Strike Resources (SRK.AX) has completed an A$5M capital raise which will boost its anticipated iron ore output from the Apurimac iron ore project in Peru from 125,000 tonnes per year to 250,000 tonnes per year. The first batch of 30,000 tonnes of iron ore should be loaded on a ship this month, and that would be right in time to take advantage of the current spot price which is exceeding US$200/t for a 62% Fe product (although there are lots of details that may impact this pricing level, while the shipping rates for bulk cargo are quite high these days).

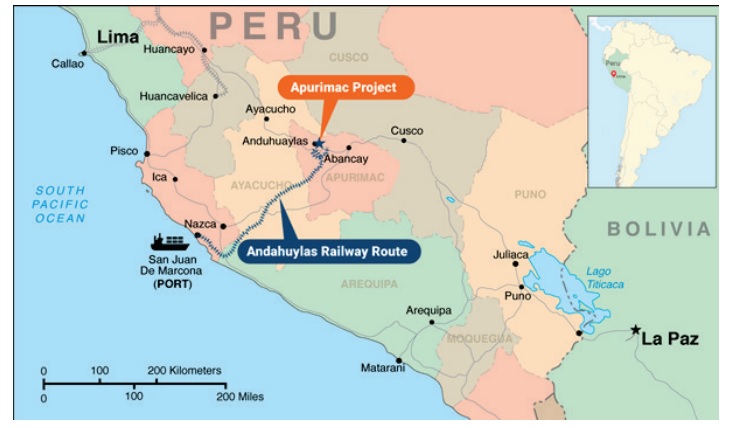

The Apurimac DSO product has an average grade of 65% which fetches a premium price compared to the benchmark pricing level, and that will likely compensate for the higher shipping expenses. If the iron ore price doesn’t completely collapse in the next few months (during the voyage), Strike Resources has a good shot at receiving a net price of $200/t (including shipping expenses), which would result in a net margin of about 60% considering Strike is guiding for an FOB operating cost of $70-80/t. That’s relatively high but that is also related to the sub-optimal shipping route as the company is trucking the iron ore from the project to the Port of Pisco using a 50-80 truck fleet.

While the focus currently is on the DSO operations to get some cash flow, the more extensive economic studies on the Apurimac project will likely also be revisited. About a decade ago, the company was planning to develop the project as a 15-20 million tonne per year operation producing an iron ore product with a 68% Fe content (resulting in an anticipated premium of about $20-35/t over the benchmark price level) from an existing resource of almost 270 million tonnes at an average grade of 57.3% Fe. The incoming cash flow from the DSO sales will for sure help Strike to revisit the full production scenario.

Disclosure: The author has no position in Strike Resources, but is watching with interest. Please read our disclaimer.