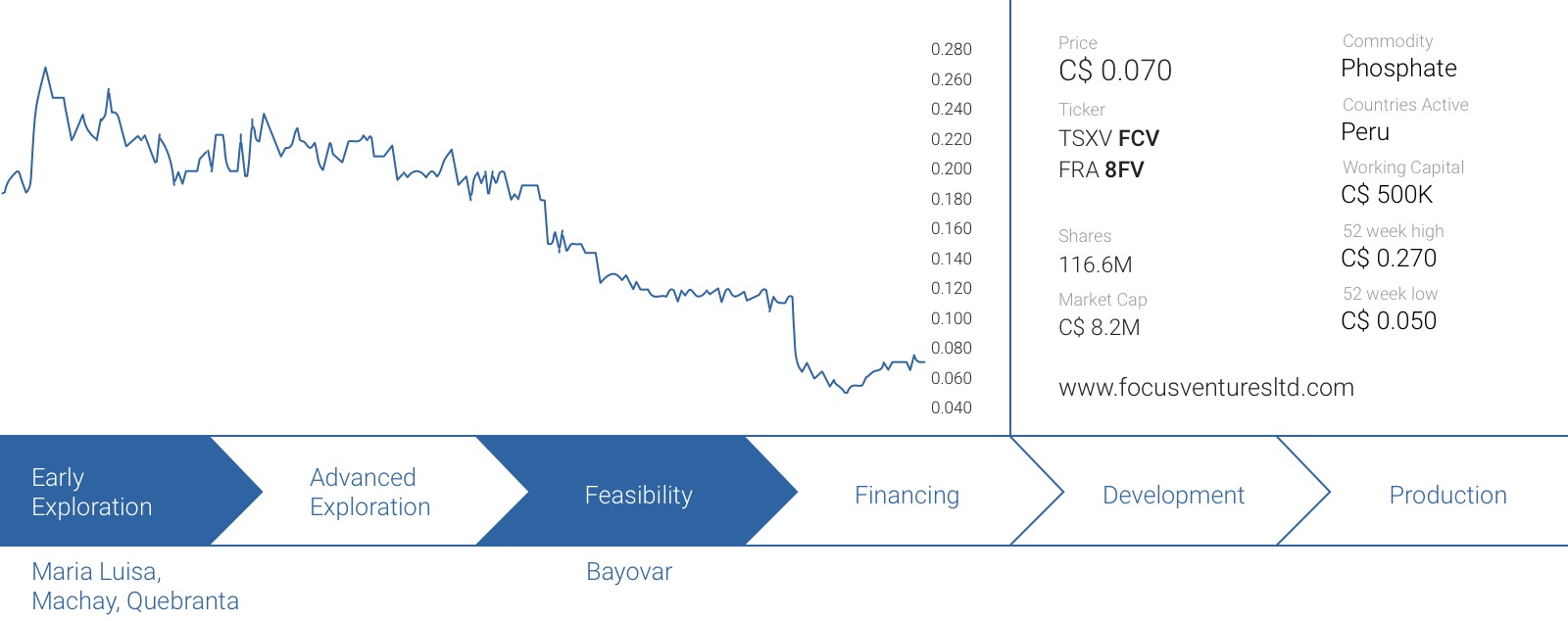

Focus Ventures (FCV.V) released a pre-feasibility study on the Bayovar 12 project in the first few days of January. This study had to be completed by the end of the previous year to avoid a $500,000 penalty payment to the vendors, so the PFS was rushed leaving the consultants insufficient time to carry out optimization studies. Certain market participants expected better numbers, and started to sell the shares knocking down the share price that briefly touched the 5-cent level.

However, we remain confident that we’ll see much improved numbers, as the management team seems to be quite optimistic that it will be able to improve the economics of the project. In this report we will briefly discuss the potential improvements at the project which will explain why we expect the feasibility study to be more appealing than the pre-feasibility study.

There’s plenty of potential to improve the economics at Bayovar 12

Even though the pre-feasibility study wasn’t that bad, the market was upset after seeing the internal rate of return coming in lower than anticipated. Despite this, the after-tax NPV was still pretty solid (at almost C$350M after-tax on a 100% basis), confirming that Bayovar remains a very robust project and probably one of the most exciting phosphate projects in the world. The main reason for the sell-off was because this first pass at the project economics didn’t live up to the market expectations and a Mea Culpa from Caesars Report is warranted as well; we also underestimated the initial capital expenditures based on what we had been told by the company’s management early on in the pre-feasibility work. The higher capex resulted in a lower than expected IRR, causing the market to overreact when the PFS was released.

But what happened has happened, and the company’s focus (pun intended) should now be aimed solely at improving the economics at Bayovar 12 in the feasibility study. We’ve spoken to management and they’ve outlined several areas of the study which would benefit from optimising so we expect the definitive feasibility study to present a much stronger project assuming they are successful. It’s also our understanding that some of the factors such as tailings facility redesign for example would be done as part of the main feasibility study. There are a lot of “moving parts” and looking at them all will take time, and can realistically only be done as part of a FS which would also bring in a new mine model.

Some improvements would require very little additional investment but could have a huge impact on the final economics of the project. For example, making a trade-off analysis to determine the best output rate would really make a lot of sense. In the original pre-feasibility study, the Bayovar mine plan was designed around an initial throughput of 300,000 tonnes per year, increasing to 1 million tonnes per year in the fourth year of the mine life. Whilst this is a good move to reduce the up-front capital expenditures it’s probably not the most efficient solution in terms of maximizing your NPV and boosting the internal rate of return.

Indeed, a higher initial throughput should improve the Bayovar 12 economics and – according to our research based on a 1M tpa plant – the initial capex for the plant wouldn’t be very different from the currently quoted $127M because building a 1M tonne plant is cheaper than building two half-million tonne per year production lines. That being said, starting with a 1 million tonne per year operation will increase the need for additional trucks and excavators, whilst the pre-stripping expenses will also increase.

We do think upsizing the output rate to 1 million tonnes per year would actually be a value-enhancing move as

- the payback period will be shorter,

- the IRR will be higher and

- the NPV would be higher as well thanks to the higher cash flows in the first few years of the mine life.

Focus is facing a balance exercise to ensure the capital ratio will be improved (capex/tonne) whilst also maximizing the NPV and payback periods and that’s always a tough call to make. But whatever Focus’ management decides to do, we are extremely confident the IRR will be in excess of 20%, and aiming for an after-tax IRR of 25% is quite realistic.

The technical report confirms our assumption this was a conservative report. Some important highlights

Focus Ventures filed the technical report on the Bayovar 12 pre-feasibility study last week, and we were obviously very eager to see some more details.

1. Pricing

The pre-feasibility study used an average price of $145/t for the 24% P2O5 product and $185/t for the 28% product, and as expected, the PFS has now provided more details on this price setting. We received some questions from readers who thought Focus’ study was using very optimistic phosphate prices. However, as Bayovar 12 will produce DAPR (Direct Applicable Phosphate Rock), the received price per tonne will contain a large premium compared to the price of phosrock which is currently trading at just $120/t, and we’d like to clarify how the expected prices were determined.

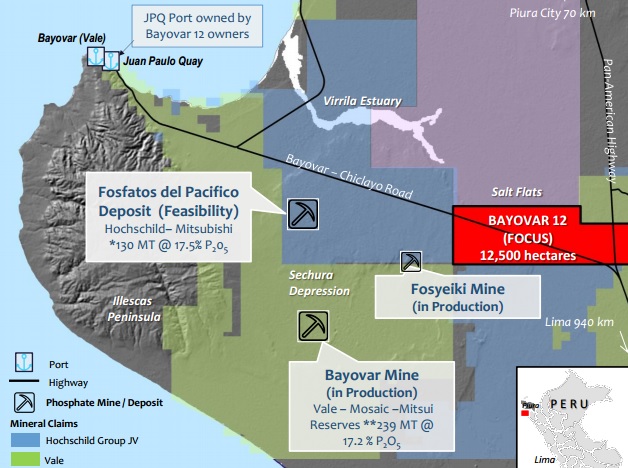

Apparently, Focus’ neighbor, the Fosyeiki mine, is selling its 22-24% product at a price range of $163-195/tonne (on an FOB basis) and even up to $220/t when the product gets shipped to Bolivia and Ecuador. Those are the wholesale prices of a small operation but according to the technical report, the retail price for Direct Application Phosphate Rock (DAPR) in Peru is approximately $320/t so the assumed price of $145/t in the pre-feasibility study seems to be very realistic.

There’s less information available on the pricing of the 28% product but Focus Ventures plans to put the product in the market as a potential competitor of Super Single Phosphate which sells at approximately $250/t. The company’s consultants have applied a 25% discount to the price of the SSP to derive the received price for the 28% product. However, we feel this is a very conservative approach. According to our research, the 28% Sechura rock actually works better than the SSP that’s currently being used. We think the 25% discount to the SSP price will only have to be implemented in the first few years of the mine life as some sort of ‘acquaintance discount’ until the end-users can really see the difference between using the 28% DAPR product and the Super Single Phosphate and we expect the discount to either disappear or to be reduced, further increasing the margins.

Based on the additional background information, we don’t think the used prices for the phosphate are unrealistic at all. This is important as the received price will have a huge impact on the after-tax NPV 7.5% of the property. A 10% change in the received price has an impact of US$100M on the NPV. Additionally, it could make sense to explore the options for a homogenous product containing 28% P2O5 (instead of producing a 24% and 28% in a 50/50 ratio) as this would expand the average operating margin by $20M per year (due to an increase in the average sales price from $165/t to $185/t).

To be honest, if there’s a sufficient demand for the 28% product, we don’t understand why Focus Ventures would even consider producing a 24% product as well, as the operating margin of the 28% product is approximately 57% (!) higher ($110/t vs $70/t).

2. Expanding the plant will be cheaper than expected

We were looking forward to see some more details about the marginal cost to start the second production line. The initial capex of $127M is based on an initial circuit capable of producing 500,000 tonnes of phosphate per year, but the PFS is taking an expansion to 1M tonnes per year into consideration by adding a second production line in the third year of the mine life.

We are positively surprised to learn the additional capex to build this second production line is expected to be just $32.2M (which includes a $5M contingency) as some major expenses (the seawater pipeline and the construction of a new power line) will be a sunk cost. That’s pretty cheap and it allows the company to think about adding a second production line once the operation is up and running at 1 million tonnes per year. We’re definitely not saying this will happen, but it could unlock potential economies of scale as the payback period of adding a second production circuit would very likely be less than two years.

Should Focus indeed be able to penetrate the Brazilian markets and take market share away from the SSP-product, there’s no reason why the company shouldn’t consider expanding its operations as the Bayovar 12 project contains plenty of phosphate and could definitely support a higher production rate. Again, we’re not saying this will happen, but Focus Ventures has the optionality to do so.

3. Surface rights

In Peru, holding a mining concession generally does not include the surface rights, but Focus’ joint venture partner JPQ has signed an agreement with the local community which removes any potential risk. The joint venture partners were granted surface rights access for 99 years and a 30 year land use easement. So, unlike other projects in Peru where communities can play hardball, the Bayovar 12 project won’t have to deal with this anymore, as it has received the community approvals to work on the property. Of course, the community will have to sign off on the environmental permit and approve new drill programs, but having the surface access agreement is a very important step.

Also important is confirmation that the project is not located in a protected area, so the permitting process should be quite straightforward. Bayovar 12 is located in a desert region, and as you can see on the images of our site visit, there’s absolutely nothing going on at and around the Bayovar 12 claims, so the local population won’t be disturbed at all.

Focus insiders continue to buy more shares on the open market

After seeing the share price tank on the back of an uninspiring pre-feasibility study, Simon Ridgway (the CEO of Focus Ventures) has continued to buy more stock on the open market. Since the pre-feasibility study has been released he has added 503,000 shares to its total position whilst director Mario Szotlender also added 166,000 shares to his portfolio, indicating both key players seem to be convinced Focus Ventures is currently undervalued.

However, there’s one elephant in the room that will have to be dealt with. Focus Ventures borrowed money from Sprott to fund its acquisition of 70% of the Bayovar 12 project, and this loan (with an outstanding amount of US$3.5M) will be due before the end of the third quarter. So besides zeroing in on a feasibility study with improved economics, Focus Ventures will also have to deal with the refinancing of this loan. But, Sprott indicated at the recent Cambridge House show in Vancouver that they don’t want to own any projects even though the loan is secured against the project, so we think there’s a realistic chance for Focus to extend the maturity date of the loan.

Investment thesis

Yes, the economics of Bayovar 12 were worse than expected, but even after this first pass, Bayovar 12 is deemed to be economic. Sure, an IRR of 17.2% isn’t great but it’s still positive. Also keep in mind the after-tax NPV7.5% came in at US$253M, so Focus’ 70% stake in the project has a fair value of US$177M or approximately C$245M, and that’s definitely a great achievement.

However, the company is caught in a catch-22 situation. It’s trading so cheap that any additional share issue to fund the feasibility study (or construction) will have a devastating impact on the share count, resulting in a lower NPV/share. Whereas we were hoping for Focus to own 100% of this project further down the road, at the current share price it might make more sense to bring a partner in to jointly develop the property.

We are looking forward to see the company taking all the necessary steps to release a much better feasibility study and we believe the economics of Bayovar 12 will be much more appealing after fine-tuning the current inputs as part of a feasibility study. The IRR of the pre-feasibility study was disappointing but we have no doubt this will be a mine one day.

Disclosure: Focus Ventures is a sponsoring company, we hold a long position.