Cypress Development (CYP.V) is currently working on its last metallurgical test work which will set the tone for what we can expect in the feasibility study. The key element to move this project forward seems to be the use of chloride-based leaching to recover the lithium from the claystone. This will have positive environmental and economic benefits compared to sulfide-based leaching and the pilot plant which is currently geared towards proving up this theory is in full swing with results expected in Q1 2022.

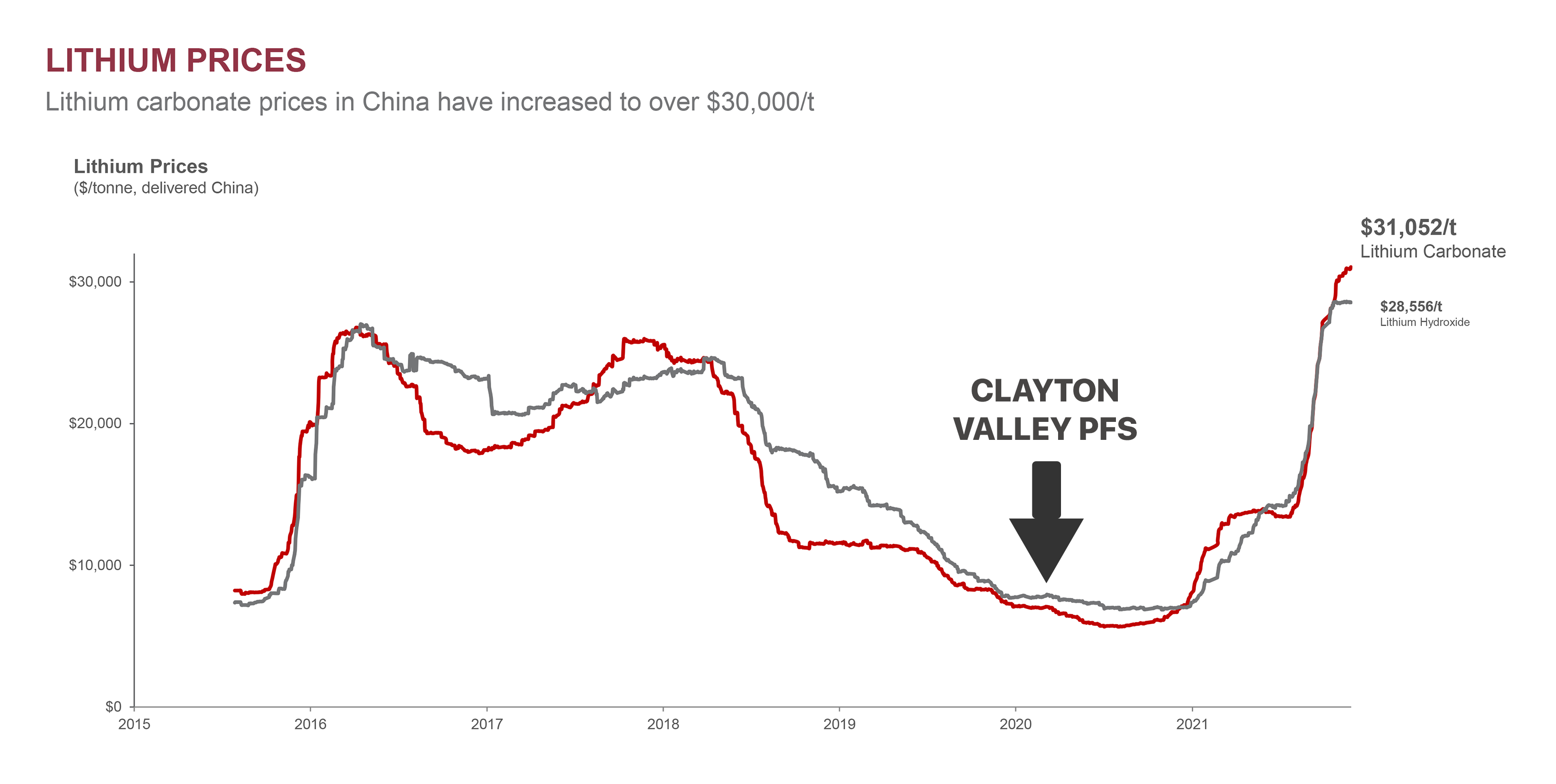

As the pre-feasibility study is now already almost 1.5 years old again and used a much lower lithium price, we wanted to spend some time to look at the potential impact of using a higher lithium price on the economics. And despite the fears of capex and opex increases due to an inflationary environment, the higher lithium price seems to be more than making up for it.

A brief recap of the Clayton Valley Lithium project

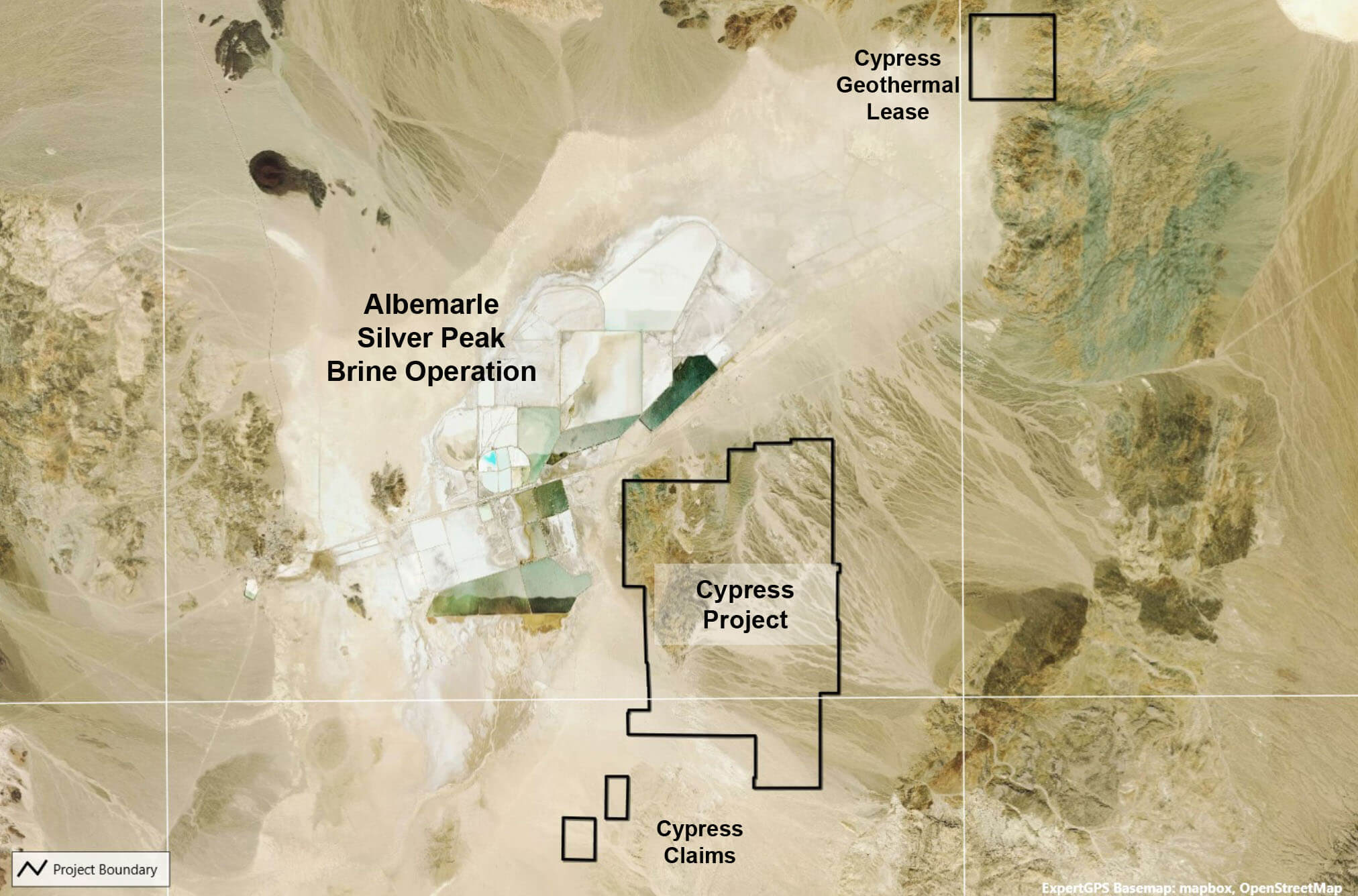

Clayton Valley is located almost just 60 kilometers southwest of Tonopah, which acts as a regional center for the mining industry in Nevada. The project is also immediately adjacent to the Silver Peak lithium mine, currently operated by Albemarle (ALB) after its acquisition of Rockwood Holdings a few years ago.

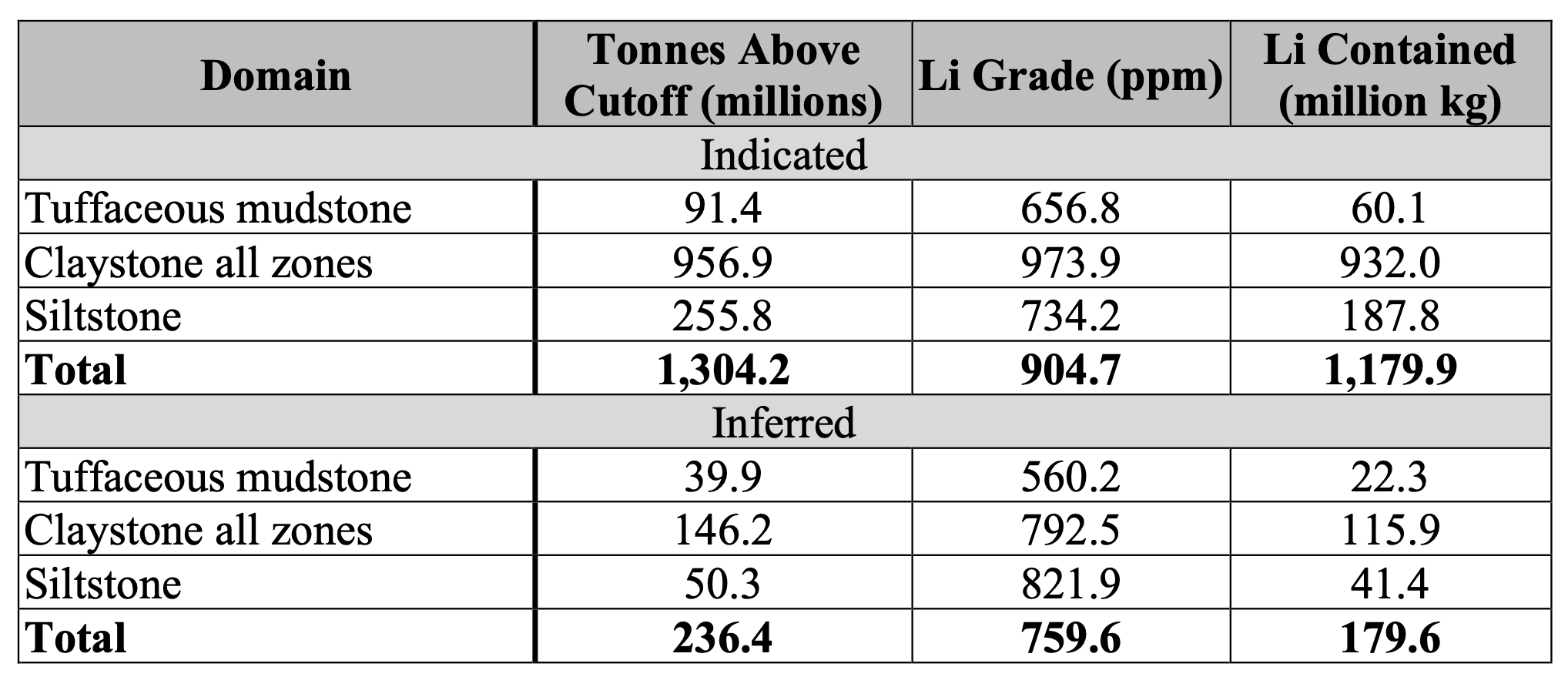

Subsequent to the release of the pre-feasibility study last year, Cypress Development announced a massive resource increase. Whereas the original resource (completed in May 2020, and used for the pre-feasibility study) contained just under 600 million tonnes in the measured and indicated resource categories at an average grade of 1,073 ppm lithium, the subsequent resource update increased this to a total of just under 930 million tonnes in the measured and indicated resource at a just slightly lower average grade of 1,062 ppm lithium. In the most recently filed technical report on the project, this was further updated to 1.3 billion tonnes in the indicated resource category and about 236 million tonnes in the inferred category.

It is important to secure all relevant inputs for the production process well ahead of time. One of the potential issues a lot of Nevada-based projects are facing is securing enough water as it often means companies need to get permits to pump up water from known aquifers. And understandably, there is more involved than just getting a request rubber-stamped. This is especially true in the Clayton Valley as the Nevada Division of Water Resources has previously stated no new water permits would be issued.

Cypress Development has been very proactive and announced in May this year it had signed a Letter of Intent with a subsidiary of Nevada Sunrise Gold (NEV.V) which owns a permit allowing it to draw down on 1,770 acre-feet of water for mining activities. According to Cypress, this water pumping permit has the largest volume allowance of all available existing permits in Clayton Valley and will take care of a large percentage of the water needs as calculated in the pre-feasibility study.

While the currently permitted pumping rate is potentially not sufficient to cover all the water needs for the mine as per the pre-feasibility study, keep in mind Cypress Development is working on the chloride leaching option to process the Clayton Valley rock. This would reduce the water consumption levels and this could make the existing water permit sufficient after all, but we will have to wait for the feasibility study before we know for sure.

Water clearly is a critical element for the Clayton Valley operations, and the proactive approach of Cypress Development is commendable. The water rights will be secured at an advantageous price as well: Cypress was required to make US$150,000 in non-refundable deposits and upon closing the company was required to make a US$2M cash payment and issue US$0.85M in new shares. A very reasonable price for a key element in the production process. The purchase of the water rights was completed earlier this month and this allowed Cypress to tick an additional box in the de-risking process of the Clayton Valley project.

The pre-feasibility study was completed at much lower LCE prices – and the situation has now changed dramatically

Cypress Development has always done a good job in delivering its milestones on time. In just a few years, the company moved from pure exploration to the PEA stage and subsequently delivered a complete pre-feasibility study in May 2020. That study is now obviously already outdated as the lithium price is now more than twice as high and the company is working on a new process to recover the lithium from the clay.

That being said, it does make sense to have another look at the pre-feasibility study, if only to paint some sort of worst case or base case scenario. Because even in that scenario, using a lithium price that’s about 60-70% lower than the current spot price, the project appears to be very viable and could be a viable source of supply for the domestic lithium needs.

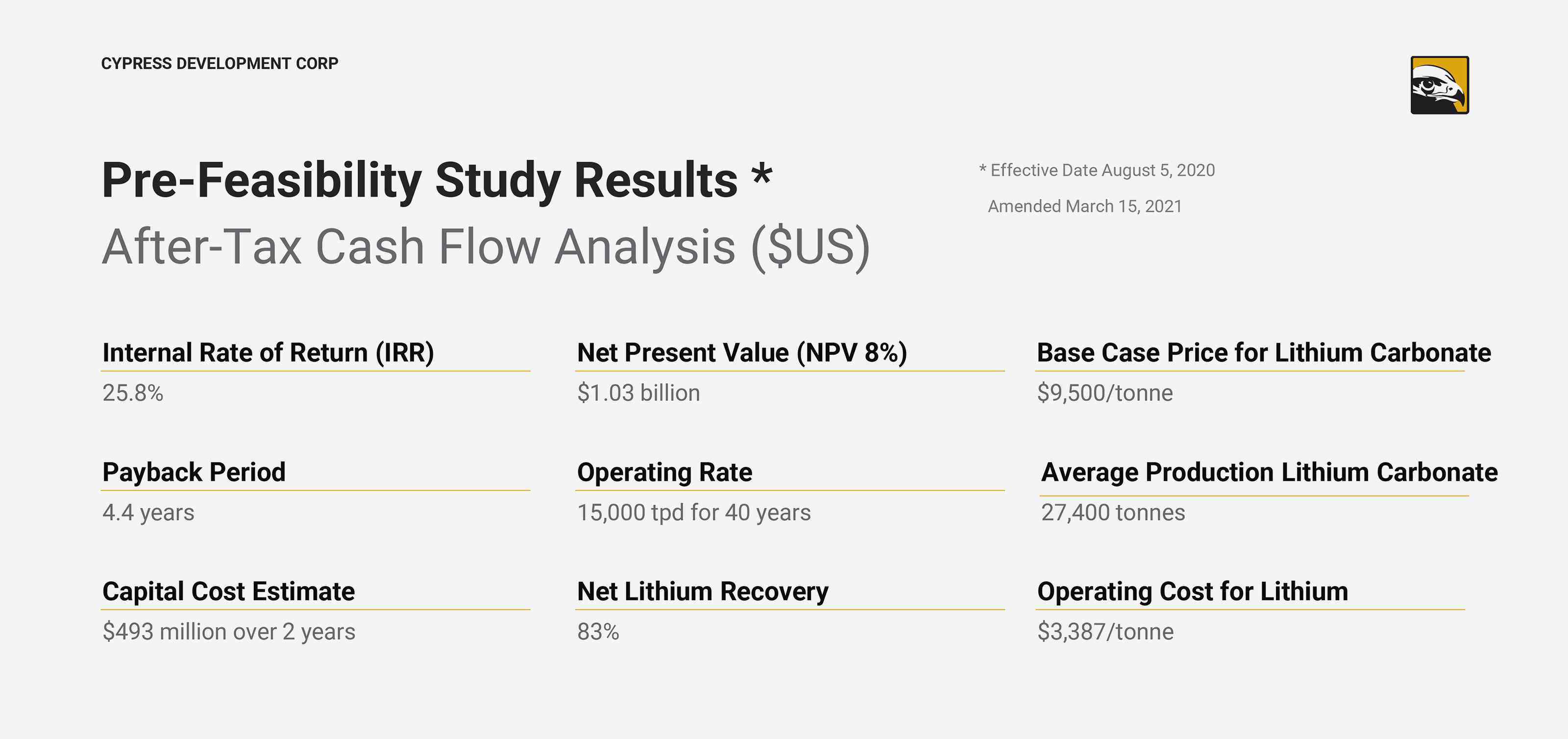

The pre-feasibility study was based on a production rate of 15,000 tonnes per day which was anticipated to produce approximately 27,400 tonnes of LCE (‘Lithium Carbonate Equivalent’) over a 40-year mine life. That production scenario was based on the probable reserves of just 222 million tonnes (at an average grade of 1,141 ppm lithium), but investors should be aware the current indicated resource contains 1.3 billion tonnes. And of course, the current lithium price may likely add quite a few tonnes to the mine plan (in the long run) because even if (slightly) lower grade zones would be mined, the increased operating cost would not be a deterrent given the strong lithium market.

The total resources on the project are currently 1.3 billion tonnes at 905 ppm in the indicated resource category and an additional 236 million tonnes at 760 ppm. At the current lithium price, we would expect mining 900 ppm material would still be very profitable and a large chunk could eventually end up in the open pit. But of course, that’s just our interpretation and not the company’s official guidance.

Just to explain how important the large resource is: even if Cypress Development would boost its throughput to 25,000 tonnes per day (+67%), mining 400 million tonnes of the total 1.3 billion tonnes in the indicated resource would still take 44 years. This emphasizes the importance of a large resource that could help the domestic lithium supply in the USA for decades to come.

Another important factor in the economics is the low stripping ratio. As per the pre-feasibility study, the strip ratio was just around 0.29 and that clearly helped to keep the operating costs low.

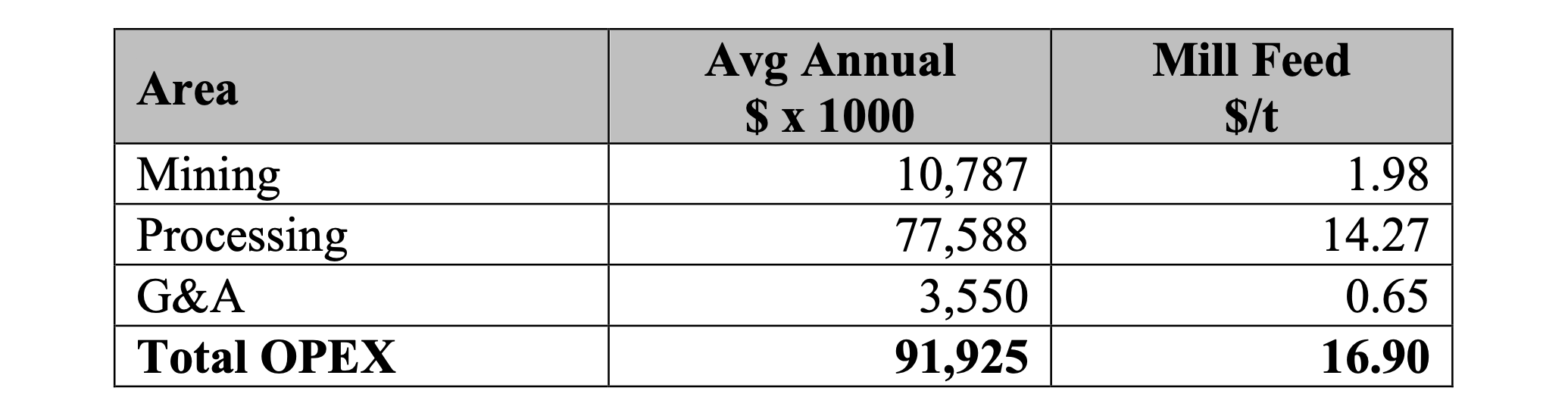

In the pre-feasibility study, the anticipated production cost was approximately $3,400 per tonne of LCE but due to some cost inflation, we expect this number to increase. That’s not an issue as the lithium price is currently more than twice as high so the margins will be very robust in any case.

Looking at the breakdown of the operating costs; the mining costs represent less than 15% of the total opex. The main element of the total operating cost is the processing cost and that’s exactly why the current metallurgical test program is so important.

Earlier test work in 2021 used samples of claystone that were treated with sodium chloride and hydrochloric acid to determine the optimal leaching temperature and the required strength of the acidic elements. Importantly, the initial results indicated the recovery rate exceeded the 81% recovery rate used in the pre-feasibility study.

The higher recovery rate could be a major boost for the project economics. An increase from 83% to 85% would add in excess of 500 tonnes of LCE per year representing an additional $14M in revenue on an annual basis using the current spot price, and about $6M using $12,500 lithium. That’s based on the anticipated production rate of 15,000 tonnes per year in the pre-feasibility study. Using an anticipated higher throughput of 25,000 tonnes per day would result in a production increase towards 40,000 tonnes of LCE per year. And although we are using LCE for now, keep in mind Cypress is obviously aiming to produce lithium hydroxide on-site.

As there would hardly be any increase in opex (in fact, using chloride leaching could result in an overall decrease in the operating expenditures), that would be a pure net gain that would help both the IRR and the NPV. And that recovery increase is likely. In fact, the pre-PFS met work indicated recovery rates of 85-87% could be achieved, but the company chose to use a more conservative approach and used an 83% recovery rate. While there’s no certainty a higher recovery rate could be achieved, we do like the odds.

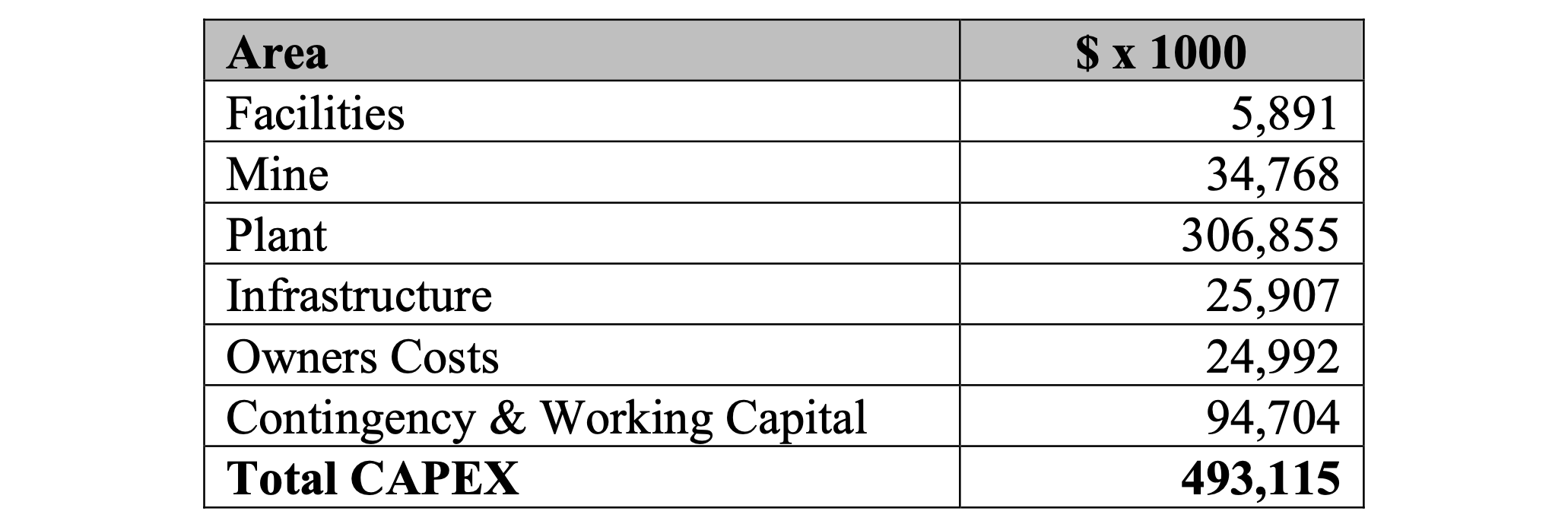

The initial capex was estimated at $493M, but looking at the breakdown of the capex elements, you’ll notice there’s an allocation of almost $95M for contingency and working capital elements. That’s approximately 24% of the pre-contingency and pre-WC capex and that’s much higher than what we usually see: most economic studies only take a 15% contingency into consideration but are ‘forgetting’ about the working capital required between the end of the construction activities and the start of the positive free cash flow.

So while investors should realistically expect a higher opex and capex mainly because of cost inflation, there is a chance Cypress could surprise positively given all the improvement and optimization projects it’s working on. Even though inflation is a real issue these days, the comfortable contingency cushion in the pre-feasibility study could absorb some of that inflation.

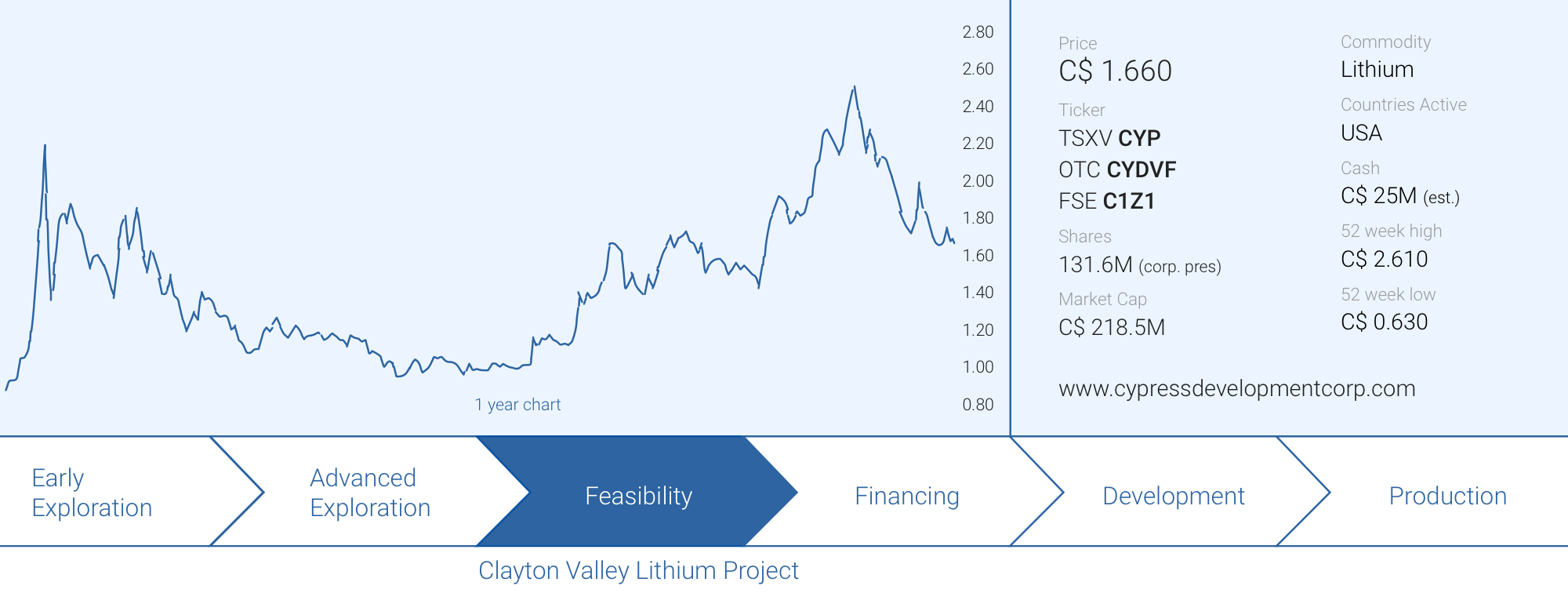

CYP’s balance sheet is very healthy

Cypress Development filled its treasury when cash was easily available.

As of the end of September, Cypress had a working capital position of approximately C$19.6M. Not only is this exceptionally strong for a company in the final phase of its economic studies, the ‘subsequent events’ section of the financial statements mentions about 4.74 million warrants have been exercised since October 1st, for a total additional cash injection of just under C$7M. Most of those warrants were part of the block of 15.64 million warrants outstanding with an exercise price of C$1.75 while we would assume all of the almost 937,000 warrants with an exercise price of C$0.33 that had an expiry date of October 26th were exercised as well, as they were deeply in the money.

This means that as of the publication date of the quarterly report, there were still about 12 million warrants with an exercise price of C$1.75 outstanding and as the Cypress share price has been quite strong in the past few weeks, we expect these warrants to be gradually exercised over the course of the next 27 months (they are expiring in March 2024).

The current healthy cash balance and the status of the warrants means Cypress won’t have to get back to the market anytime soon and that puts the company in a luxury position. And the market knows that if anyone wants to acquire a position, open market purchases are the only option as Cypress can negotiate future financings from a strong position as it is for sure not with its back against the wall.

Thanks to the low-cost nature of the pilot plant (kudos to Bill Willoughby and his team for that), we expect Cypress to have a net working capital position of around C$25M. That indeed is a very comfortable position to be in as Cypress continues to work on de-risking the project.

Pilot Plant – Extraction Testing of Lithium-Bearing Claystone

Conclusion

Five years ago, no one cared about clay assets. ‘Too difficult’, ‘why would anyone want clay-hosted assets when there are plenty of ‘normal’ lithium assets’ were the main arguments. But the situation has now changed as in the past few years it has become clear the lithium supply just cannot keep up with the increased lithium demand. Projects are taking longer to reach full production or are facing permitting issues. This, in combination with an anticipated additional demand increase, has pushed the lithium price higher and although Cypress will for sure not use a $25,000/t base case scenario, we think the base case scenario of $9,500/t in the pre-feasibility study may be too conservative.’

When we look at the ‘optimistic’ scenario in the pre-feasibility study, the lithium price of $14,250/t would likely be a more realistic scenario. This means that although we would expect both the capex and opex to increase compared to the pre-feasibility study (mainly due to cost inflation), the NPV and IRR should remain very healthy thanks to the strong lithium price which will be very forgiving.

While there still is a negative perception surrounding clay-hosted deposits, Cypress Development will likely benefit from the second mover advantage as Lithium Americas (LAC, LAC.TO) will advance its Thacker Pass clay-hosted lithium project and this will likely pave the way for other clay-hosted deposits, of which Cypress Development’s Clayton Valley is the most advanced.

We are looking forward to seeing the results of the pilot plant as that will determine the main parameters of the upcoming feasibility study. But at $20,000/t lithium or even $15,000/t, there’s no doubt the feasibility study will show Clayton Valley to be a very profitable project with a margin of at least $10,000/t in the $15,000/t pricing scenario. And with a multi-decade mine life, it may be only a matter of time before larger players could notice the potential importance of Clayton Valley in the domestic lithium supply chain.

Disclosure: Cypress Development is a sponsor of this website. The author has a long position in Cypress Development. Please read the disclaimer.