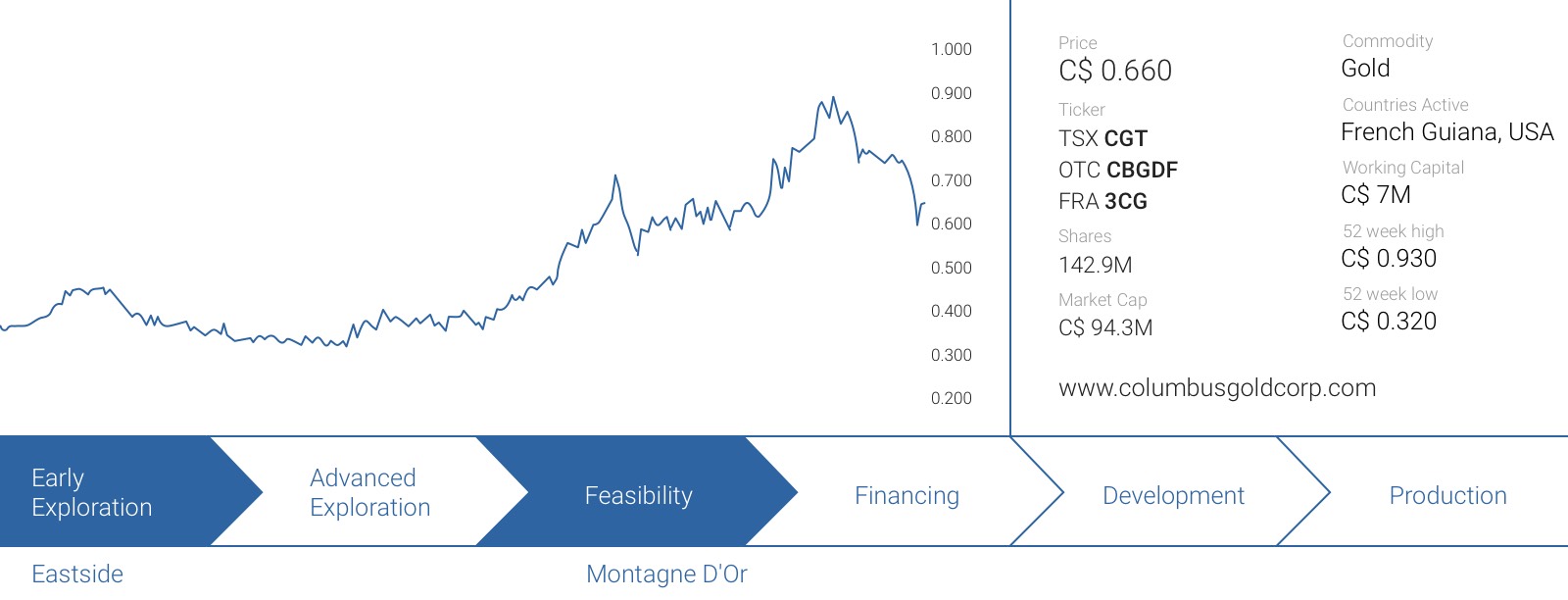

We have been very positive about Columbus Gold (CGT.TO) ever since the company acquired the Montagne D’Or gold project in French Guiana. Whereas most investors were quite unfamiliar with the country, French Guiana wasn’t uncharted territory for us, as it’s an integral part of France. France indeed doesn’t really have a mining history, but the local and national governments seem to be eager to get the project up and running to fight the 21.9% unemployment rate in the overseas department.

As always, all assumptions and calculations in this report are our own back of the envelope calculations and do not represent the official position of Columbus Gold.

A brief recap of Montagne D’Or and the earn-in agreement with Nordgold

The project is located in the northwestern part of French Guiana, approximately 130 kilometers from the Atlantic Ocean, and not too far away from the border with Suriname where several large gold deposits have been discovered, and where IAMgold (IMG.TO, IAG) is mining the Rosebel gold mine and Newmont Mining (NEM, NEM.TO) is about to open its Merian mine. Newmont spent approximately $1B on Merian, which will produce 400,000-500,000 ounces of gold in the first five years of its mine life.

When Columbus acquired the project, Montagne D’Or contained almost 2 million ounces of gold, but there clearly was a lot of potential to increase this resource and a few years ago we already made the bold statement the Montagne D’Or land package very likely contains 8-10 million ounces of gold. After an extensive drill program (partly funded by Nordgold), the resource estimate at Montagne D’Or contained approximately 5 million ounces of gold and as plenty of strike length remains unexplored and as several other ‘hot spots’ remained untested (or where insufficient data was collected to include these zones in a resource estimate), we remain confident in our exploration target and remain convinced Montagne D’Or will ultimately contain 8-10 million ounces of gold.

Columbus Gold wasn’t the only company that saw the value in this property, and Columbus was able to attract London-listed Nordgold (NORD.L) as its joint venture partner on Montagne D’Or. The joint venture agreement was advantageous for Columbus Gold and it’s obvious the company negotiated the agreement from a point of strength. Not only is the JV deal an ‘all or nothing’ agreement whereby Nordgold will only earn its 50.01% (+5%) interest after completing $30M in exploration expenditures (completed) and publishing a bankable feasibility study before March 2017. This means the total financial commitment from Nordgold will very likely be somewhere in the neighborhood of $40-45M, and it’s needless to say this was quite a good deal as Columbus’ share structure would have exploded if the company would have had to raise this cash on its own.

Nordgold is now completing the final part of its earn-in commitment. The required amount of exploration expenditures has now been met, and the company now only has to release a feasibility study to earn a 50.01% stake in the property, where after the acquisition of an additional 5% will be confirmed as well. Technically, Nordgold has until March of next year to complete the feasibility study, but it does look like we could see the results as early as January. Long story short, there’s zero doubt Nordgold will earn a 55.01% stake in Montagne D’Or.

The PEA was very positive, but there still was ample room to improve the economics

The next question is whether or not the project is good enough to entice Nordgold to move to a 100% ownership. Keep in mind Nordgold has always bought the stakes of its minority partners in its previous ventures. It was able to gain full control of High River Gold after a long fight, and earlier this year Nordgold made a move to acquire all remaining shares of Northquest it didn’t own yet. This also confirmed one of the first remarks we made when the joint venture with Nordgold was announced; this major gold producer isn’t interested in dealing with a minority partner, and once it will have earned its 55.01% in the project, we think the company will make a move to acquire the remainder from Columbus Gold.

But of course, acquiring the remaining 44.99% won’t be cheap, and consolidating its ownership in the project must also make sense for Nordgold. So let’s take a step back and figure out what the ‘true’ value of the Montagne D’Or project is, based on the Preliminary Economic Assessment, which was completed and filed in the summer of last year.

As the gold price was trading much lower when the PEA was published, Columbus Gold used a gold price of $1200/oz as its base case scenario. However, as gold now seems to be holding its ground above $1300/oz, we think it makes more sense to use that gold price to figure out what the project would be worth today.

If we then pull up the sensitivity analysis from the Preliminary Economic Assessment, it’s obvious the used discount rate and gold price play an important role in the Net Present Value of the project. Using a gold price of $1200/oz, the after-tax NPV8% is $324M which is okay but not shocking. However, if you’d reduce the discount rate to 5% (which would be acceptable in the current low-yield investment climate, as a discount rate should be seen as a mark-up to the risk free interest rate to include a certain risk-adjusted variation in the NPV calculations), the after-tax NPV increases to $451M.

Using a gold price of $1300/oz (but still using a discount rate of 8%), the after-tax NPV increases to $452M and if we would use a discount rate of 6%, we would end up with an after-tax of in excess of $475M, and this also is the base case valuation we would use in our scenarios.

That’s obviously pretty nice and we think the final feasibility study won’t be very different from the PEA although you should obviously take some inflation into account. On top of that, we have the impression equipment prices have picked up again now the worst seems to be behind us and the mining sector is gaining momentum again.

We are also looking forward to see if the cost of power could be reduced. The PEA estimated the cost of power to be $6 per processed tonne of rock, which basically meant that in excess of 40% of the total production cost was related to power expenses. This was mainly due to the fact the power was expected to be generated by the company’s own generators at a cost of approximately 21-22 cent per KWh. However, Columbus Gold and Nordgold have engaged Tractebel to study the possibility to extend the power grid from Saint Laurent to the project, which could reduce the power cost to 12 cents per KWh.

We don’t have any details about the potential cost of the grid extension, but a short note in the company’s technical report indicated linking up the project with the power grid would cost approximately $70M. That’s indeed quite a bit of cash, but considering the generator-based scenario would cost the company $27M per year in power-related expenses, slashing these operating expenses by 50% would save Columbus and Nordgold $13M per year, so the payback period of the power grid extension would be 5-6 years. So, the longer the mine life in the feasibility study, the more sense it makes to investigate this scenario as it could reduce the production cost per ounce by in excess of $50/oz over the entire mine life. According to our own back of the envelope calculations, this could add $30-50M to the after-tax NPV8% of the mine, using a gold price of $1300/oz.

Nordgold’s balance sheet could definitely handle the acquisition of the remaining 44.99%

At a gold price of $1300/oz, we expect the after-tax NPV6% to be approximately US$475M, which means Columbus Gold’s stake should be valued at US$214M. Thanks to the cheap Canadian Dollar, this is approximately C$283M (using an USD/CAD exchange rate of 1.32). That’s indeed substantially higher than Columbus’ market capitalization, and in the next table we provide you with a simplified sensitivity analysis based on a P/NPV ratio Nordgold would be willing to pay, and what the value per share of Columbus Gold would be (using 145M outstanding shares rather than the 141.5M shares right now).

[table caption=”” colalign=”left|left|left”]

P/NPV Ratio;Value (in C$M);Value per share of Columbus Gold (in C$)

0.25;71M;0.49

0.4;113M;0.78

0.5;142M;1.98

0.6;170M;1.17

0.75;212M;1.46

1;283M;1.95

[/table]

Of course, the total amount of gold in the proven and probable reserve categories will probably be a bit lower than the 3M ounces we are taking into consideration, but this could be mitigated by Columbus Gold demanding a higher P/NPV ratio, to take future additional ounces into account as we have no doubt the total mine life at Montagne D’Or will be much longer than the mine life to be used in the feasibility study. Not all of the 5 million ounces will be converted into reserves in the first mine plan, but we have very little doubt the Montagne D’Or mine will produce more gold than what will be anticipated in the feasibility study.

Are we 100% certain Nordgold will make a move to acquire 100% of Montagne D’Or? No, but we are very confident the company will make a move, as its development pipeline is almost ready now the Bouly gold mine in Africa is currently being commissioned. There aren’t a lot of feasibility-stage projects out there that would meet Nordgold’s requirements, and the simple fact it will own 55.01% of Montagne D’Or will put the company in the pole position.

We don’t expect Nordgold to make a move the day after publishing the feasibility study, as the Russian company is quite smart and wants to de-risk a project as much as possible before ‘betting big’ on it. We would expect the Environmental and Social Impact Assessment (‘ESIA’) to be crucial in Nordgold’s decision-making process.

And Nordgold has plenty of cash available, as its adjusted free cash flow in the first half of the year (defined as operating cash flow excluding changes in its working capital position minus the sustaining capital expenditures) was $190M. Not only would this allow the company to fork over cash to acquire the remaining 44.99% of Montagne D’Or, it would also put Nordgold in a position to fund the construction of the mine without any external financing.

Conclusion

With the gold price trading firmly above $1300/oz, the economics of Montagne D’Or will improve and we are now expecting an after-tax NPV6% of US$475M in the upcoming feasibility study, based on 3M ounces of payable gold, and approximately $370M based on 2.5 million ounces (the reserve estimate will be released with the definitive feasibility study)s. Of course, should the reserve statement contain less than three million ounces, the NPV will be lower, but if we keep an eye on the greater scheme of things, we dare to go on record and say Montagne D’Or will be one of South America’s next multi-million ounce gold mines.

If history repeats itself, Nordgold will try to acquire 100% of Montagne D’Or, and after checking up on the company’s financial health, we have no doubt the Russian company will be able to fund an acquisition of the remaining interest as the total price tag for the 44.99% stake will very likely be lower than the free cash flow Nord Gold generates in a semester.

And even if Nordgold doesn’t make a move, we would expect Columbus Gold to be able to contribute its fair share of the development expenses to maintain its 44.99% stake in Montagne D’Or. Whether or not Nordgold will acquire 100% of Montagne D’Or, the fair value of Columbus’ stake is substantially higher than the current market capitalization of C$94M.

The author holds a long position in Columbus Gold. They are a sponsor of this website. Please read the disclaimer

Interesting analysis. Do you think that Iamgolds approx 14% holding in CBGDF suggests they would have an interest in buying CBGDF’s gold portion and sharing in the Nordgold mine development? Plus how might CBGDF Nevada project (first estimate Nov 2016?) impact the Nordgold decision. If Frank Giusta is a major shareholder of CBGDF (??) he has shown no concern with having Russian involvement in American based minerals.

Hi Asrm,

Considering Nordgold already has the option to acquire 55.01% and seems to be pretty straightforward and aggressive advancing the project, IAMgold would only be able to maintain a 44.99% stake if it would buy Columbus Gold. That’s definitely possible, but Nord Gold seems to be ‘allergic’ to having minority partners on a project level, so in case IAMgold would step up the plate, it’s not unlikely to see a bidding war.

However, and this brings us to your second question, it would be easier for Nord to just acquire the 44.99% stake from Columbus (and then you have to trust the negotiation skills of the CGT management to get the highest price possible), where after Columbus will retain the Nevada assets. Nord Gold isn’t opposed to owning US assets, but we’re not quite sure Eastside meets Nord’s requirements yet, so we would expect Nord to retain an equity stake in the vehicle which owns Eastside, and once the project is more advanced, they will be in the pole position to negotiate a strategic deal.

We hope this answers your questions?

Hi Asrm,

Considering Nordgold already has the option to acquire 55.01% and seems to be pretty straightforward and aggressive advancing the project, IAMgold would only be able to maintain a 44.99% stake if it would buy Columbus Gold. That’s definitely possible, but Nord Gold seems to be ‘allergic’ to having minority partners on a project level, so in case IAMgold would step up the plate, it’s not unlikely to see a bidding war.

However, and this brings us to your second question, it would be easier for Nord to just acquire the 44.99% stake from Columbus (and then you have to trust the negotiation skills of the CGT management to get the highest price possible), where after Columbus will retain the Nevada assets. Nord Gold isn’t opposed to owning US assets, but we’re not quite sure Eastside meets Nord’s requirements yet, so we would expect Nord to retain an equity stake in the vehicle which owns Eastside, and once the project is more advanced, they will be in the pole position to negotiate a strategic deal.

We hope this answers your questions?

Pingback: ALEXEI MORDASHOV PREPARES $400 MILLION DOLLAR TAKEOVER OF CANADIAN GOLDMINER – HIT AND RUN FOR KREMLIN FOREIGN INVESTMENT BAN | Dances With Bears