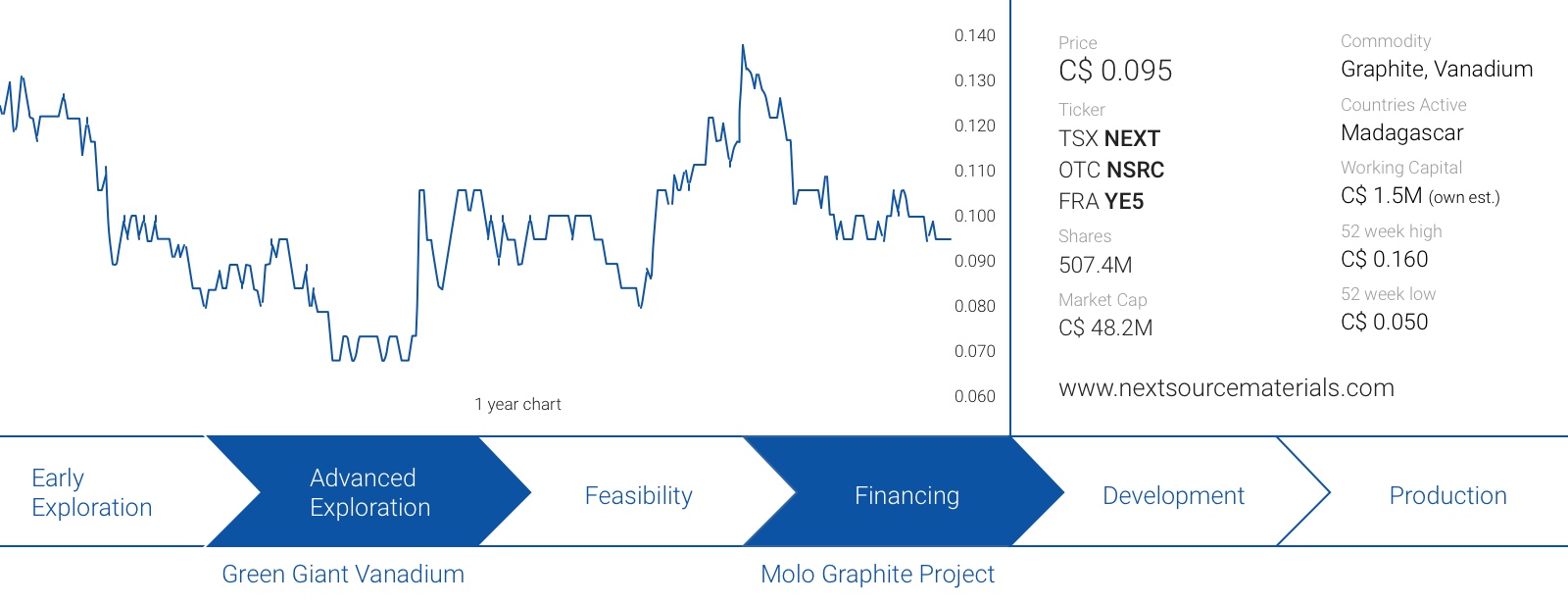

Hypes come and go and while most graphite focused companies that surfed the hype-wave have moved on to follow a new ‘hype du jour’, some companies have continued to work on their projects as they actually have merits. NextSource Materials (NEXT.TO) is one of those companies that didn’t have much to announce in the past 18 months since it released its feasibility study in the summer of 2017, but things have changed this year as the company’s Molo graphite project in Madagascar is now fully permitted and has secured a binding offtake agreement, with another one expected.

With negotiations to fund its unique, all-modular construction approach (more about that below) underway, we wanted to have another close look at the Molo project now that the graphite price is trading approximately 30% higher than the level used in the feasibility study as base case pricing.

Ticking two important boxes with the mining license and environmental permit

Advancing the Molo graphite project accelerated tremendously in the first few months of 2019. In February, the Madagascar government granted the company a 40-year mining license on the Molo project. As there’s no upper limit on the volumes that are allowed to be mined under this permit, NextSource can immediately build a plant with an optimized capacity based on the offtake agreement it has signed and additional ones it is expected to sign in the near future.

Approximately two months later, the mining license was followed by a definitive global environmental permit, which was the last outstanding important permit. There are some smaller permits outstanding, but the mining license and environmental permit were the most important boxes to tick.

A quick glance at the graphite market and the impact on the economics

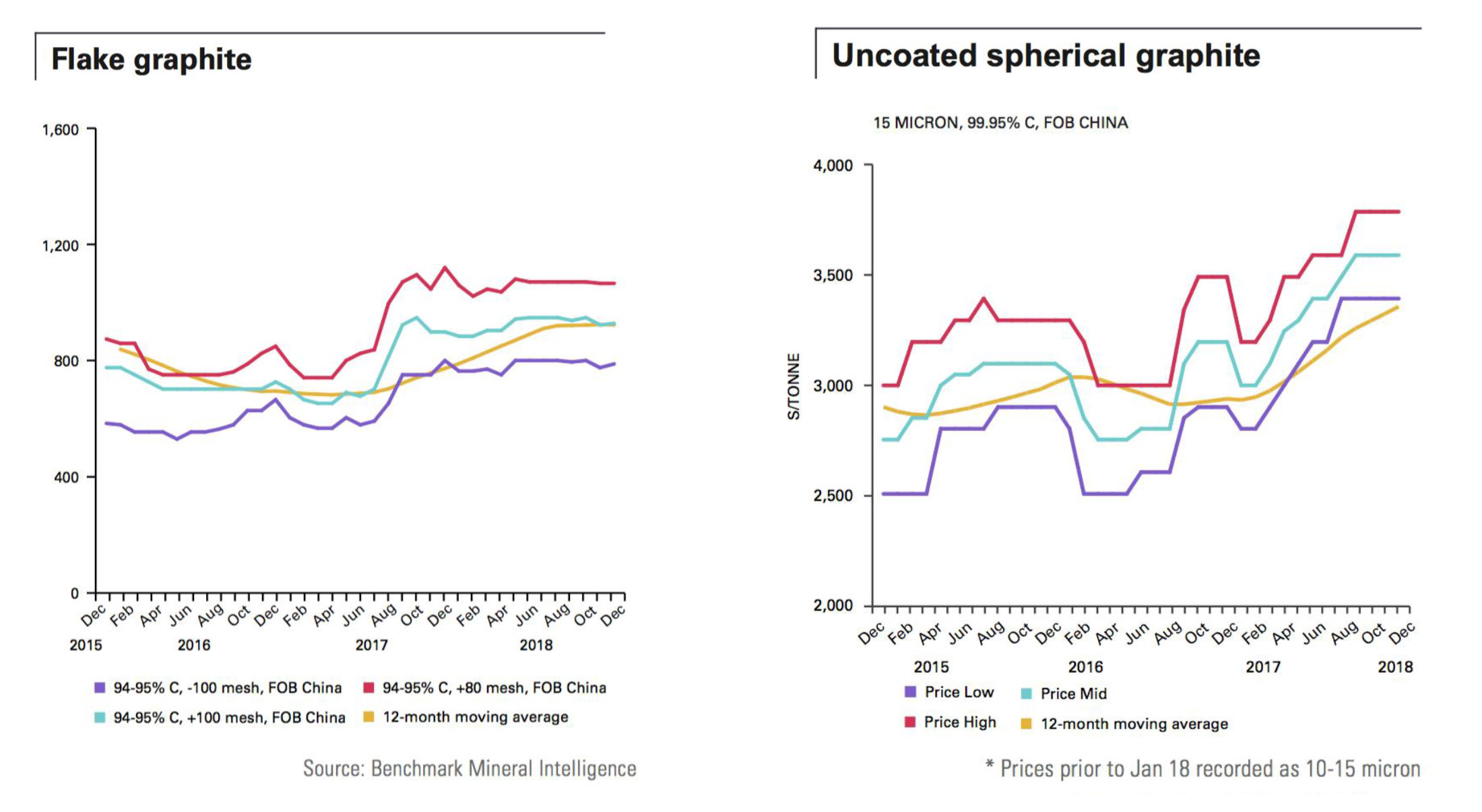

There’s no such thing as just ‘one graphite product’. The quality of the graphite (and thus the pricing) is based on two different parameters: the size of the flake (bigger is better) and the purity of the product after processing (higher carbon content is better).

If you’re trying to produce fines with a low carbon content, you’re hooped as there isn’t much money to be made in that segment of the market. A good example would be Syrah Resources (ASX:SYR) which used to be one of the market’s darlings in the graphite space as it owns a large graphite project in Mozambique which it successfully financed, built and which is currently ramping up towards its targeted nameplate capacity. But in the graphite sector, bigger is not always better as the quality of the graphite product is even more important than the total output.

That’s clearly visible in Syrah’s guidance. In its most recent update, it confirmed its production guidance at 250,000 tonnes of graphite, to be produced at an operating cost of around $400/t by the end of this year (note this is just the C1 cash cost and does NOT include any domestic transportation to a port and does not include any sustaining capex). That sounds great. But then you need to look at the quality of the product: the majority of the graphite that will be sold are categorized as ‘fines’, and as you can see on the previous image, the sales price for fines is usually quite low.

And indeed. Syrah is guiding for an average revenue of $460-470/t (the average selling price in Q1 2019 was $469/t), indicating its operating margin per tonne of product will be just $60-70/t (based on the expected production cost by the end of this year). Which very likely means the company won’t make any money this year.

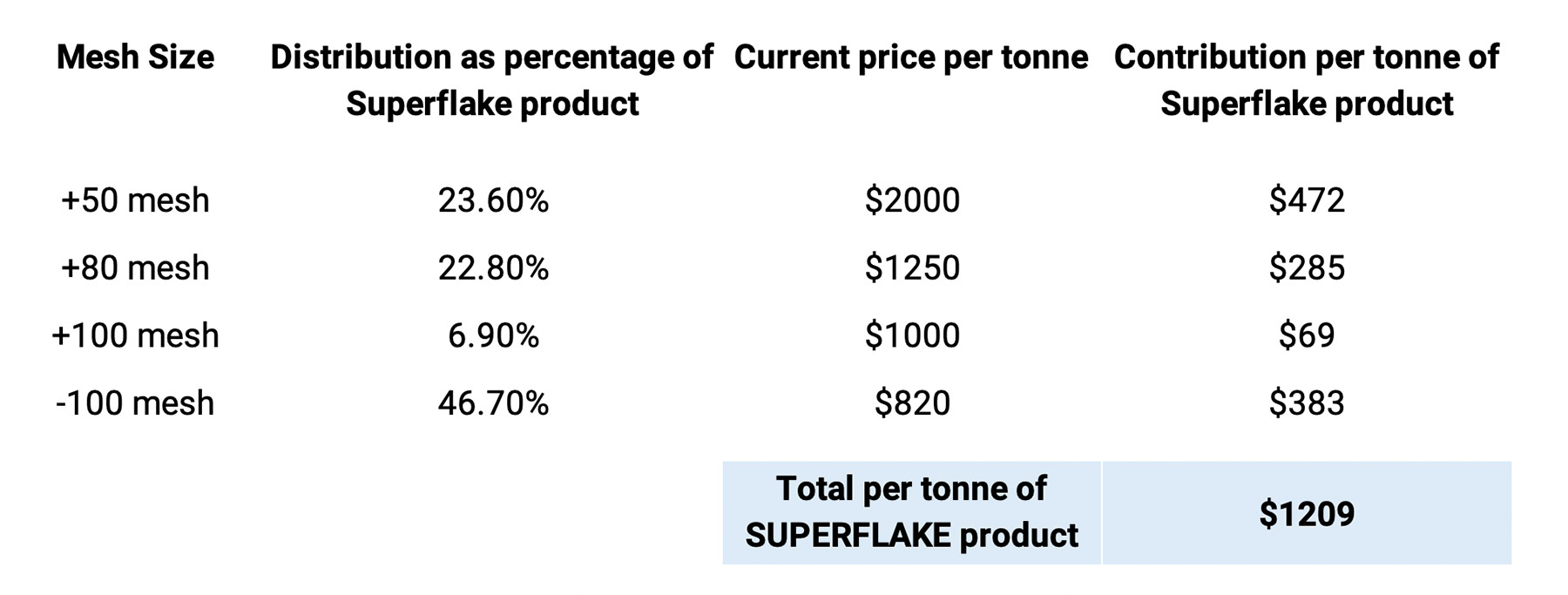

NextSource’s focus in the past few years was to make sure a large part of its graphite production would qualify as ‘high revenue’ production (i.e. producing as less ‘fines’ as possible). And indeed, if we have a closer look at its SuperFlake product (which is a registered trademark), the distribution model shows almost 50% of the Molo deposit contains large and jumbo-flake, and over 23% alone of just the jumbo-flake. Approximately 80% of the SuperFlake concentrate consists of at least medium-sized flakes and small and fine flakes represent just over 20% of the output. In short, NextSource has a flake size distribution well above the global average.

And that’s good news for the expected revenue. Although the exact pricing mix will be determined in function of the market circumstances when the SuperFlake product gets shipped to the offtakers, we are in a position to provide some sort of back of the envelope calculation based on the currently known prices for the different flake sizes of the graphite.

Port of Ehoala at Fort Dauphin (left) – Madagascar location and potential markets (right).

The impact of the current graphite price levels on the economics

Based on recent graphite pricing provided by Benchmark Mineral Intelligence (here after ‘Benchmark’), the (rounded) graphite prices for the 4 parts of the SuperFlake product are:

This results in an average weighted selling price of $1209/t. There’s one other important element we need to take into consideration here; the prices provided by Benchmark are FOB China, which means the shipping expenses to the end consumer have NOT been taken into account yet. And that’s important as NextSource Materials has included its shipping expenses in its operating expenses. So if we want to compare apples to apples, we either need to remove the shipping expenses from the CIF operating cost of $688/t, or add these expenses back to the expected revenue per tonne.

For simplicity sake, we will just add it back to the revenue as that will make it easier to explain our point. After all, this is a back of the envelope calculation. NextSource’s feasibility study expects a domestic shipping cost of $133/t to truck the graphite from the mine to the port at Fort Dauphin, while seaborne transportation to Rotterdam was estimated to be $122/t. While the domestic cost to truck the graphite will remain unchanged, we need to be mindful that approximately 20% of the $688/t in operating expenses consists of shipping expenses that aren’t included in the FOB China price we quoted before.

Let’s remain conservative and add $91/t back to the sales price, and use $1300/t as a rounded number.

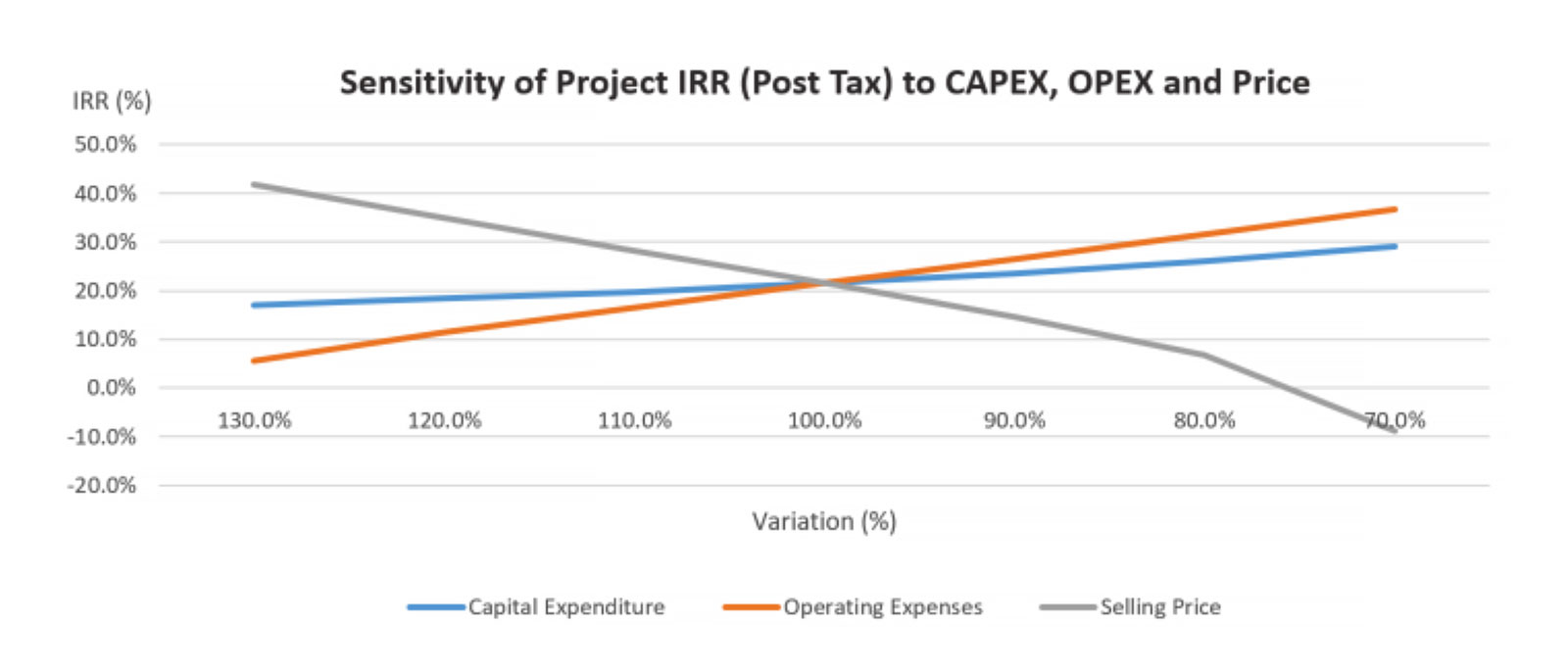

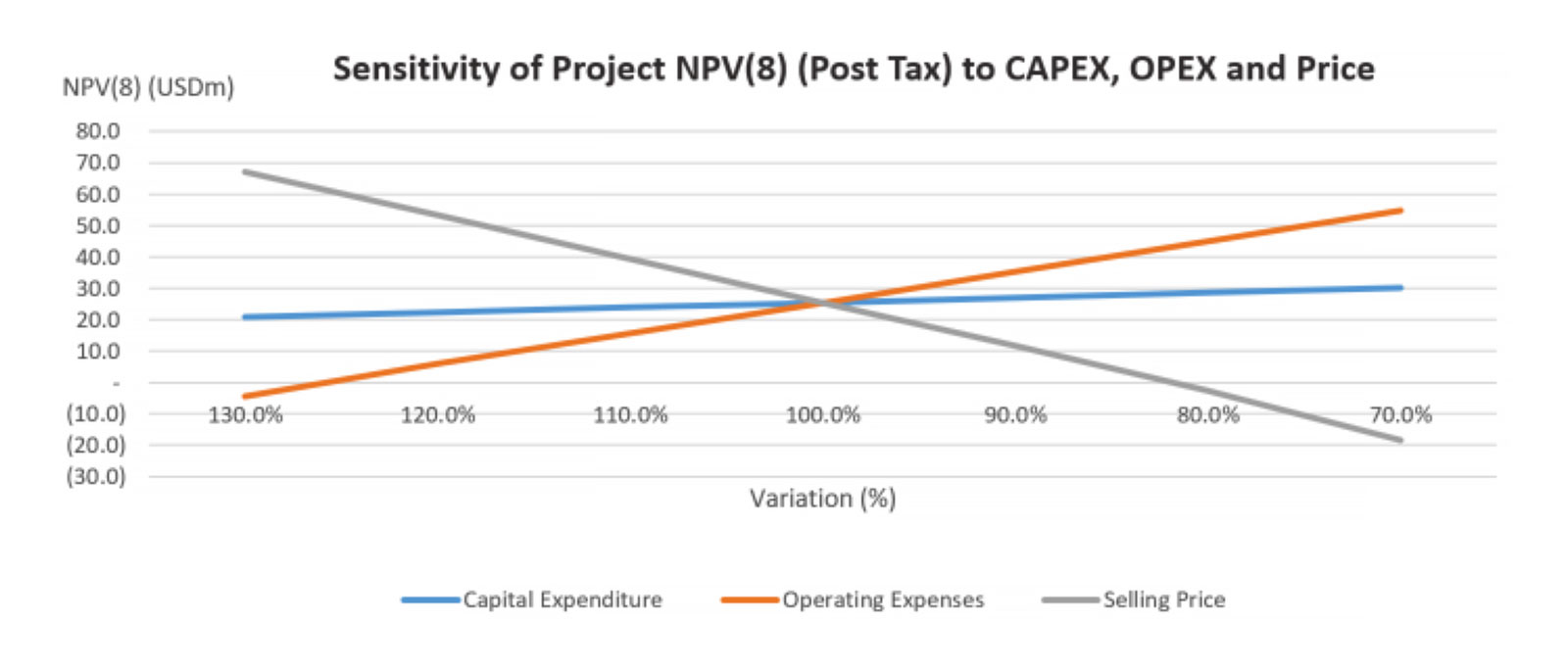

This has important implications for the Internal Rate of Return and Net Present Value of the project. As a brief reminder, these are the basic inputs of the feasibility study, which shows the returns based on just the first module:

As you can see, NextSource used a CIF-based production cost of almost $700/t which results in a net margin of $326/t. That’s very respectable and this results in an after-tax NPV8% of US$25.5M. That’s indeed less than the current market capitalization (before even taking dilutive effects of construction financing into account) but as you may have guessed by now, there’s more to the story.

First of all, according to our back of the envelope calculation, NextSource’s SuperFlake® product could sell at around $1300/t using the current indicative price deck. This means the operating margin would increase from $326/t to $612/t. And that’s an important development as this changes the whole investment case. Fortunately, the company’s Feasibility Study includes a sensitivity analysis showing what happens if the total revenue per tonne increases by 10%, 20% and 30%. Considering $1300/t is almost 30% higher than the $1014/t in the base case scenario, let’s have a look at how the Internal Rate of Return and NPV8% are evolving based on the higher graphite price.

The Internal Rate of Return increases to in excess of 40%, while the after-tax NPV8% increases to almost US$70M.

And finally, keep in mind this is based on just ONE module of 17,000 tpa that will mine and process just 7.5 million tonnes of the 100 million tonnes in the measured and indicated resources and almost 40 million tonnes of inferred resources. Sure, the average grade of the total resource (6.3%) is a bit lower than the average grade in the single module mine plan (8.1%), but the impact of the lower grade could be mitigated by A) economies of scale at the processing plant and B) getting better shipping quotes as more product will be shipped making it more economic to ‘fill’ a shipping vessel and demand better terms.

It’s important to realize that the initial 17,000 tpa scenario is just the first stepping stone for the project. And that seems to be something the market and investors have lost track of; NextSource’s intention has always been to roll the Molo project out in phases. The first phase of 17,000 tonnes per annum is designed to verify their product with run-of-mill material for the graphite market, while the second phase is intended to make the project more profitable with increased market share by tripling production to 51,000 tonnes per annum. The initial capacity is just a stepping stone to quickly expand the production rate.

Phase 2 would be much more profitable than simply adding two more ‘Phase 1’ modules as the additional “scaled-up” plant would achieve economies of scale for both CAPEX and OPEX.

As the graphite will be shipped in 26 tonne containers, a 17,000 tonne per year production scenario would need just over 650 containers. A 50,000 tonne per year operation would need to secure cargo space for 2,000 containers, which could qualify for bulk pricing when negotiating with the shipping companies. So we think the currently assumed $122/t for seaborne transportation could drop a bit from the current pricing of almost $3,200 per container.

View of the Molo Project area showing the nature of the vegetation (left). Trenching for the Bulk Sample on Molo, May 2013 (right).

SuperFlake is in high demand – this should unlock additional economies of scale

To make sure the capex remained manageable for a junior company, NextSource focused on a modular build approach for its mine. It would start with one operating module which would produce up to 17,000 tonnes of graphite product per year at an astonishingly low estimated CAPEX of just US$23 million, which includes four months of working capital. How they are able to build it for such a low capital cost is due to the cost-advantages of using an all-modular build approach. And the cash flow generated from this first module would fund the construction and commissioning of an expanded plant.

At least, that was the original plan. Unlike most juniors which need to reset their expectations when reality sets in, NextSource Materials will very likely be able to do much better than its own expectations. It signed a binding offtake agreement with a major Japanese graphite trader which agreed to purchase 20,000 tonnes of product per year for an initial period of 10 years. Not only is this already more than the anticipated 17,000 tpa output of the first module, this agreement actually comes on top of advanced-stage discussions (which culminated in a Letter of Intent) with a European graphite trader for 17,000 tonnes per year.

Should the second LOI also be converted into a binding offtake agreement, NextSource will have to upscale its production plans and immediately build a plant with a capacity sufficient to fulfil its obligations under both offtake agreements. That will increase the initial capex as well as the working capital needs (which was estimated at US$3.1M in the 17,000 tpa scenario), but that shouldn’t be a big hurdle.

Next stop: construction funding

Now the graphite prices are strong and all relevant permits (the construction permit and environmental permit) have been received, the logical step that comes next is to secure funding to build the mine.

The initial capex was estimated at US$18.4M (including a 10% contingency allowance, excluding the aforementioned four-month working capital), but NextSource will have to decide about its initial plant throughput. Installing two modules at the same time would very likely increase the initial capex to US$33M (our own estimate) and we would expect the majority of the construction funding to be debt-based (we imagine French banks would be interested in providing debt, while the Japanese offtake party could also open doors to Japanese funding).

Unfortunately there will be an equity component as well (unless one of the offtake parties is willing to pre-pay for shipments), but considering the most important permits have been issued, the binding offtake agreement and the strong graphite price, we are secretly hoping NextSource will be able to attract a strategic investor who sees the value of a graphite mining operation with a multi-decade mine life.

The next weeks and months will be important for NextSource as it will have to take a few decisions and raise the money.

With a binding offtake agreement for 20,000 tonnes per year (which should result in a net operating cash flow of US$12M per year based on the current expected margins) and the current strong graphite price, we think it makes a lot of sense for NextSource to immediately build a larger 34,000 tonne per year module. It could then either sell the ‘excess’ 14,000 tonnes per year to the second potential offtake party, enter into smaller offtake agreements, or sell it on the market. At the current graphite price, a 34,000 tonne per year module would generate approximately US$20M in net operating cash flow (and an estimated US$14-15M in free cash flow after deducting the 20% corporate tax rate in Madagascar and assuming an 11.5% interest rate and a 60% debt funding ratio). This means that even after deducting taxes and interest payments on the construction-related debt, the payback period will remain very short.

Investment thesis

NextSource is arguably one of the best graphite projects in the world that investors simply do not know about. While the initial graphite hype faded away, NextSource’s management team remained committed to the Molo graphite project as it strongly believed in the odds to develop a profitable mining operation. The 2017 feasibility study has proven them right as the independent study confirmed the viability of Molo, indicating the project would have healthy operating margins at a base case price of just over $1000/t.

Meanwhile, the basket price of the SuperFlake product has increased by approximately 30%, making the returns even more attractive.

Now all relevant permits have been secured, it’s up to NextSource’s management team to secure funding at an acceptable cost. With an operating margin of 45% and a binding offtake agreement, we are feeling confident to see this project moving forward. Considering the construction period is estimated to be just 9 months, NextSource Materials could be cash flowing by the summer of next year…

The author has a long position in NextSource Materials. The company is a sponsor of the website. Please read the disclaimer

Pingback: NextSource Materials Featured in Caesars Report Analysis | Investing News Network

I am impressed. Held this stock for a long time. Now I may invest more. 😊

I would worry about Black Rock Mining Ltd on the ASX BKT. Syrah is not the competion for NEXT . Both Next and Syrah have to worry about Black Rock as Black Rock is going to be the big mover in the Graphite Space into the future .

Worth the comparison. But BKT has the edge

moureeses