Sierra Madre Gold & Silver (SM.V) announced the acquisition of the past-producing La Guitarra silver-gold mine in Mexico in 2022 and kicked off an aggressive plant refurbishment plan in 2023. An easy decision as there were no permitting hoops to jump through considering the previous owner of the mine kept all relevant operating permits in good standing.

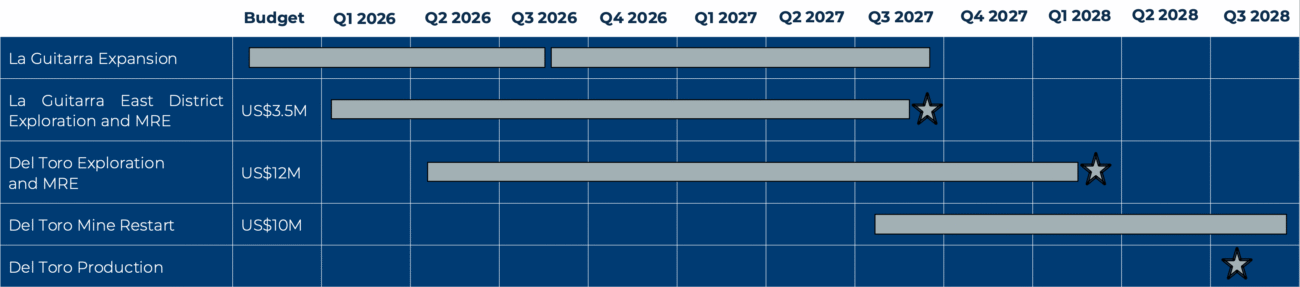

This allowed the company to move from acquisition to commercial production in a record time, as Sierra Madre declared commercial production at La Guitarra in January 2025. This now makes it easier to have a closer look at its production profile, and more importantly, its cash flow profile. After all, the cash flow will be needed to increase the capacity of the processing plant as Sierra Madre expects to reach a capacity of 800 tpd by the end of this quarter, with plans to complete a further increase towards 1,200-1,500 tonnes per day by Q3, 2027.

One of the key elements we appreciate in Sierra Madre’s structure is its social responsibility. Not only does every employee receive stock options (so everyone wins if the share price is doing well), there also is a cash profit sharing agreement. In Q1 2026, for instance, C$424,000 was recorded in the books as a profit sharing agreement for the labor force.

Reviewing the Q1 results

Any investor who just looks at the headline results may be disappointed with Sierra Madre’s first quarter. But as you can imagine, there is a good explanation for the lower than expected production and higher than expected production costs.

First things first. In the March quarter of this year, the mill processed just under 41,700 tonnes of rock, which once again is a quarterly record, and it translates to a throughput of 463 tonnes per day (that’s based on the calendar days, as Q1 included new year’s, the throughput per operational day was likely slightly higher). That’s pretty decent. The main culprits and causes of the lower production of just over 143,000 ounces of silver-equivalent, of which 58,500 ounces were actual silver with the remainder of the silver-equivalent consisting of gold.

Whereas the plant processed rock with an average grade of almost 141 g/t AgEq in Q1 2025 and recovery rates in the high 70% range and seeing a further increase to a head grade of just under 155 g/t in Q3 2025, the 137.78 g/t silver-equivalent in combination with recovery rates in the low-70% range were the main issue.

But fortunately there is an explanation. First of all, the mining operations at Nazareno and Coloso were still ramping up. Although new production faces have opened up, there was quite a bit of ore coming from outside the resource area, which were lower-grade sections which weighed on the average grade. This was development waste rock, that was able to be mined, milled and processed at a profit; lengthening the life of mine and leaving higher grade ore for the future. Having said that, the grades should improve as 2026 progresses as more fresh ore from the resources will be mined and processed, and this should restore the head grade.

The recovery rates may require a bit more work. Sierra Madre disclosed it is still working on optimizing the blend from its three operating mines, so it may take another few quarters – especially with Nazareno and Coloso still in the ramp-up phase – to further refine the recoveries.

Meanwhile, the combination of all of those elements weighed on the Q1 performance. The cash cost came in at $42.55 per ounce of silver-equivalent while the all-in sustaining cost jumped to almost $54/oz.

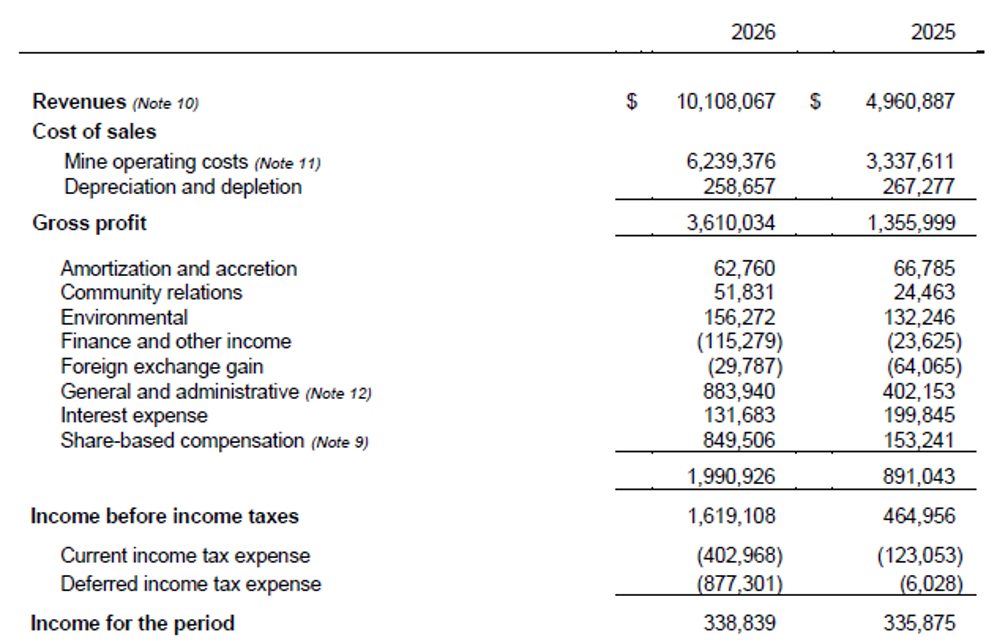

But despite this, the company remained profitable (and we think it’s fair to say Sierra Madre took advantage of the silver price). As the income statement below shows, the company generated a net profit of US$0.34M (almost C$0.5M) in the first quarter. The underlying net profit would be even higher if it wasn’t for the deferred tax expense as the pre-tax income more than tripled compared to the first quarter of 2025 despite seeing the G&A expenses double while the (non-cash) share-based compensation expenses (approx. $1m) increased as well.

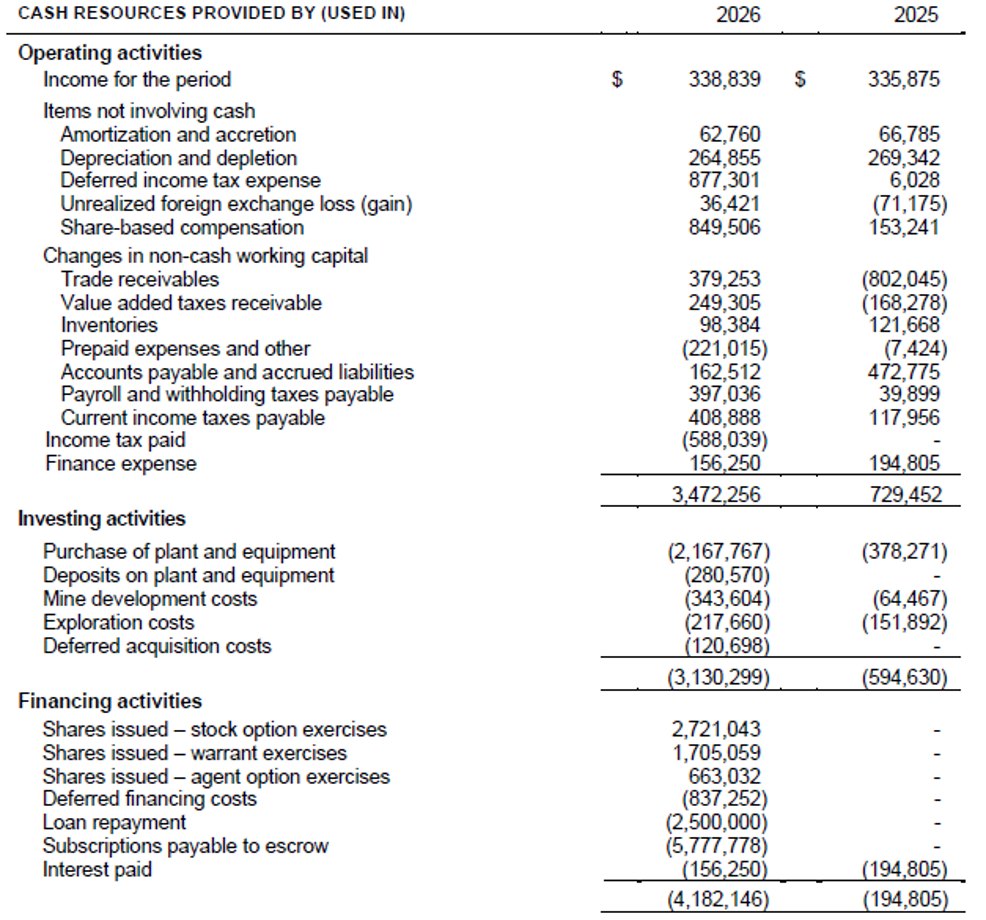

Looking at the cash flow statement, Sierra Madre reported a positive operating cash flow of US$3.5M, which included a positive change in the working capital position of approximately US$1.5M resulting in an underlying operating cash flow of US$2M. Not sufficient to cover the capex and the US$2.5M loan repayment (a portion of the outstanding balance to First Majestic was repaid), so the company had to dip into its treasury. But thanks to the strong share price performance, Sierra Madre reported a total cash inflow of in excess of US$5M related to the exercise of options and warrants.

That cash inflow helped to keep the balance sheet in a rather comfortable position.

At the end of Q1, Sierra Made had US$13M in cash and short-term investments on the balance sheet, and a positive working capital position of approximately US$14.4M.

So despite the high operating costs and lower than expected production, Sierra Madre is not painted into a corner and has plenty of fire power to improve its financial performance. And as we will explain later in this update, the completion of the Del Toro mine acquisition will unlock in excess of C$20M in additional cash as subscription receipts are converted into common shares, and the cash moves from escrow to Sierra Madre’s bank account.

Sierra Madre is currently also in the process of commissioning additional diesel-powered generators. Last year, the company had to deal with some serious power outages at the plant and with an initial 1,250 kW generator for Coloso and Nazareno mining operations and two new 1,500 kW generators to support the processing plant, the company’s operations should be affected less by weather-related power outages. And as diesel is still relatively cheap in Mexico, this likely was an easy trade-off to make for the company.

The capacity expansion remains on track

It would be completely wrong to look at Sierra Madre Gold & Silver from a backward looking perspective. As mentioned in the introduction, the company is going full steam ahead to deliver an initial increase of the production capacity to 750-800 tpd by the end of the current quarter. An additional cone crusher has already been commissioned, an oversized ball mill is being installed and the overhaul of the electric system means the equipment that’s currently being installed can go up to 850 tpd.

While the construction of the additional milling capacity is ongoing, Sierra Madre also dealt with the other key elements that are required for a capacity upgrade. A thickener tank is currently under construction with an anticipated completion date later this month. An important part of the expansion plans, as the thickened tailings will allow for a substantial portion to be pumped directly into the open stopes below the San Raphael mine level.

And while the activities at the processing plant are ongoing, it will of course be important to also get enough rock from the mine to the plant. Four additional haul trucks were purchased and will be deployed to bring mineralized material from the Coloso mine to the plant, while two new scoop trams have already been delivered.

And in order to be absolutely certain the company can A) fill the mill at a rate of 800 tpd and B) ensure the further capacity increase to 1,200-1,500 tpd is feasible, it has engaged a special services contractor to provide equipment and manpower to bring the Coloso and Nazareno mines up to speed. Once the contractor reaches its cruising speed at the two satellite deposits, Sierra Madre will pull its staff and equipment and redeploy everyone and everything at the main La Guitarra mine to ensure the most efficient production scenario at all three mines.

The acquisition of the Del Toro mine could be a game changer

At the end of last month, Sierra Madre announced it has received approval from the Mexican antitrust agency to complete the acquisition of the Del Toro silver mine in Mexico. This was a much-anticipated move (there was no real reason why any antitrust agency would object, but that’s just part of the process in Mexico), and now allows the company to go ahead and finalize the acquisition.

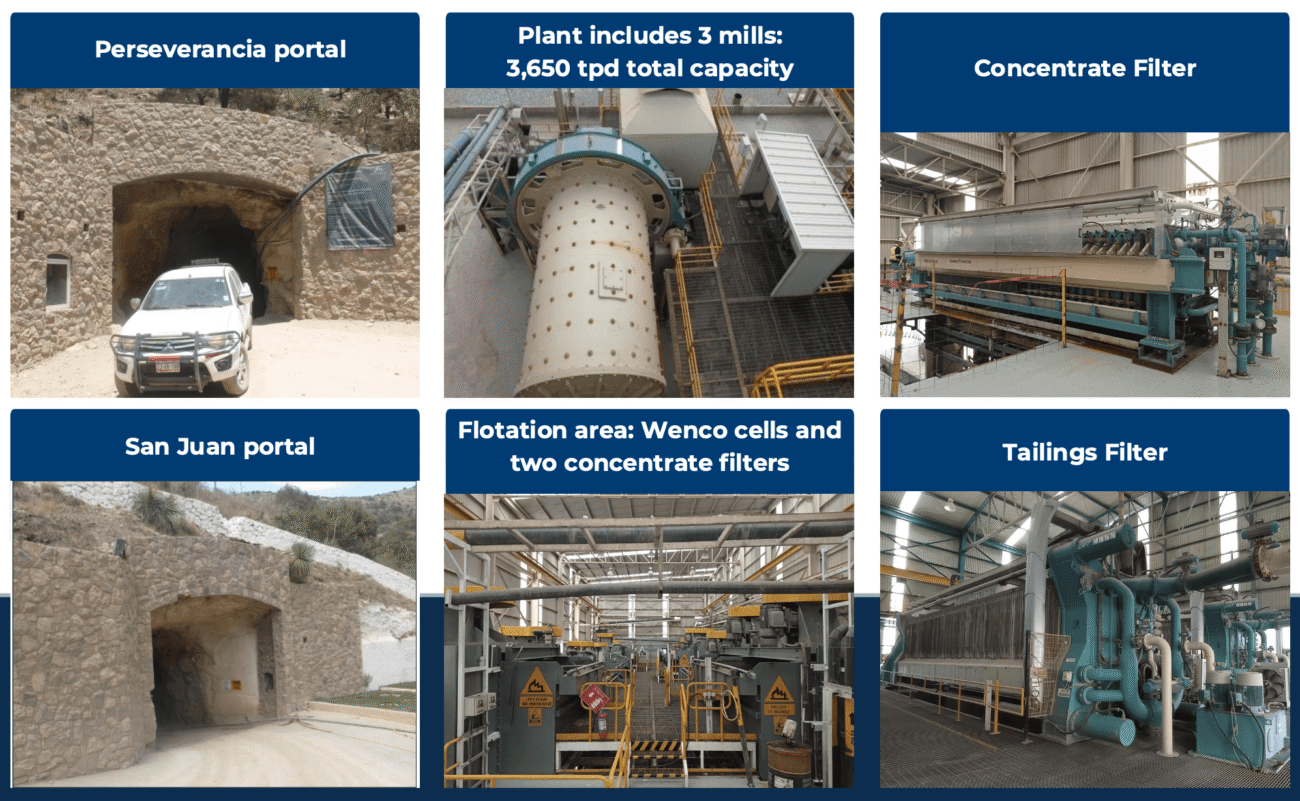

As we explained before, the Del Toro mine is a fully permitted and past-producing underground silver-gold-lead mine that was operational for the better part of the 2010s. All the relevant processing equipment is still on site, including three mills with a combined capacity of approximately 3,000 tonnes per day. You can read our extensive review of the asset here .

The upfront cost for the acquisition is very reasonable with a US$20M cash payment and US$10M payable in stock to First Majestic Silver, the seller, followed by a series of milestone and success payments totalling US$30M in cash or stock (at Sierra Madre’s discretion). This means the total price tag to complete the acquisition is just US$60M, of which some payments are highly uncertain: there is for instance a requirement to make a US$10M cash or stock payment when the mine achieves commercial production at 4,000 tonnes per day (which would be a 33% increase from the current official capacity of the processing plant) within 60 months of closing. Another US$10M payment is only due when the project hosts at least 100 million ounces silver-equivalent within four years after the closing date.

Both those milestones are highly uncertain but if they would happen, it would be great news as it would establish Del Toro as a robust producer with a long mine life given a 100Moz AgEq resource base, so even if both milestones would be met, we are certain Sierra Madre would gladly make those payments.

In any case, Sierra Madre will have plenty of cash to cover the initial cash payments. Concurrent with the acquisition, the company entered into an agency agreement to raise C$57M in subscription receipts priced at C$1.30, and convertible in common shares upon closing the acquisition of the Del Toro mine.

So just over C$50M will flow into Sierra Madre’s treasury after taking care of the finders fees and legal expenses.

That is of course more than sufficient to cover the C$27M initial cash payment (US$20M at the current approximate exchange rate) with likely north of C$20M in cash being retained on the balance sheet and ready to fund any exploration and redevelopment activities the company may have in mind. The share count will increase towards ~240M shares after taking the impact of the sub receipt financing into consideration.

Sierra Madre Project Timeline

Conclusion

Sierra Madre is currently firing on all cylinders. We are looking forward to seeing an update on the completion of the capacity expansion at La Guitarra and hopefully we can see an initial game plan for the soon-to-be-acquired Del Toro silver mine as well.

And that’s what investors should focus on. Not the annualized 0.6Moz AgEq production rate based on the Q1 numbers as that will prove to be not very relevant when A) the grades increase as Coloso and Nazareno ramp up and B) the production capacity increases by 50-60%. Completing the Del Toro acquisition will also bring in north of US$15M in cash, which will boost the total working capital position to around US$30M (with the net proceeds of the sub receipt financing earmarked for Del Toro related expenses).

Meanwhile, the existing cash and working capital should provide plenty of liquidity to initially complete the Phase 1 capacity expansion as well as the Phase 2 capacity expansion which will be the focus for the subsequent twelve months.

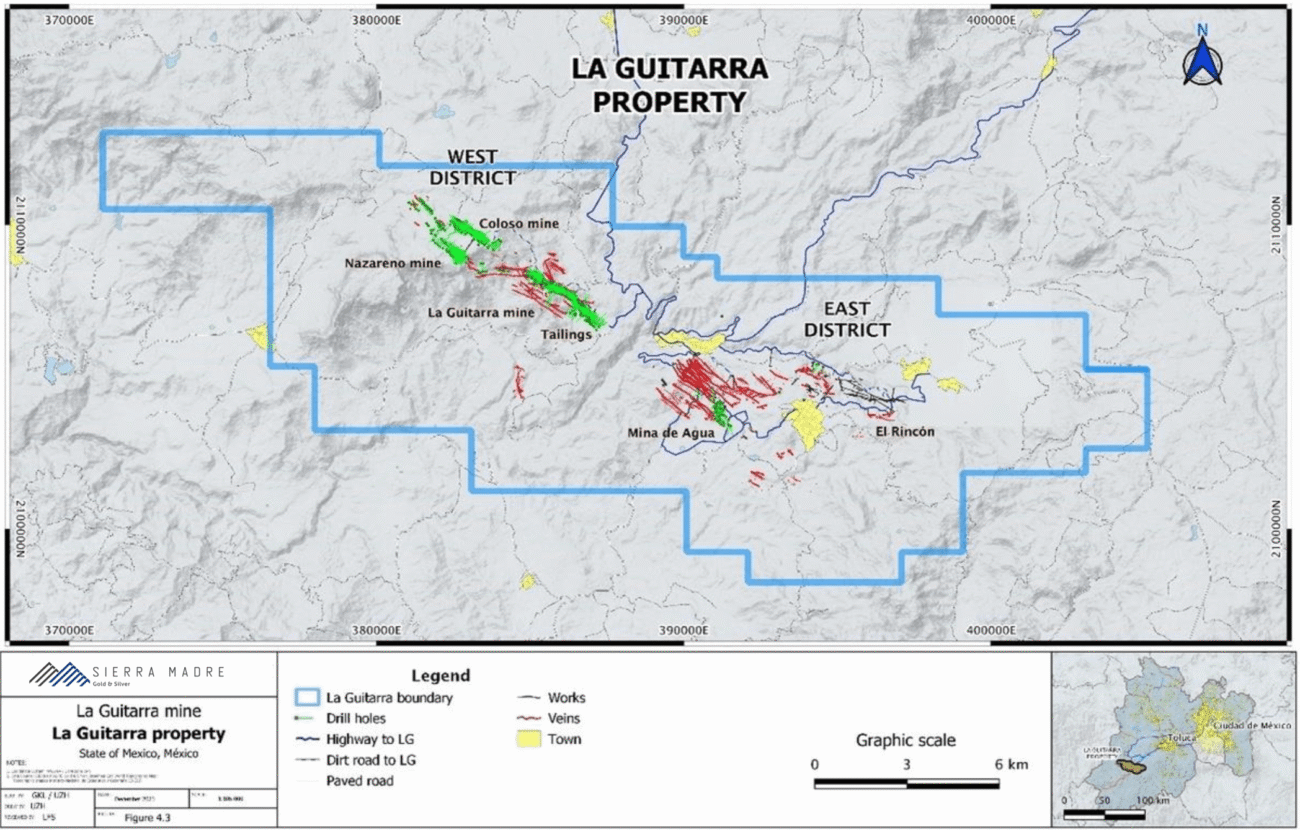

Meanwhile, an active exploration program is underway at La Guitarra, and we expect the technical teams to start warming up to tackle Del Toro soon after the acquisition officially closes.

Disclosure: The author has no position in Sierra Madre Gold & Silver. Sierra Madre currently is not a sponsor of the website, but has been one in the past. This post is for educational purposes only; be mindful investing in junior mining stocks is risky and you may lose your entire investment if things go wrong. Please read the disclaimer.