Kutcho Copper (KC.V) just announced an interest deferral agreement with Wheaton Precious Metals (you can re-read the update here). We sat down with Vince Sorace, Kutcho’s CEO to discuss the recent developments and the plans forward.

You recently announced an agreement with Wheaton Precious Metals (WPM, WPM.TO) which basically allows you to defer the next two interest payments until the end of 2021 while the credit facility provided by Wheaton will also be extended to December 2021. You must be happy to see Wheaton being flexible with the convertible debenture it owns?

Yes, we are very happy with this. Wheaton benefits from this project when it’s in production, and I believe they will continue to support us in a variety of ways, including technical support in order to achieve that goal.

Just to be clear, Wheaton PM currently has an option to establish a streaming deal on the Kutcho project and for now, Wheaton has only provided the US$7M for the feasibility study and the C$24M investment in equity (C$4M) and debt (C$20M through a convertible debenture), correct? May we assume Wheaton PM would like to remain in the pole position for the Kutcho precious metals streams and the current flexibility should predominantly be seen as Wheaton protecting their longer term streaming interests, as they will make quite a bit of money on the Au/Ag stream once you get through the feasibility study, permitting and construction phase?

This is correct. Wheaton has an option and will make a firm election to proceed with the streaming arrangement after the feasibility study is complete, at which point, they would contribute and additional USD $58 million to help build the project. This US$58M would qualify as an ‘equity’ investment and sharply reduces the financing needs for Kutcho for the equity component of any construction financing down the line.

Let’s talk about the feasibility study for a second. What’s the timeline on this?

We are quite confident we can complete the feasibility in about 6 months. We have done a lot of work in the background leading up to this over the past few years, which should help us move efficiently and cost effectively through the process now.

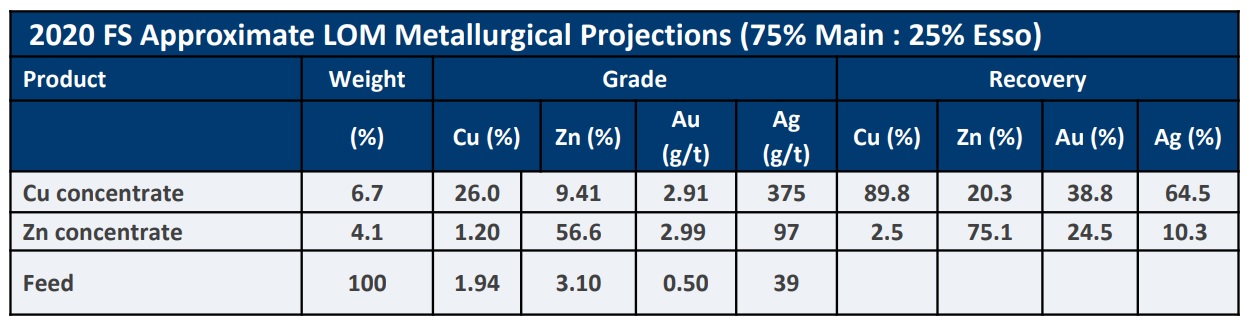

What changes are you eyeing to make in the feasibility study compared to the pre-feasibility study? Are you planning on reviewing things like throughput and cutoff grades for the mining reserve given the current strong copper (and PM prices)?

The significant changes we are looking at include mining methodologies, mine planning and throughput trade off studies, cutoff grades, processing will change now as determined by a successful metallurgical program over the past 18 months which varies from the PFS, and some other potential ideas to optimize the project we are excited to pursue.

Right before the summer, you reported strong metallurgical results as the copper, gold and silver recovery rates increased. This should have a positive impact on the feasibility study as well.

Anytime you can get more metal out of the ground and/or recovered through processing (economically), one could expect better economic results from the project. It is definitely our goal to optimize all of our findings and results through the revised metallurgical program and translate that into value. But of course, it’s not up to us to speculate about NPV and IRR boosts at this point, so we will have to wait for the feasibility study to see the final impact of these important improvements.

Right now, you’ve got everything going for you. Your project is an underground project in a Tier-1 mining jurisdiction, the copper price is exceeding $3/pound, despite the streaming agreement with Wheaton you’ll retain some of the upside potential from the precious metals contribution while a zinc price of $1.10 will also be a welcome sight. What’s holding Kutcho back, in your opinion? Is it the convertible debenture? Is it the wait for the feasibility study? Is this one of those Catch-22 situations where the debt is a prohibiting factor to raise the money for the feasibility study which in turn doesn’t allow you to raise money with a positive FS to repay the debt?

I do believe we have had two hurdles in front of us. The first was the ability to raise capital to complete the feasibility study, which we now have. The feasibility study will be an extremely important milestone towards de-risking and the viability of the project.

As mentioned earlier, there will be some significant changes from the Pre-Feasibility Study (done in 2011), and once we have proven those changes to be opportunistic and adding value to the project, it will add a lot of confidence to investors. From there, I believe we will attract a significant audience of potential financiers/strategic investors, at which point we can address our second biggest hurdle, the outstanding convertible debenture (which I believe we can deal with in a positive way once we have a path to production).

What’s your outlook on the copper market?

In my opinion, the copper market is poised for significant growth. We were already on a path (before COVID) where demand from EVs, renewables and other green/technologies was helping demand outpace supply. Now, with supply side disruptions prevalent because of COVID, yet demand side increasing out of China due to infrastructure/stimulus spending (and more infrastructure spending to come from countries around the world to replace permanent job losses due to COVID), copper is poised for some significant price increases in the year(s) to come.

Disclosure: The author has a long position in Kutcho Copper. Kutcho is a sponsor of the website. The author has no position in Wheaton Precious Metals.