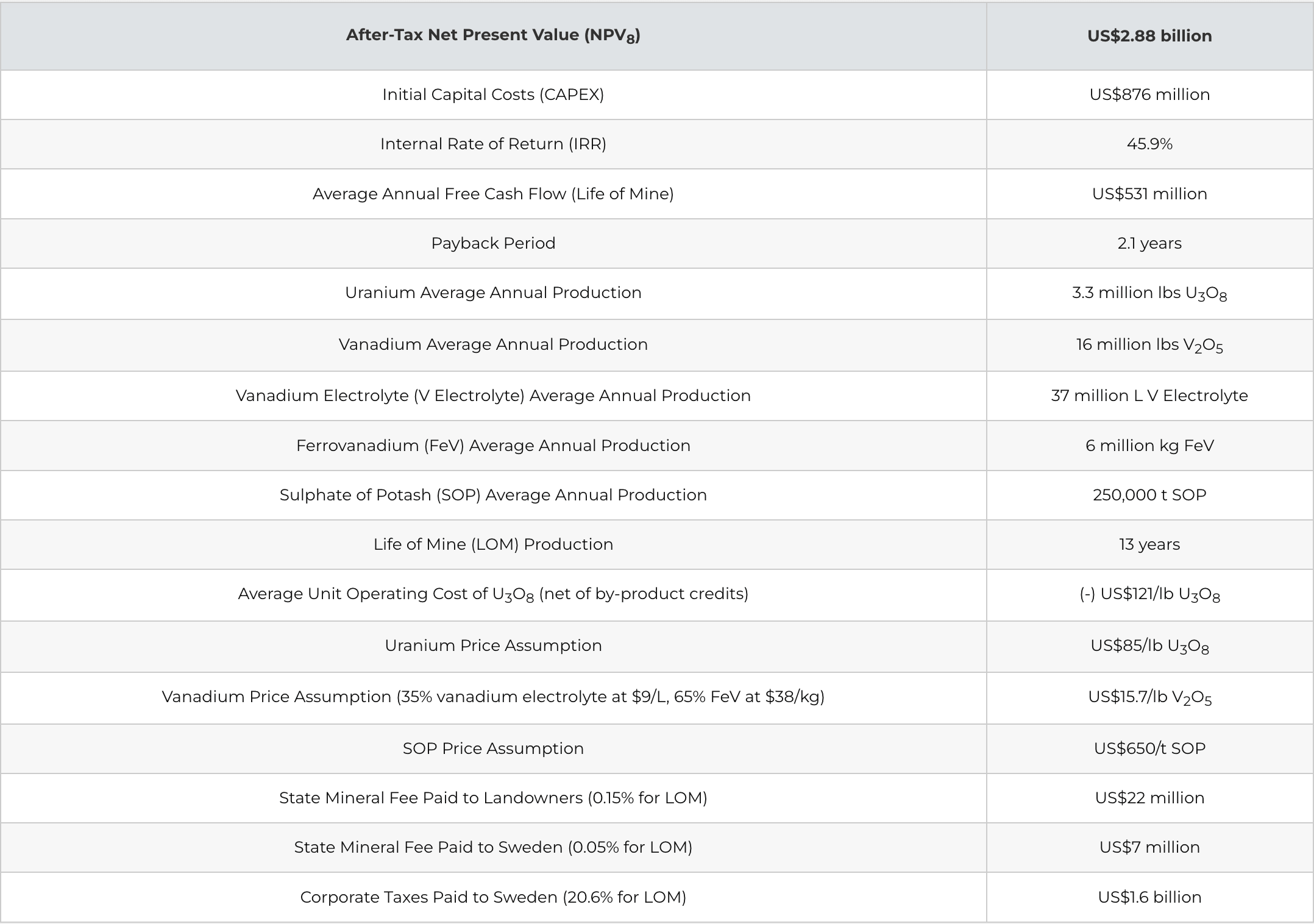

A throughput of 10 million tons per year will result in an annual production of approximately 3.3 million pounds of uranium per year, as well as 16 million pounds of V2O5 equivalent. As the price for just vanadium pentoxide is pretty low these days, District Metals made the smart move to produce premium vanadium products. The company now expects to produce approximately 37 million liters of vanadium electrolyte per year as well as 6 million kilograms of ferrovanadium per year which would fetch prices of respectively $9 per litre and $38 per kilogram. This would result in a combined V2O5 received price of approximately US$15.70 per pound.

On top of that, the Viken alum shale project is expected to produce 250,000 tons per year of sulphate of potash (‘SOP’) which could be sold at approximately US$600 to US$700 per ton (the PEA uses US$650/t as the average sales price).

The project will also produce 4.5 million pounds of molybdenum per year, 1.6 million pounds of nickel as well as 2.1 million pounds of zinc. These three elements will definitely contribute to the overall economics of the project but they’re clearly not as important as the vanadium and the SOP production.

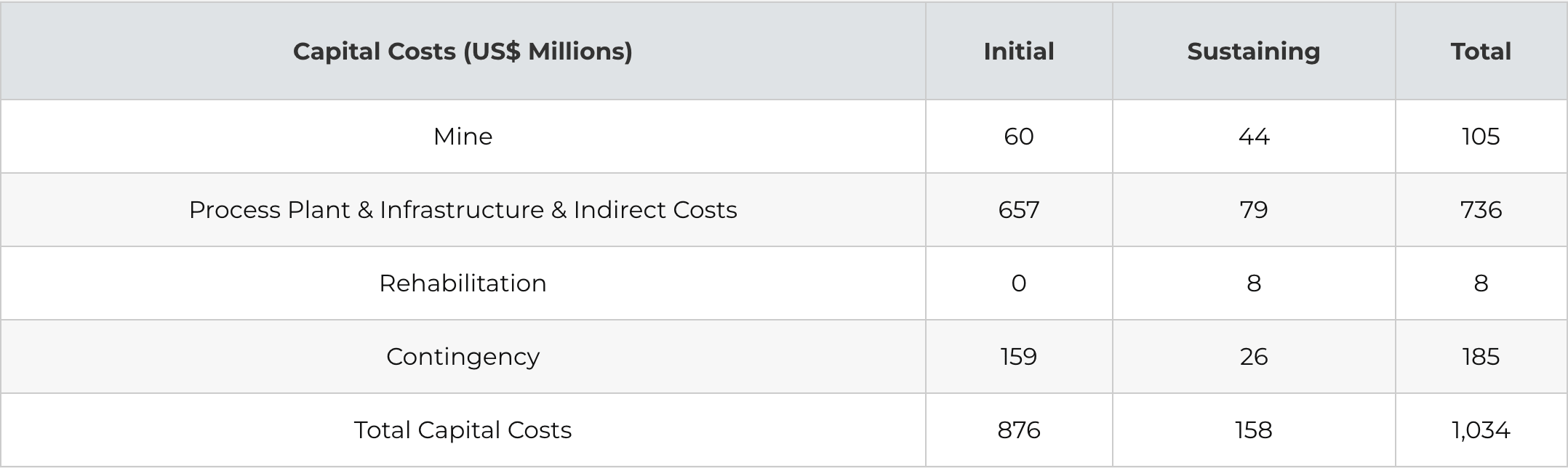

The initial capital expenditures are estimated at US$876M (which includes the investments required to produce value-add vanadium products), and given the abundance of byproduct credits, the net cash cost per pound of uranium (net of the aforementioned byproduct credits) is a negative US$121 per pound.

It goes without saying that a negative cash cost, let alone a triple digit negative cash cost, has a tremendously positive impact on the economics of the project. Using a base case uranium price of $85 per pound (perhaps a bit high, but in line with or even on the lower end of the base case uranium prices used by its peers in recent studies), the after-tax internal rate of return (‘IRR’) comes in at just under 46% while the after tax net present value (‘NPV’) discounted by 8% per year comes in at an astronomical US$2.9B, which is roughly C$4B at today’s exchange rate. And we would like to emphasize once again that the total amount of resources included in the mine plan represents under 3% of the total resource on the Viken project.

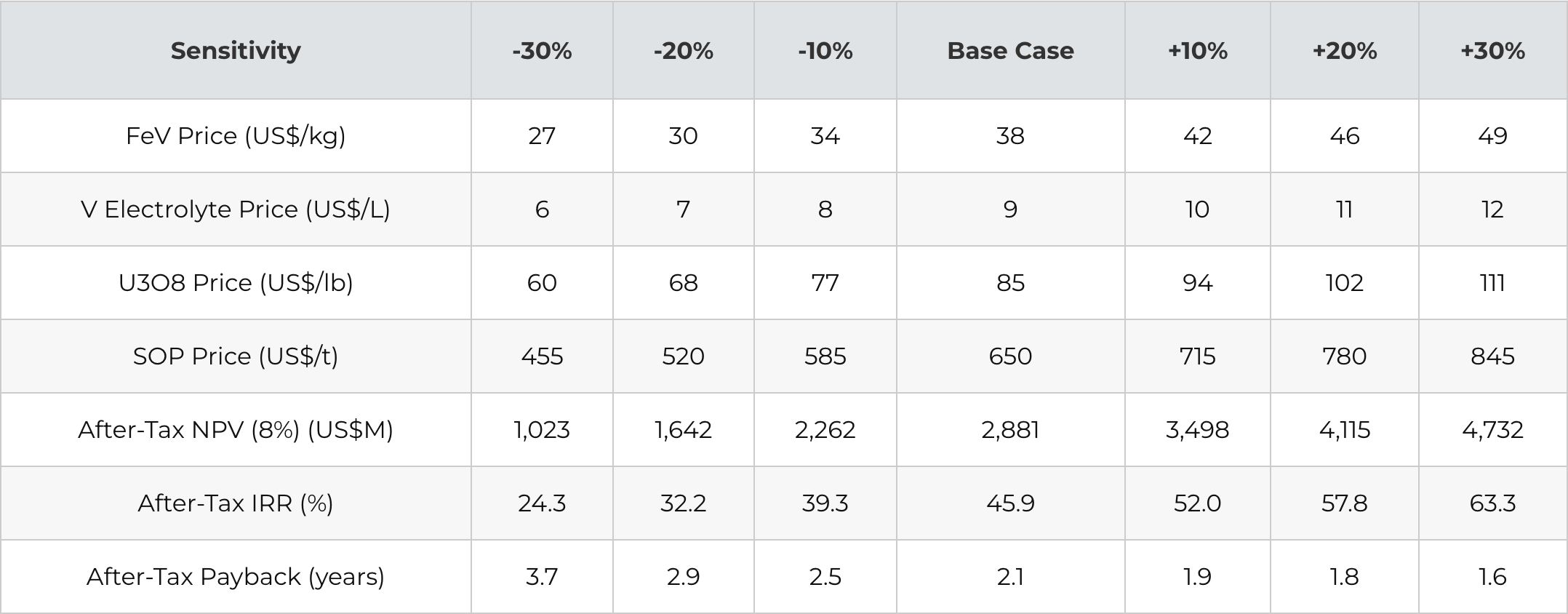

The company also provided a detailed sensitivity table allowing investors to have a look at what happens with the economics when the commodity prices decrease by 10%, 20% and 30%. As the table below shows, even in the conservative scenario with a 30% lower commodity price across the board (including a uranium price of approximately $60 per pound), the after-tax net present value discounted by 8% still exceeds US$1B (C$1.4B) while the after-tax internal rate of return comes in at 24%.

It is a pity that it’s a bit more difficult to isolate the impact of a price change per commodity as it would have been interesting to use a – 30% scenario for the vanadium but only a 10% lower uranium price as part of stress-testing the economics. As the press release obviously only offers just a summary of the economics, we expect the technical report to contain much more useful data including a better insight on the vanadium electrolyte and ferro vanadium products.

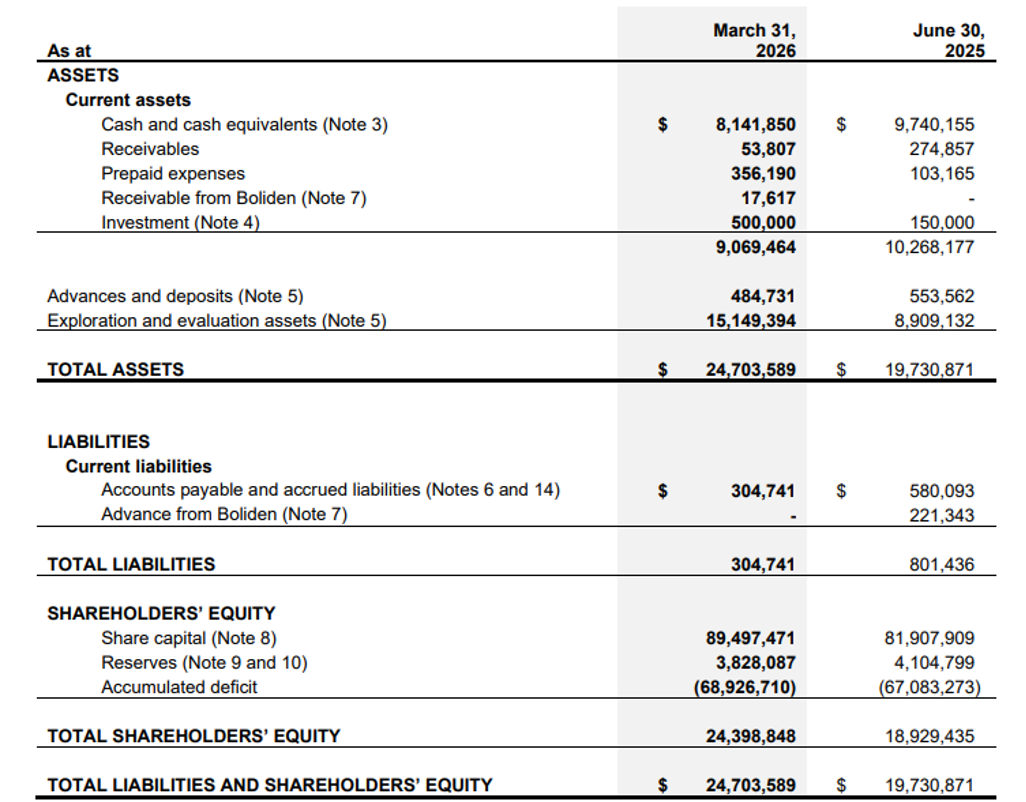

The company is cashed up after the recent raise

Earlier this quarter, the company raised C$10M in a no-warrant financing priced at C$0.68 per share. The vast majority of these shares are placed in Sweden while 100% of the offering appears to have been placed in Europe (as Pareto Securities earned a 5% finders fee and no Canadian brokers were mentioned). Not only does this provide the company with additional exposure to European investors and vice versa, not having to issue warrants is definitely a positive feature.

This financing will nicely top up the treasury which already had a positive working capital balance of approximately C$8.7M at the end of the first quarter. While we still have to wait for the company to file its financials for the second quarter, we estimate District Metals to currently have a positive working capital position exceeding C$16M.

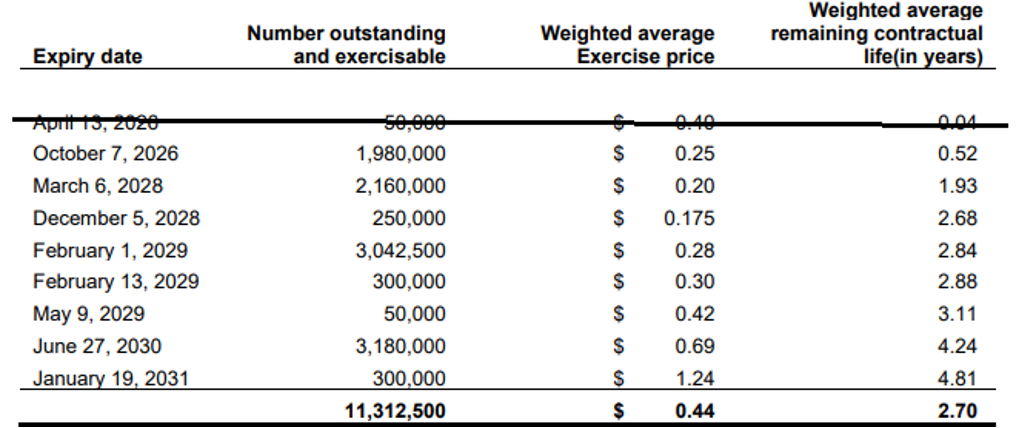

It’s perhaps also worth noting that there are 6,045,500 warrants with a strike price C$0.30 due to expire in February 2027 that should bring in approximately C$1.8 million. The next expiry date for options are the 1.98 million options with an exercise price of C$0.25 expiring in approximately 4 months from now (shown above). If and when exercised, these will bring in an additional C$0.5M.

What’s next for District?

Completing the PEA was an important step for District Metals, but that doesn’t mean the company will sit on its hands. We can expect the Economic Impact Study to be published in the next few weeks, and this will highlight the positive economic impact the project will have on the local economy, as well as the Swedish economy. And within the next few weeks, we also expect/hope to see the Viken project to get the ‘project of national interest’ designation.

The company will also remain active on the technical front. Not only do we expect to see the company getting active on the other alum shale properties, we also expect to see a drill program on the Viken project.

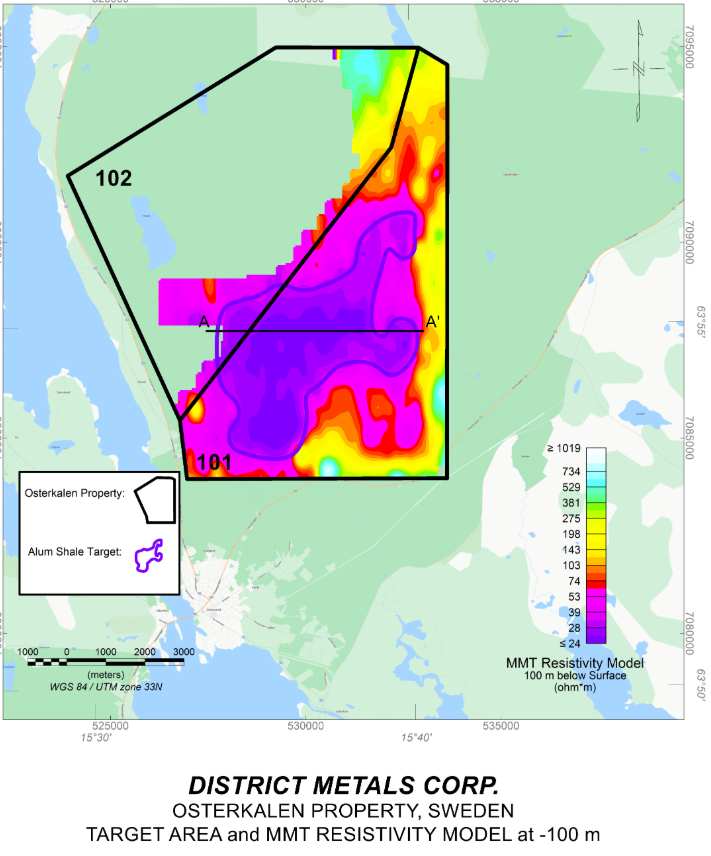

And as the company announced earlier this week, the Österskälen alum shale project will be drilled before Viken. A drill permit has been received and a drill contract has been awarded, with the drill rig expected to arrive on site within the next few weeks. The total amount of holes and meters has not been disclosed yet and will depend on the actual exploration success.

The drill program will test a large MobileMT geophysical conductive anomaly that was identified in 2025, which, in combination with other elements, makes the project prospective for alum shale exploration. With a total size of 8 kilometers by 3.5 kilometers, this also represents a sizeable target which hopefully hosts a Viken-style mineralized system.

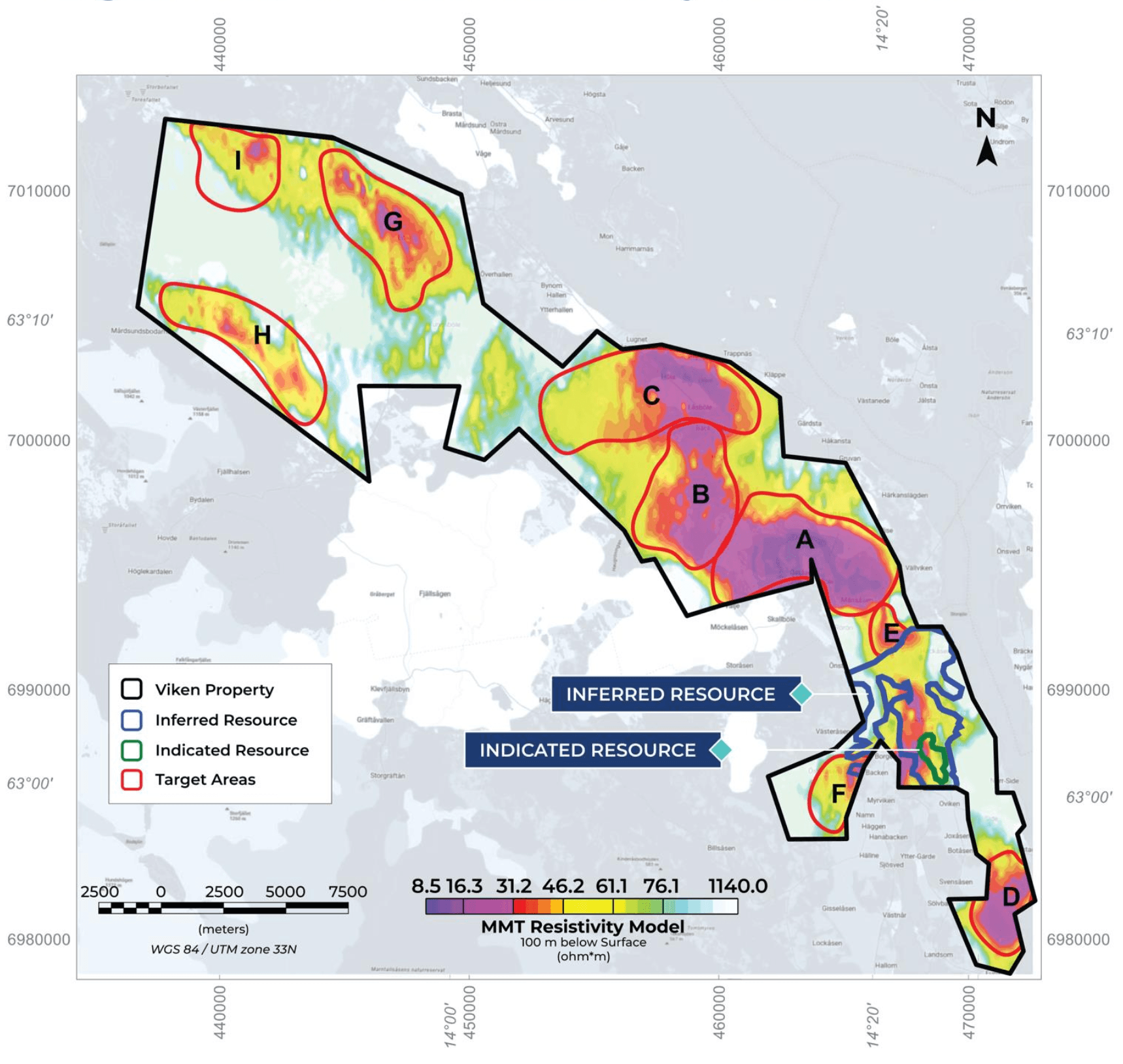

Once the Österskälen drill program will be completed, we hope to see more details on a Viken. That drill program will likely not focus on the existing resource and the area where the PEA was focusing on, but as the image above shows, a recent geophysics program has highlighted about half a dozen high priority targets, with some of those targets presenting larger opportunities than Viken. It’s our understanding CEO Garrett Ainsworth and his technical team are chomping at the bit to drill-test ‘Target Area A’.

Just to be completely clear, the Viken PEA includes just 3% of the total resource. No additional resources are needed to continue to advance Viken towards a feasibility study and a construction decision, but it would be interesting to have several resources on the Greater Viken area. After all, it would technically be feasible to simultaneously mine several areas if that would turn out to be the best approach. And with the recent positive political developments (see below), District Metals is in an excellent position to help Sweden unlock its raw materials potential.

Conclusion

Since the acquisition of the Viken project, District Metals has diligently worked towards an updated resource estimate which was published last year, and now the moratorium on uranium mining in Sweden has been lifted, the recently published PEA was the next logical step.

We are glad to see that the company is not just going to produce a ‘standard’ vanadium pentoxide product but it has elected to go the extra mile and invest the additional cash and produce vanadium electrolyte as well as ferrovanadium to ensure a higher pricing for these premium products.

Using the company’s base case scenario, the after tax net present value discounted by 8% comes in at approximately US$2.9B (which represents an excess of 4 billion Canadian dollars) and even in a stress test scenario whereby commodity prices are reduced by 30% across the board, the NPV8% still comes in at almost C$1.5B while the internal rate of return almost reaches 25%.

The results of the PEA confirm District Metals should continue to aggressively advance the Viken uranium-vanadium-potash project, as the project could help to reduce the EU’s reliance on imported commodities.

Disclosure: The author has no position in District Metals. District Metals is a sponsor of the website. This post is for educational purposes only; be mindful investing in junior mining stocks is risky and you may lose your entire investment if things go wrong. Please read our full disclosure.

If I understand it well, the production scenario will be 10 miljoen TON per year. Which values it on $ 2.88 Billions. But, that is only 3% of the total amount. Is that correct??

Second question, why only 3%?? Hope to receive a clear answer. Thanking you in advance

You are correct in your interpretation. A mining/processing scenario of 10 million tonnes per year is envisaged.

Why only 3% of the resource? It doesn’t really matter if you outline a 100 year mine life, the impact on the NPV would be negligible. As explained in the report, even in Y14, the after-tax cash flow would be discounted by 70%. And by Y30, cash flow would be discounted by 92%, so for every $100M in after-tax cash flow, only $8M would be added to the NPV.

Hope this helps,