Camino Minerals’ (COR.V) share price has continued to slide since reaching C$2 in April last year on the back of an interesting copper discovery in Peru. Whilst investors initially seemed to be speculating on Camino discovering one of the typical Peruvian large-scale copper porphyry deposits, the interest in Los Chapitos tanked.

Undeservedly so.

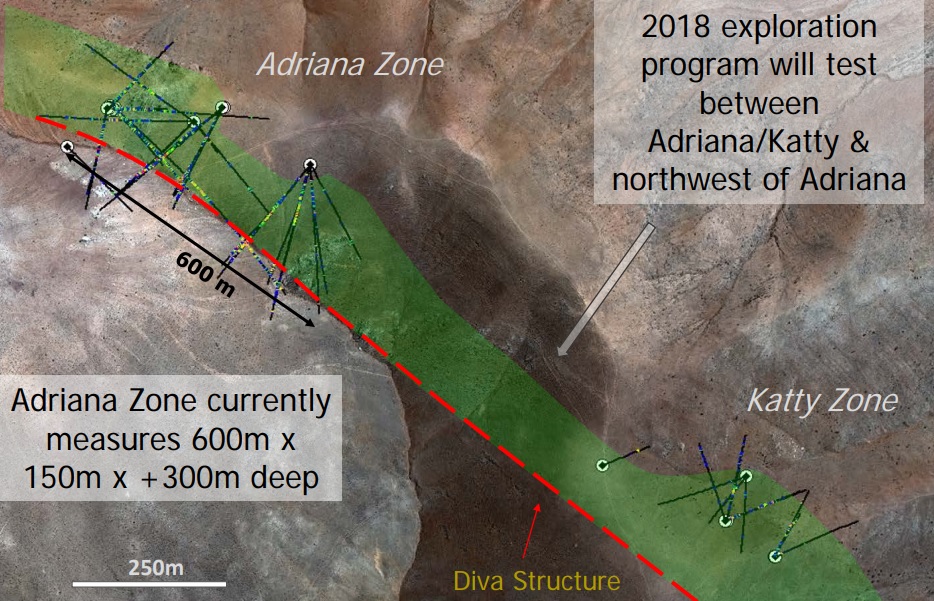

Camino Minerals has done pretty much everything right as every single step it took in 2017 was aimed at proving up the value of Los Chapitos’ three deposits. Recently, the company announced the drill results of an additional 7 holes at the Adriana zone, of which 4 were drilled as a step-out of 100 meters towards the southeast of the currently known Adriana zone. With almost 50 meters at 0.82% copper, 45.5 meters at 0.65% copper and 75 meters at 0.45% copper (with the soluble copper content approximately 80-90% of the quoted percentages), the step-out drill program was a great success. And the final three holes of the program confirmed the relatively thick copper mineralization with 33 meters at 0.54% copper, 60 meters at 0.4% copper and some higher grade intervals within the broader intercepts. We estimate the Chapitos project currently contains in excess of half a billion pounds of copper, based on the size of the mineralized envelope.

Long story short, we feel Camino Minerals is worth more than the current share price, and we think there’s a natural ‘shift’ going on in the type of investor who owns Camino stock these days. The early speculators who were hoping for a large copper porphyry deposit appear to be selling out and this could be an opportunity for copper investors interested in a copper oxide play.

We are anxiously awaiting a first resource estimate at Los Chapitos and – perhaps even more important – the results of metallurgical studies to determine the recovery rates of the copper in an acid solution which will immediately show whether or not the deposit is viable. As a reminder, 0.5% copper has an in situ value of $33/t using a copper price of $3 per pound and assuming a recovery rate of just 65%, the recoverable rock value is approximately $20/t. This sounds low, but should be sufficient considering the low-cost nature of open pit mining. The jury’s out, but no verdict has been reached (contrary to what a C$0.37 share price might indicate).

Go to Camino’s website

The author has a long position in Camino Minerals. Please read the disclaimer