Since we published our first full report on Falco Resources (FPC.V) less than a year ago, the company’s share price has increased by approximately 150%. A lot has happened in the past 12 months as Falco released a Preliminary Economic Assessment on the Horne 5 property confirming the economics of the project.

Falco was also able to take advantage of its strong share price as the company raised in excess of C$45M which puts Falco in an excellent position to complete the feasibility study and the permitting process to restore the Horne 5 mine in all its glory.

A lot has changed since the PEA was published

Falco Resources published a Preliminary Economic Assessment on its Horne 5 project in May of last year. The study confirmed the potential of Horne 5 as a poly-metallic underground mine with a total production of 2.9 million ounces of gold, 800 million pounds of zinc, almost 200 million pounds of copper and just short of 25 million ounces of silver.

We were attracted by the variety of metals that would be produced at Horne 5, as the impact of a weaker precious metals environment could be compensated by higher base metal prices and vice versa. The initial capex of C$905M sounded quite steep, but let’s not forget Osisko Gold Royalties (OR.TO, OR) has a vested interest in making sure Falco Resources succeeds. We have no doubt Osisko will play an important role in the financing mix to build the mine.

On an after-tax basis, the NPV5% of Horne 5 was estimated at C$667M using a gold price of US$1250/oz. That was a good start, but a PEA is per definition indeed ‘preliminary’ in nature.

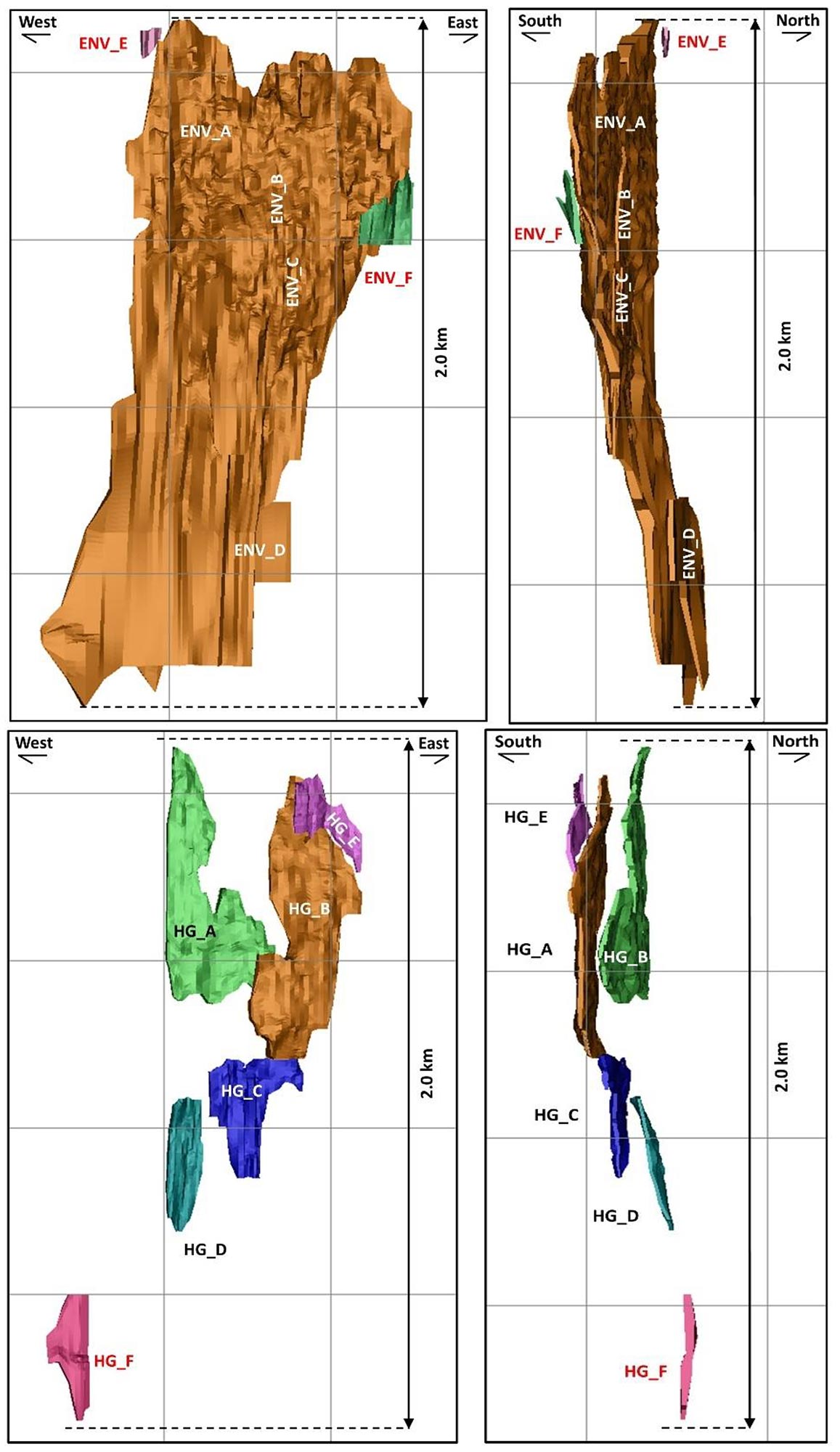

Just a few months after filing the technical report on Horne 5, Falco released a very important resource update. Whereas the PEA was based on a total resource estimate of exactly 71 million tonnes, Falco’s most recent resource estimate increased the tonnage to 91 million tonnes in the measured and indicated categories, and 113 million tonnes in all categories. The average grade is a bit lower, but the weaker Canadian Dollar and longer mine life will compensate for the impact of a lower grade.

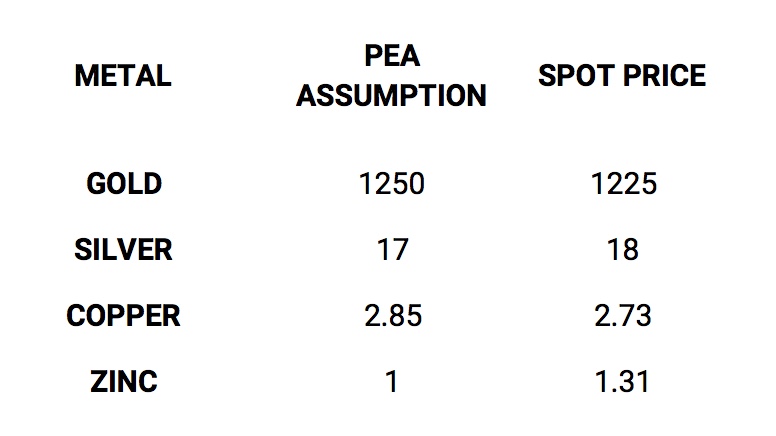

But there’s more. Whilst a copper price of $2.85 per pound was quite optimistic in May 2016, that specific price is now definitely within reach. On top of that, the other commodity prices have also increased as well:

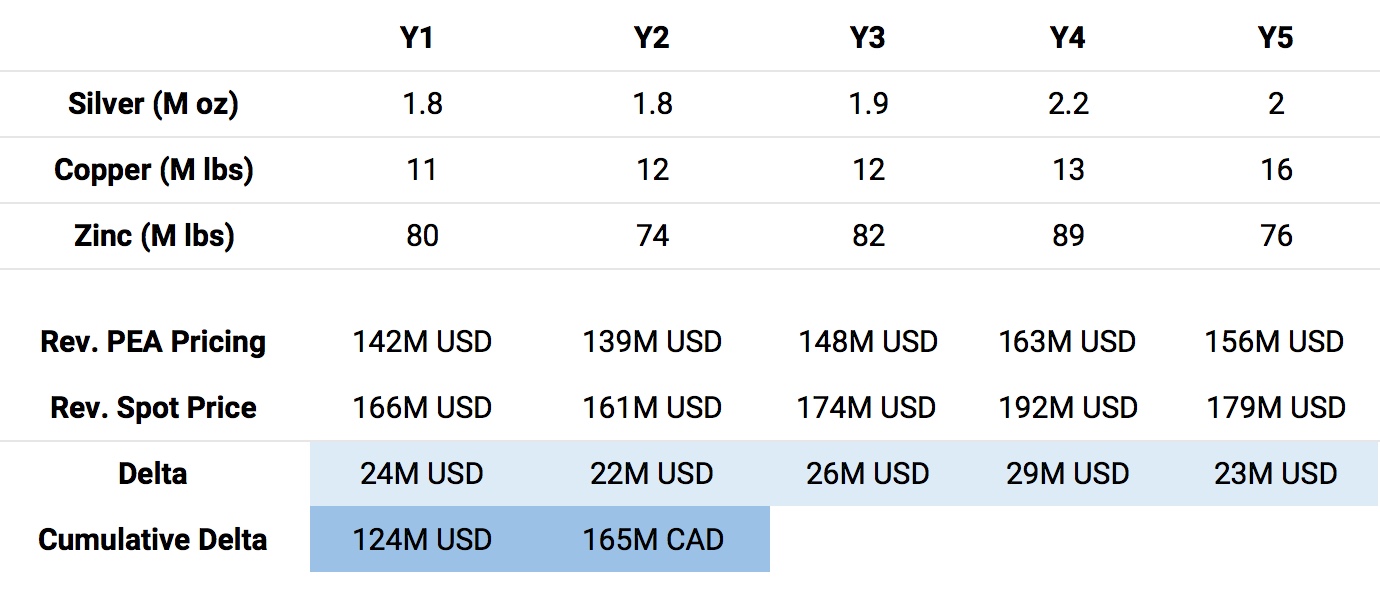

That’s great news, and the impact of the higher silver and zinc price becomes immediately obvious when you look at the (payable!) production mix in the first five years of the mine life (according to the PEA).

{kind=link}

Thanks to the current high zinc price, the total revenue in the first five years of the mine life (based on the mine plan in the PEA, which will undoubtedly be updated in the upcoming feasibility study) will increase by C$165M. Keep in mind that’s just a rough back of the envelope calculation and doesn’t take any discount rate or taxation into account, but it’s obvious the current zinc price will have an important impact on the economics of Horne 5.

2017 will be an important year for Falco Resources

Falco’s consultants are currently finalizing the feasibility study on Horne 5 and whilst Falco considered the PEA results to be excellent (and reliable), the company is obviously also considering alternative development scenarios. Not only did the total tonnage of the resource estimate increase, the (much) higher zinc price could allow Falco to see if more higher grade zinc zones could be brought forward in the mine life as this will have a positive impact on the NPV and payback periods.

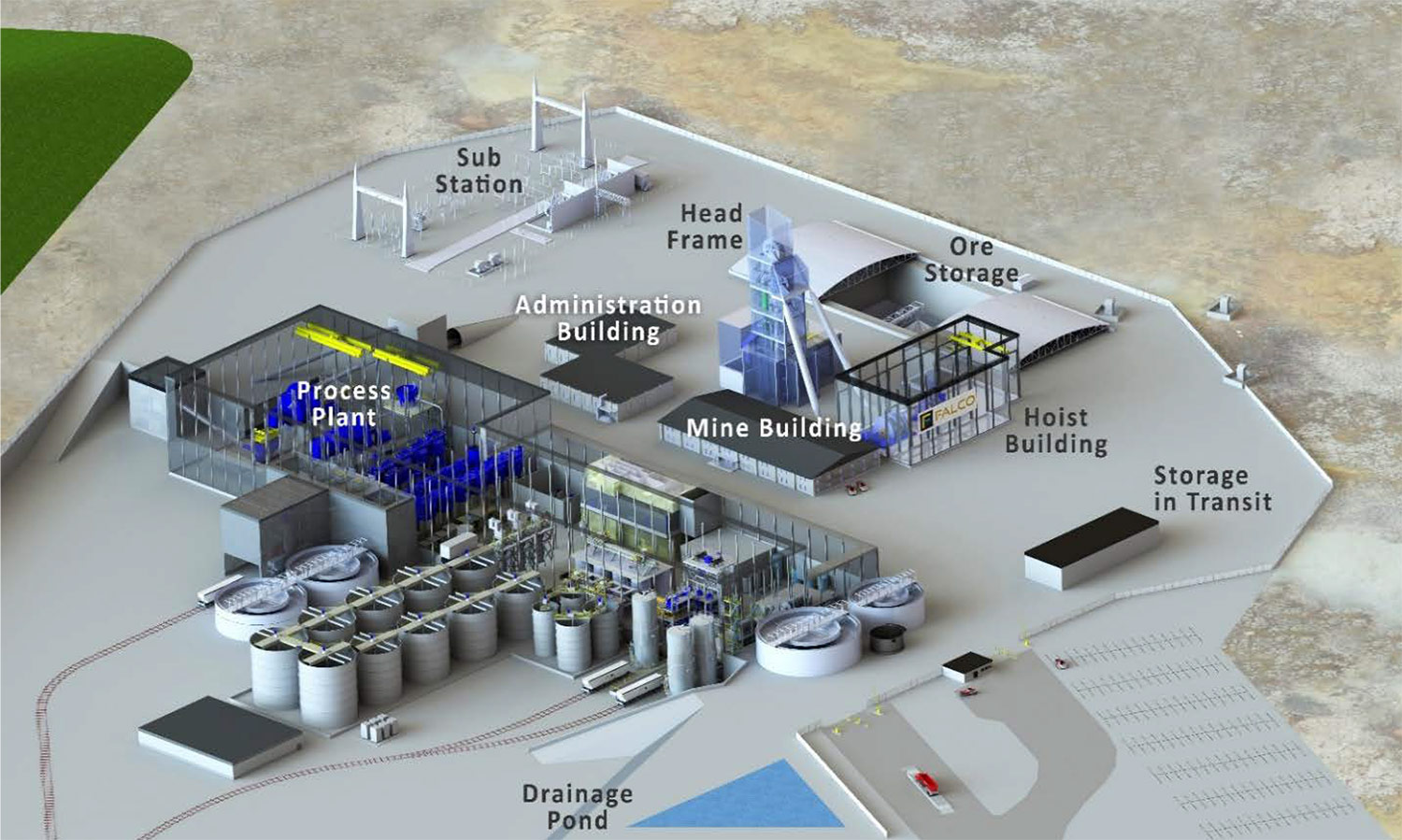

As Glencore (GLEN.L) elected not to exercise its back-in right on Horne 5, Falco has now retained full ownership of the Horne 5 mine which should simplify things, going forward. Glencore does retain a 2% Net Smelter Royalty and has a Right of First Refusal to purchase or toll process anything that comes out of the Horne 5 mine.

Not only will the feasibility study be a very important milestone, we also expect the company to start dewatering the Quémont shaft number two. Falco has received all permits to start dewatering the shaft up to a depth of 100 meters, and should initiate this process within the next few weeks. The company will need to ‘neutralize’ the water to reach a pH-neutral level but this shouldn’t be too difficult at all.

With the feasibility study in hand, Falco Resources will also be able to put its financing mix together for the construction phase. The ‘deadline’ to negotiate a potential streaming deal with Osisko Gold Royalties expires at the end of November, so we would expect both parties to work towards a mutually beneficial agreement to hit the ground running. This would keep the company on track to indeed start producing gold at Horne 5 in 2020/2021.

Three short questions for Vincent Metcalfe, CFO of Falco Resources

At the end of September, Falco had a working capital deficit of approximately C$7M. Subsequent to the end of that quarter, you were able to raise almost C$45M (net) in two different private placements after seeing a strong interest from shareholders to support Horne 5 moving forward. What’s your current cash position, and will this be sufficient to cover all expenses until a construction decision will be made?

Sure, we now have approximately C$42M (with a big endorsement from the Québec government which recently invested an additional C$10M) in cash and this should definitely be sufficient to allow us to complete the feasibility study and the Environmental Impact Assessment. We are also planning to start preparing the mine site which should allow us to really hit the ground running once the construction decision will be made.

We will also be spending approximately C$10M in exploration expenditures as we just announced we are planning to drill in excess of 40,000 meters this year to add value to the project and the company as a whole.

Could you elaborate a bit on Falco’s plans for 2017? What will be the milestone achievements and decisions?

As mentioned before, we will be completing the feasibility study before the summer, and that’s also when we would like to complete our EIA. The C$10M we are planning to spend in 2017 will be spent on a 10,000 meter drill program at Horne 5, but we will also continue to explore our larger land package. We anticipate to complete 30,000 meters of drilling outside of Horne 5 as well.

The metal prices are moving in the right direction and in just a few months, even the copper price is almost at the $2.85/lb used in the PEA whilst zinc is now trading much higher. You will be announcing the results of your feasibility study in the next few months, will there be any additional changes compared to the PEA, specifically in the mine plan (changes in the mining sequence) or anticipated recoveries and potential cost savings?

Yes, there will be some changes, and the most important update will probably be the increase of the stope sizes. As you might remember, in the PEA we were including 15x15x38 meter stopes, but the size of the stopes will now be increased to 25x20x38 meters which more than doubles the stope size from 8,500 m³ to 19,000 m³. This will probably allow us to reduce the mining cost per tonne.

On top of that, we are planning to modify the hoist and use a more efficient hybrid friction hoist. This could reduce the required horsepower of the hoisting engine by 20-30%, which should reduce the power consumption rate.

And finally, we wouldn’t be surprised to see a higher average recovery rate for the gold. In the original PEA, the payable gold recovery was estimated at 86.8%, and every 1% increase would allow us to add an additional 2,500 ounces of gold per year to our production mix.

Conclusion

2016 was a turnaround year for Falco Resources as the PEA confirmed Horne 5 is viable, whilst a subsequent resource update shows there’s additional upside potential at Horne 5 (completely ignoring the regional exploration potential).

2017 will be the year of the ‘finishing touch’ with the completion of the feasibility as main milestone. Given the desire from senior producers to fall back on the ‘safer’ North American projects, we do think the Horne 5 mine will attract some attention as for instance Silver Standard Resources and Gold Fields have submitted a joint bid for Kirkland Lake Gold in 2016. This could mean the M&A market is still in full swing and especially Gold Fields seems to be keen to acquire properties in safe first-tier mining jurisdictions.

Disclosure: Falco Resources is a sponsor of the website. We have a long position.