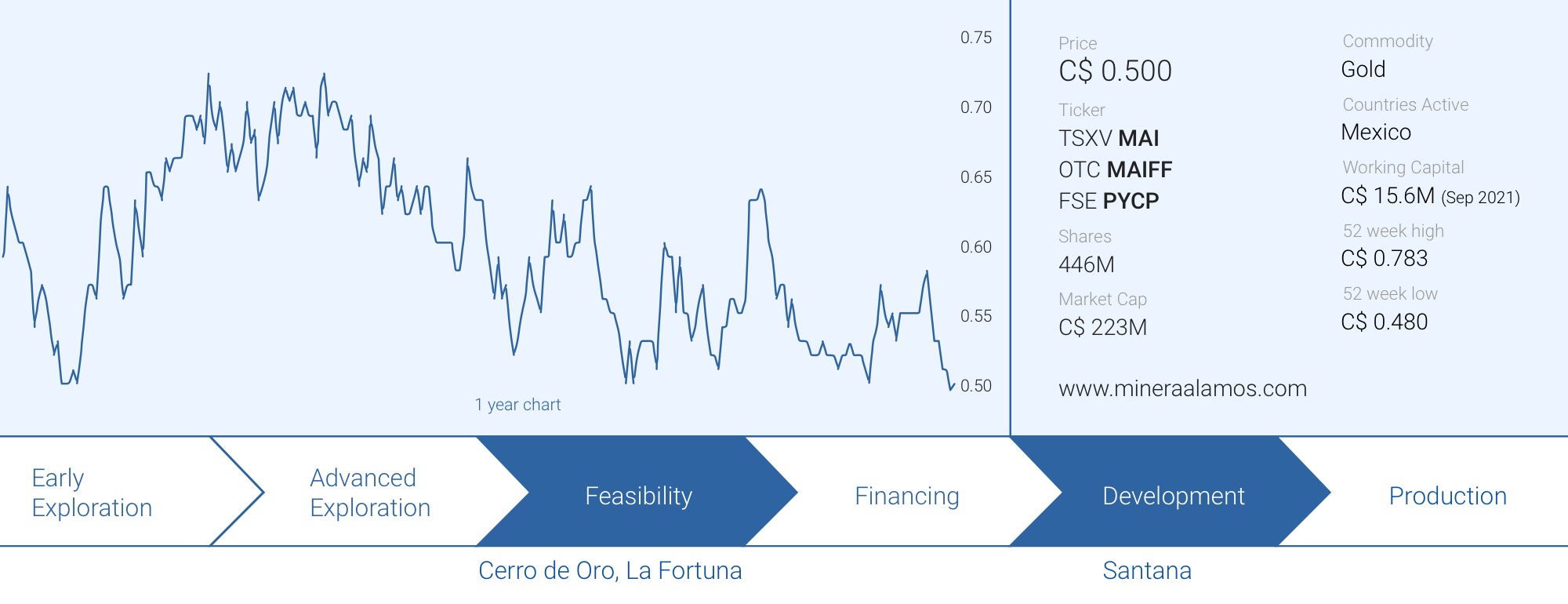

Minera Alamos (MAI.V) has been taking the unconventional route to bring its Santana gold project in Mexico into production. Rather than relying on a lengthy process of completing a PEA, PFS and DFS, Minera relies heavily on its in-house talent on making the first mine work. CEO Darren Koningen has done this before and as the Santana mine required just a high single digit capex to get started, there was no lengthy process to get the approval of third party financiers: Minera is doing everything in-house, using equity.

2022 will be the year of the truth for the company as the Santana mine will be reaching the free cash flow positive stage sooner rather than later and the cash flow from Santana will be used to develop the rest of the asset portfolio with the Cerro de Oro project and the Santana Expansion project to be developed using the Santana phase I cash flow.

We sat down with President Doug Ramshaw to discuss the recent events and to get a better understanding of how Minera Alamos is approaching 2022.

Santana

In your December update on the Santana mine you mentioned about 1,200 ounces were ‘removed’ from the processing plant and presumably were shipped off to be refined?

That’s correct – we decided upon using a different stripping plant for the final processing and that doré is presently being refined in the US.

It’s always a risk to actually develop a gold mine without having ‘official’ studies although it’s understandable a knowledgeable and experienced team doesn’t need a piece of paper to tell them what they already know. In your recent updates you seemed to imply both the grade, tonnage and reagent consumption are in line with your internal expectations and that was perhaps the most important element of your update. Is everything still going according to plan, and what are the biggest risks for the Santana production process right now?

Sure; that is the perception and our news has to be heavily laden with cautionary language as a result, however, I could easily argue that if we look at say our metallurgical understanding it is superior to what would be understood from a company with a PFS or FS filed nicely with a little bow on Sedar. Most metallurgy sections of 43-101 reports don’t have the benefit of a 50,000t pilot heap leach pad evaluating three different lifts of material: run of mine, coarse crushed and fine crushed and agglomerated. The resource itself, while internal, is one that is drilled off on almost 25 m centres so again very robust information to base decisions on and when looking at open pit heap leach projects I think resource reconciliation and metallurgical understanding are absolutely the two most important factors to have paid great attention to.

As for biggest risks moving forward, perhaps a slower ramp up of operations, although we don’t need a particularly high monthly production rate to cover costs, I see the impatience in the market at large and so while not rushing things we are very aware all eyes are on Santana and it needs to perform, not just at a solid pre-commercial rate but also as a consistent and profitable operation moving forward. That said we do not plan to rush any decisions to appease the impatient. When one thinks we spent a year permitting the mine, a year constructing the mine and are now going through the ramp up then if it takes some extra time to be comfortable that everything is good in an ongoing way then we will take that time. The ramp up isn’t just about getting the project to a particular point it is also about ensuring it is optimized in many different ways during that ramp up phase.

Some aspects of Covid are somewhat in the rear-view mirror, however, what we see now is what we are seeing across sectors of industry and that’s supply chain issues that I think probably still need another 12-18 months to work through the system. We see these impacts affecting contractors with long delays in delivery of maintenance parts etc. that have likely begun to bite more recently as 2020 inventories disappeared.

Having started up Santana, we are seeing firsthand the issues that the economy is facing with the supply chain and we will use this knowledge to work to mitigate these same risks when planning the Cerro de Oro development. I think it will prove invaluable as we generate positive free cashflow as the year continues that we think about how we can minimize the impacts of the Cerro de Oro construction by using it to make advances toward long lead items and simply building up inventories of parts and supplies we need and will need. Advancing or injecting capital this year to offset these risks could be very beneficial in working through these areas of development risk than just hoping that things correct in due course, especially given how impactful a timely construction of CdO can prove to our future gold production. Most certainly we live in a time where it is best to be proactive than reactive.

In addition to the supply chain, Government/Bureaucratic aspects of business that were certainly impacted by the pandemic are still not back to normal and the recent Omicron surge will likely extend those issues further as backlog from the last shutdowns has in no way been completely resolved, These are all things we need to be prepared for and plan appropriately for going forward but I think this is well we are very well served by a team with so much experience in Mexico.

What are the regulations when it comes to reporting Santana cash flows? Are you allowed to report on revenue and costs if there’s no valid economic study? Or will you have to apply incoming cash flows against capital expenditures in your cash flow statement? We’re not looking to hear when Minera Alamos will declare so-called ‘commercial production’ as that term has been hollowed out over the past few years to just a meaningless arm-wavy term, but at what point will investors be able to look at your income statement and cash flow statement to see how much cash the company is generating?

The reporting standards change upon a declaration of commercial production, which quite honestly is the very least of my concerns right now. As you say it has become more of a promotion level of some companies that have made the declaration clearly prematurely and paid the price for the false expectation of an operation that is sustainable without ample additional injections of equity. I don’t think I need to point to examples as there have been a couple of poster child’s of this in Canada, US and Australia in the last 12 months.

I think it will only be after commercial production we provide some initial guidance on both production and costs but prior to that the impacts of gold sales and also the costs of the mining and processing to achieve those would be clearly within the financial statements. As production continues one would expect the overall cash draw down to level out prior to what I would want to see which if you got granular (and for this we will probably have to present within news releases) a solid period of time of net cash generation that leads to that commercial production announcement.

You were aiming to have a maiden resource estimate out on Santana in ‘early 2022’ on the back of the Phase 3 drill program, are we still on track to accomplish this anytime soon?

Phase 3 drilling has concluded. We await some assays from some last drilling that was done at Nicho before the end of last year – with those remaining holes we can finish the work on the resource statement and that’s important because you could hardly announce commercial production without it as the obvious question would be “Commercial Production? On What?”. So, the work toward that should run in parallel with the operating ramp up so hopefully it wouldn’t be too long after that we are comfortable with a commercial production declaration. It is definitely tough to nail down precise timing with the assay labs but we have had pretty good turnaround in the past so hopefully it doesn’t serve to be a hinderance to timing on release of the initial resource that really is just only iteration 1 focused largely on the Nicho complex.

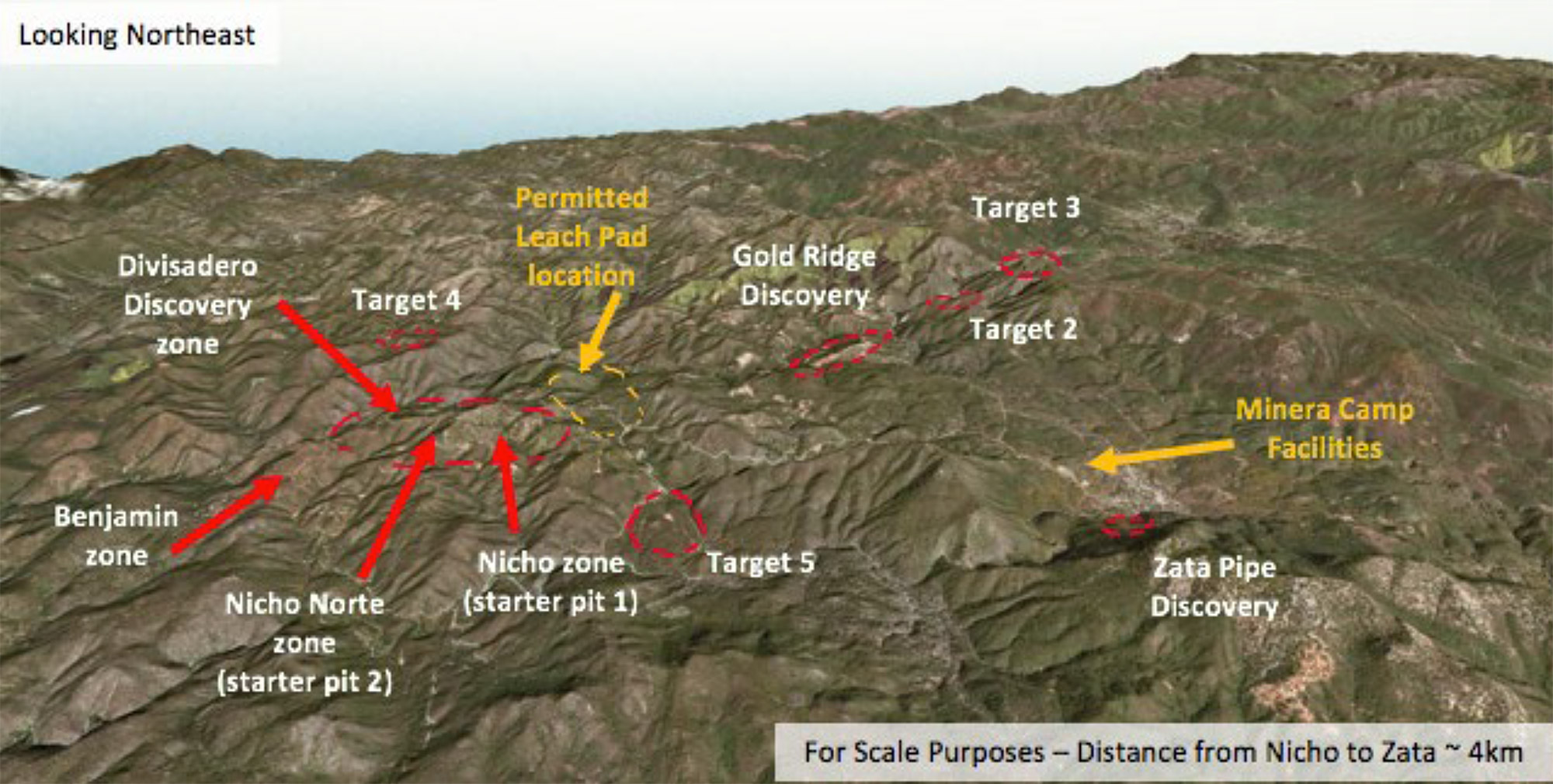

Let’s discuss the exploration approach in the Greater Santana region for a minute. While the attention was originally focusing on the oxide-hosted gold zone, there’s more than meets the eye here at Santana and your recently discovered ‘pipes’ could potentially add a lot of value to Santana. Can you elaborate on the exploration approach here and how this may impact your plans moving forward? Are the upper layers of these pipes also oxidized and amenable for heap leaching or will a different approach be necessary?

Absolutely! When we look at a project it needs to meet 3 criteria or we don’t have interest. Firstly, a starting resource in the +/- 400koz gold range; secondly, can we build it as is and where it is in a low capital intensity manner; and thirdly and perhaps most importantly, if we do build it do we see how it can become a bigger operation from reinvesting cashflows to expand the resources and thereafter scale up the production profile.

Santana is no exception in this regard and that geological visibility of upside resources comes in the form of the cluster of gold bearing breccia pipes we have identified at Santana. While all the historical drilling has largely focused on the Nicho and Nicho Norte pipe, we have a half dozen other pipes all within a few kilometers. Some as large as Nicho or potentially larger and others smaller. What we know is they are all gold bearing and were all emplaced the same way. Surface sampling demonstrates grades indicative of those we see at surface at Nicho. With the mine up and running, which ultimately was our focus during the pandemic, we can begin to prioritize which of those other pipes will see definition drilling and allow us to establish new 43-101 resources beyond the initial Nicho development. This will likely start with a few holes in each to confirm the grades we are seeing at surface and to get a rudimentary sense of the volumetrics of each. In terms of their leachability, there is nothing that would suggest any surprises that would differ from the treatment of Nicho’s mineralized material.

We’d also like to go back to 2018 when you announced assay results from the Divisadero discovery where hole 18-121 encountered almost 96 meters of 0.85 g/t gold, 9.8 g/t silver and 0.33% copper. With copper trading over $4/pound, is Divisadero a prospect you’ll revisit sooner rather than later? And how does this fit into the greater scheme of things at Santana?

Divisadero definitely needs some follow up and could well be the first in line of the other targets to see additional drilling but less for its copper and more the gold.

Minera actually has a genuine copper project just to the north and adjacent to the Santana claims – it underwent economic studies back 8-10 years ago and yet we barely give it a mention in the MD&A – however, the lack of us talking about it doesn’t reflect our goals to monetarize it in one form or another for the benefit of Minera shareholders as a copper development project doesn’t belong in a gold producer.

The other projects

Let’s tackle Cerro de Oro first as this is the second domino in your corporate strategy. You originally anticipated a very straightforward permitting process. Are you still feeling confident in a smooth and fast process? It’s starting to sound some Mexican regions are becoming a bit tougher but Zacatecas obviously has a long history of mining and could be seen as one of the better states to work in.

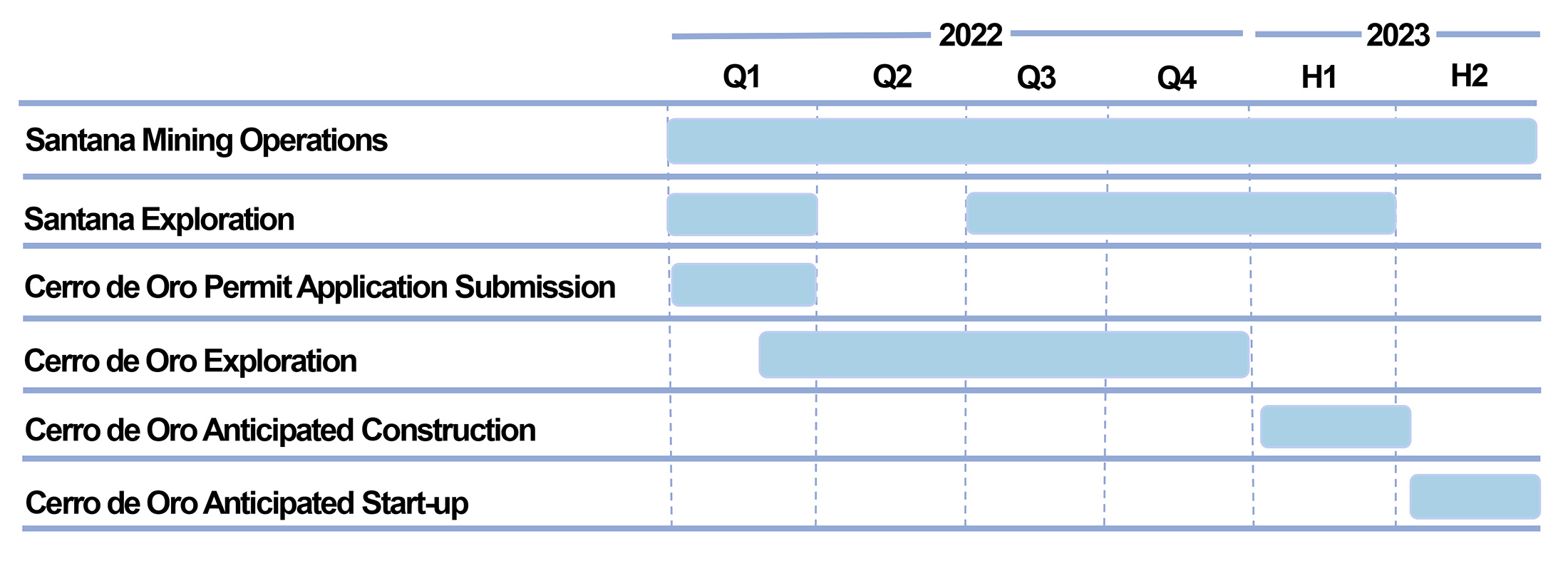

Cerro de Oro’s news flow has been bottlenecked not really by permitting as it hasn’t entered permitting yet. The surface rights agreements were largely done last summer but not entirely and I appreciate our team’s approach to do things right than rush again for market expediency. Trust me I would have loved the dual track news flow last year but we are pretty close on everything and the permit applications are ready for submission shortly after we finalize the last of the surface rights. As for the time after that to permit we hope to be able to make a construction decision in Q1 of 2023 and the mine could come on stream later in H2 2023.

What’s your estimated capital intensity and initial capex at Cerro de Oro? Have you recently had to revise some of your expectations due to inflationary pressure or is a heap leach project like CdO relatively ‘shielded’ from that? Will there be external capital required to build Cerro de Oro or do you expect the 2022-2023 cash flow from Santana in combination with your existing cash position and marketable securities to be sufficient?

We really haven’t experienced too much in the way of cost inflation so far. I believe our cyanide prices have risen a bit but we really have such a low cost base to build these mines that they certainly aren’t at risk of significant cost overruns as a result of the inflationary pressures we are all witnessing in the global economy right now. The cost structure in Mexico is very favourable for us given 65-70% of our operating costs are in Pesos too.

CdO will be a bigger operation out of the gate than say Santana, perhaps 60,000-70,000 oz/y and scaling pretty rapidly beyond that. As such everything is on a bigger scale, carbon plant, pads etc. Given we also intend to build an ADR for CdO that would take both the loaded carbon from Santana and CdO I would estimate capex to be in the US$25 million range – likely funded by a modest debt package supported by cashflows from Santana.

Does the company already have some sort of blueprint for the Santana Expansion plans or are you waiting for the NI43-101 compliant resource estimate before finalizing those plans? How fast would you be able to switch gears and develop the Santana Expansion instead of Cerro de Oro?

The way we see CdO as a project is it will likely see a more rapid growth in its resource base and production profile. I think Santana, with its discrete pipes that could lead to multiple pits perhaps serving a central pad, will be a slow and steady growth that will be led much more by the drill bit that CdO.

You have a third interesting project in your asset base, La Fortuna. Are you planning on doing any work there in the near future, like expanding the resource to further extend the current 5 year mine life. Applying a $1625/oz gold price would result on an after-tax NPV of US$115M (almost C$150M) compared to the US$70M base case factor using the 2018 PEA so this really is a good project at the current gold price as the after-tax IRR will exceed 100% even if one would factor in capex inflation.

If Fortuna has one issue it’s that the PEA was based off a high-grade starter pit with a modest 5-year life – the economics are so good it still provides an excellent case for its development and sits there with permits in place. However, we know there are both brown fields extensions to the pit resources to drill as well as surrounding greenfields exploration that we have drill programs planned for in due course. I think it makes sense to deploy cashflows from the first mines to properly drill off more mine life at Fortuna and perhaps even more so we can consider the proper utilization of our mill which is rated at 2,000 tpd against a base case PEA that uses 1,100 tpd. Imagine a project with a 7-8 mine life perhaps at closer to that mill capacity with may be a slightly low grade. It will be an even more impressive mine that starting it up on the 5 year pit. That said I will look forward to it contributing those lower cost ounces indicated within the 2018 PEA.

Are you still looking to add more assets to the company? Has it become more difficult to find decent projects at a decent price now gold is trading at and above $1800/oz? Is Minera’s core focus still purely on Mexican assets?

We are always looking both in Mexico and elsewhere, however, I think we have a lot to focus on for the next 6 months so the 4th asset we talk about is, in my opinion, some way off. In the meantime, we will continue desk due diligence on opportunities that may fit our business plans.

Minera Alamos as a company

How do you see the business climate and more specifically the attitude towards mining evolve in Mexico? Do you notice any difference in doing business in Mexico compared to, say, three years ago?

Things are tougher and I think some of that is changes in the government although you could argue some stuff has just become harder as a result of bureaucratic delays due to Covid. I think it will be easier to tell a year from now whether with things hopefully normalizing is it a Covid influenced effect or a result of changes at Federal and State levels in recent years. We remain very comfortable operating in Mexico and while, like any country, it has its drawbacks we believe the cost structure, geology and rapid permitting more than make up for some of the harder aspects of operating in Mexico.

The acquisition of the option to acquire Los Reyes and subsequently selling that option to Prime Mining was a brilliant move as you have been able to consistently monetize bits and pieces of your Prime Mining stock at a much higher price than the deemed value upon receipt. According to you recent financial results you still have about 590,000 shares in Prime Mining. Do you have a strategy to monetize these last few shares?

I have always believed that mining companies shouldn’t be investment holders if those equity holdings could be monetarized to advance the development of assets under control. That is why we have sold blocks of our position all the way up – the last being 1 million shares at C$4 a share last year. In due course we would probably be saying a fond farewell to what has proven to be an excellent source of capital for our activities.

You currently have 446 million shares outstanding and although you have reached a market capitalization north of C$200M you technically still are a penny stock. Do you notice this is still making people reluctant to invest in the company or is that ‘prejudice’ mostly gone now?

I think there is always that perception and its one I’d love to resolve but I think any kind of share restructuring needs to be done around something and we aren’t at that point yet. That said when done correctly, it can be very beneficial as in the case of Aya Silver, Endeavour Mining and Victoria Gold.

Conclusion

2022 will be a pivotal year for Minera Alamos as the company will join the ranks of gold producers. While the initial gold production from Santana won’t be spectacular, it will provide the capital necessary to get the ball rolling and start the development of the Cerro de Oro gold project. According to President Ramshaw, there still is plenty of exploration upside on all three projects in the asset portfolio and the incoming cash flow from the Santana gold mine will kickstart the exploration and development scenarios on all other projects.

The proof of the pudding is in the eating. And we’ll know so much more by the end of this year.

Disclosure: The author has a long position in Minera Alamos. Minera Alamos is not a sponsor of the website. Please read our disclaimer.