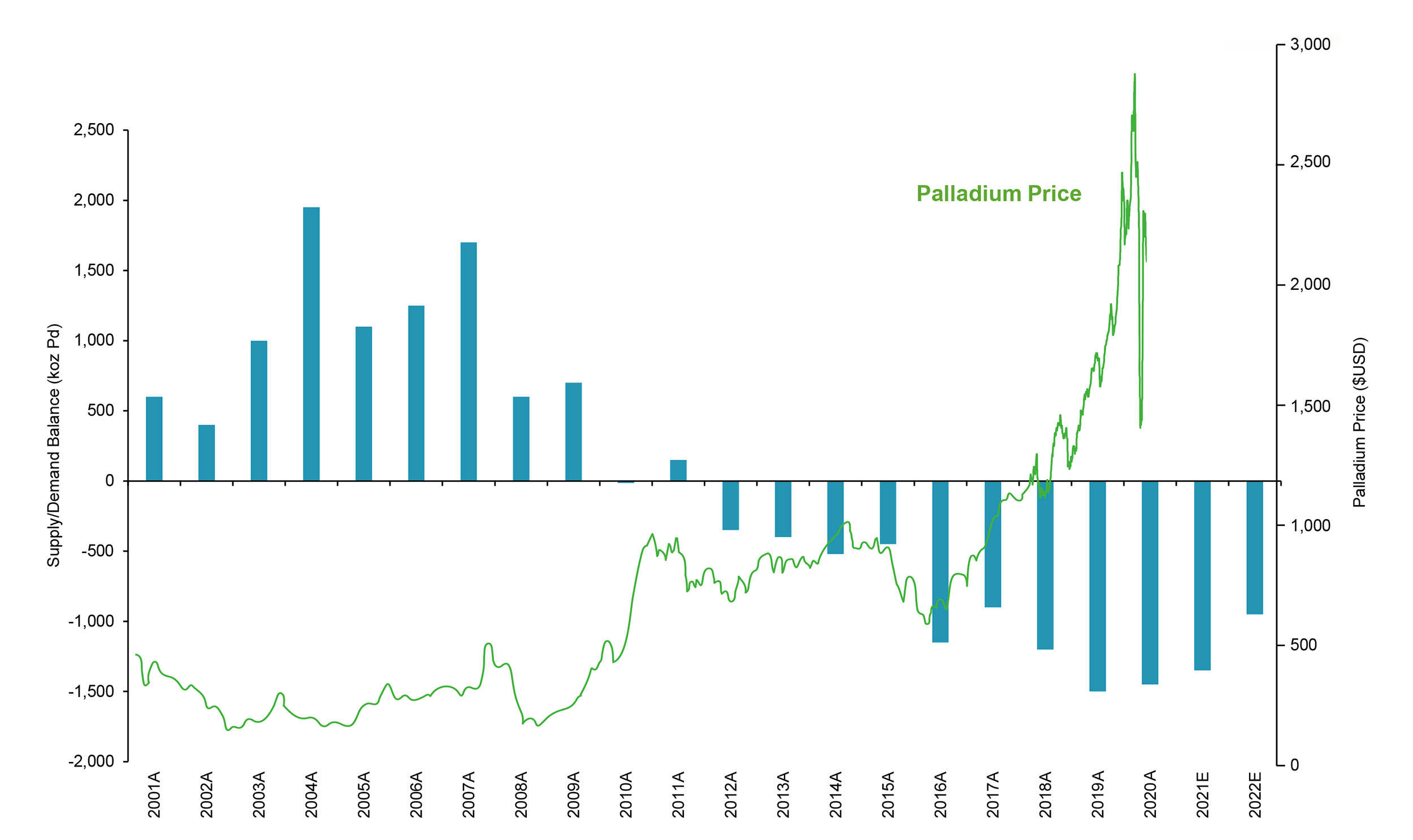

Less than six months ago, companies were stumbling over each other to acquire and drill PGM projects as the Palladium-price soared to in excess of $2000/oz. Pretty much every company which previously encountered some palladium dust in its samples was re-branded as a palladium story as that made it easier to secure funding. Some of those companies will succeed, others will fail.

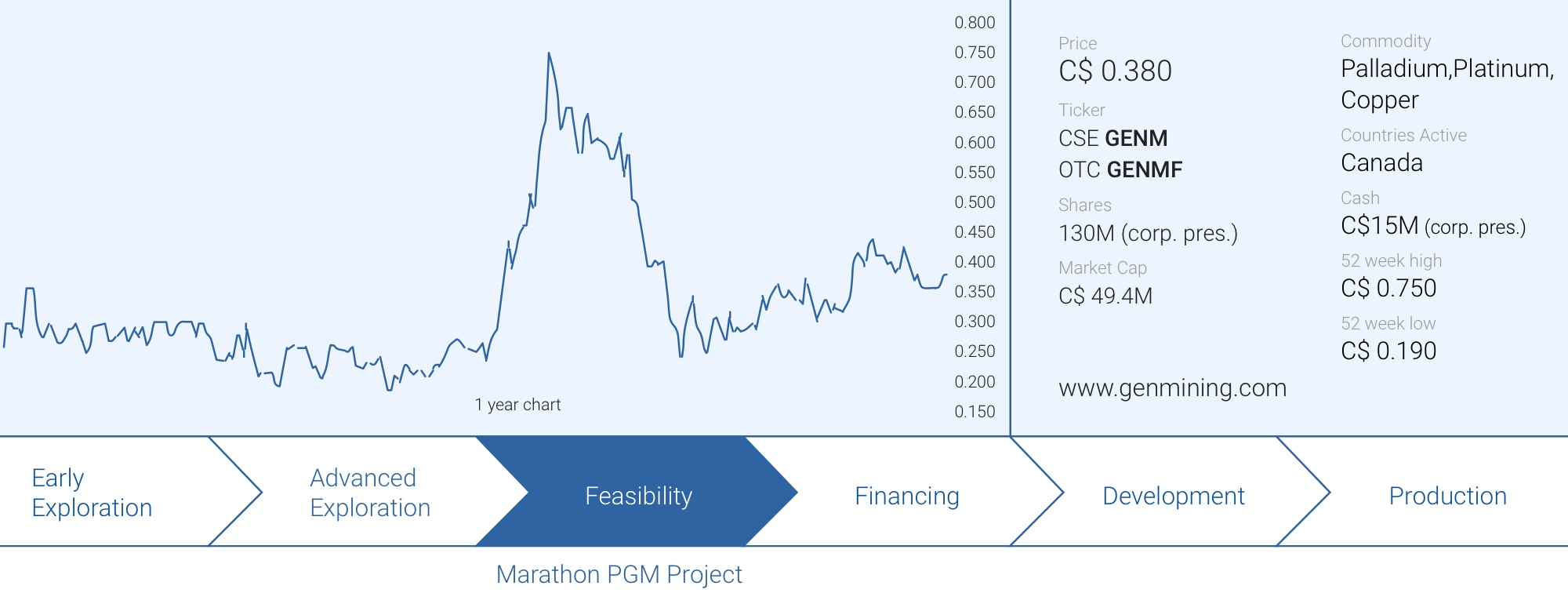

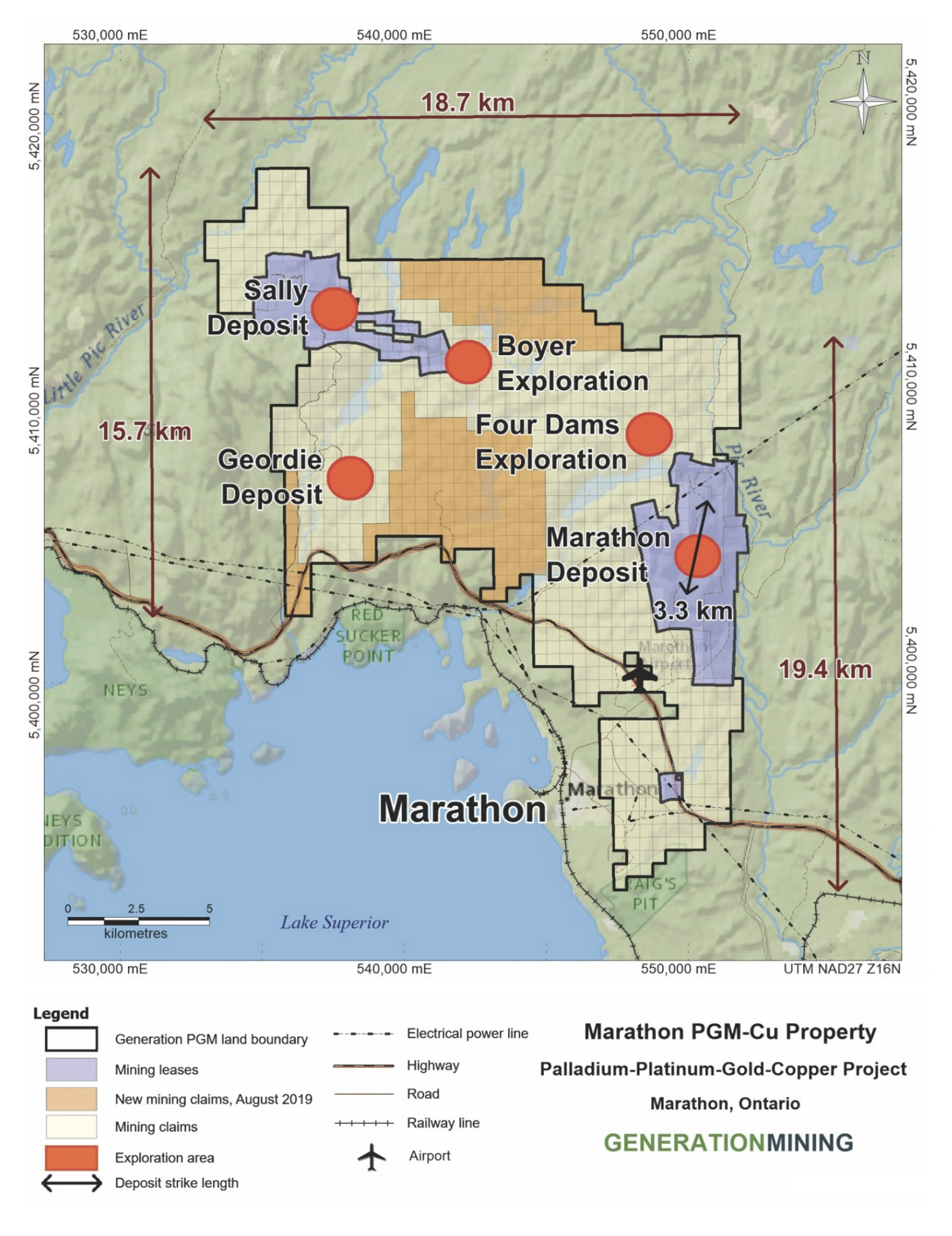

Generation Mining (GENM.C) was an early mover as it secured the majority ownership of the Marathon PGM deposit in Ontario about a year ago. Given the current palladium price and how the deposit is shaping up with a recently completed PEA as crown jewel, this acquisition may enter the history books as one of CEO Levy’s best deals ever. Unfortunately, Generation Mining has also been sold off along with the other palladium companies although the base case scenario of its PEA uses a palladium price that’s substantially lower than what the metal is trading at now.

At the current Palladium price, Marathon remains hugely profitable

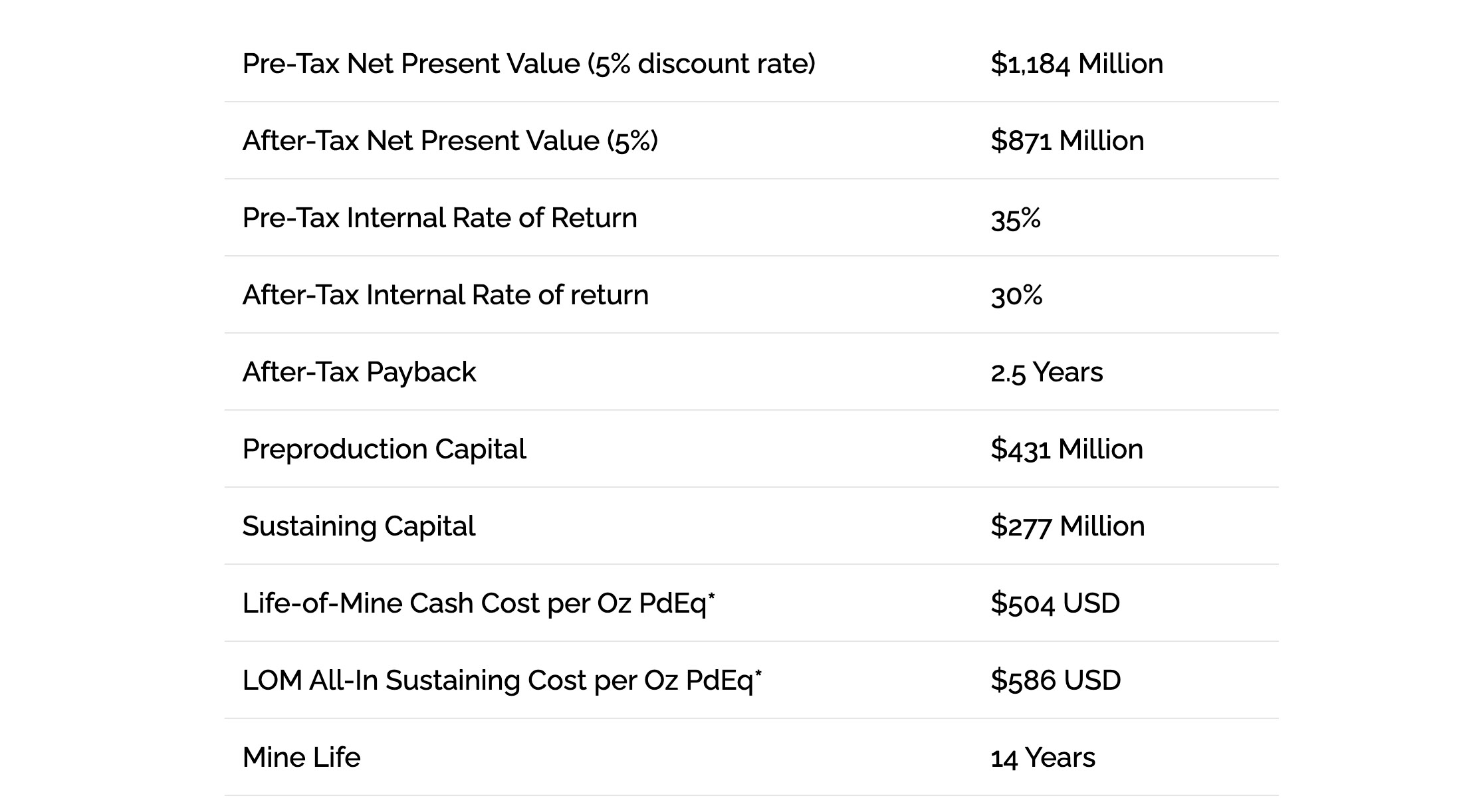

The January 2020 PEA intended to figure out the economics of the Marathon PGM project using reasonable commodity prices. A successful exercise as the base case scenario using $1275 palladium confirmed the economics of Marathon as the after-tax IRR came in at 30% while the NPV5% of C$871M (again on an after-tax basis) shows how important the low-cost nature of the operations will be: the all-in sustaining cost per ounce of palladium-equivalent is estimated to be less than US$600, or less than a third of the current palladium price and less than half the base case price used in the PEA.

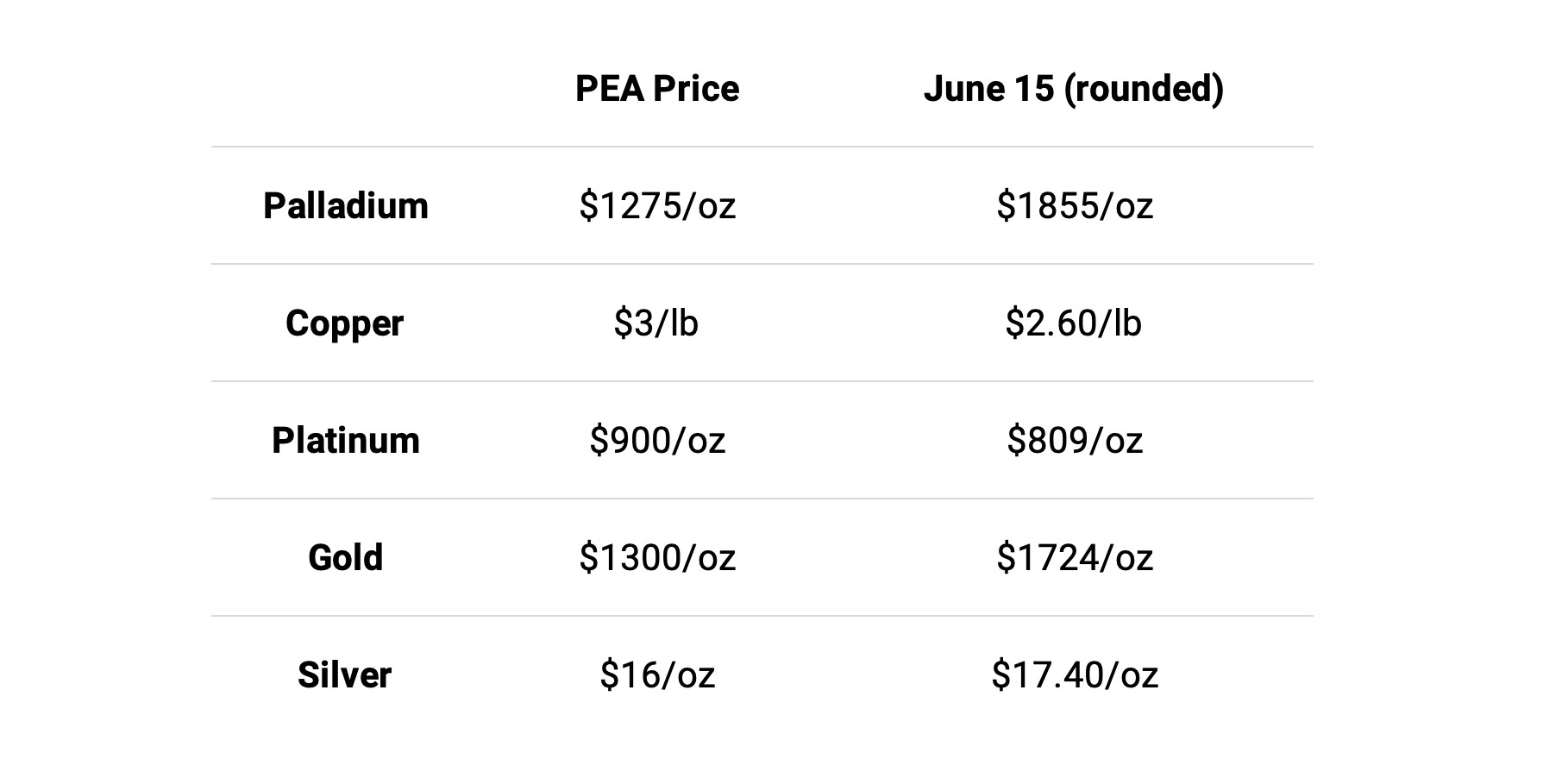

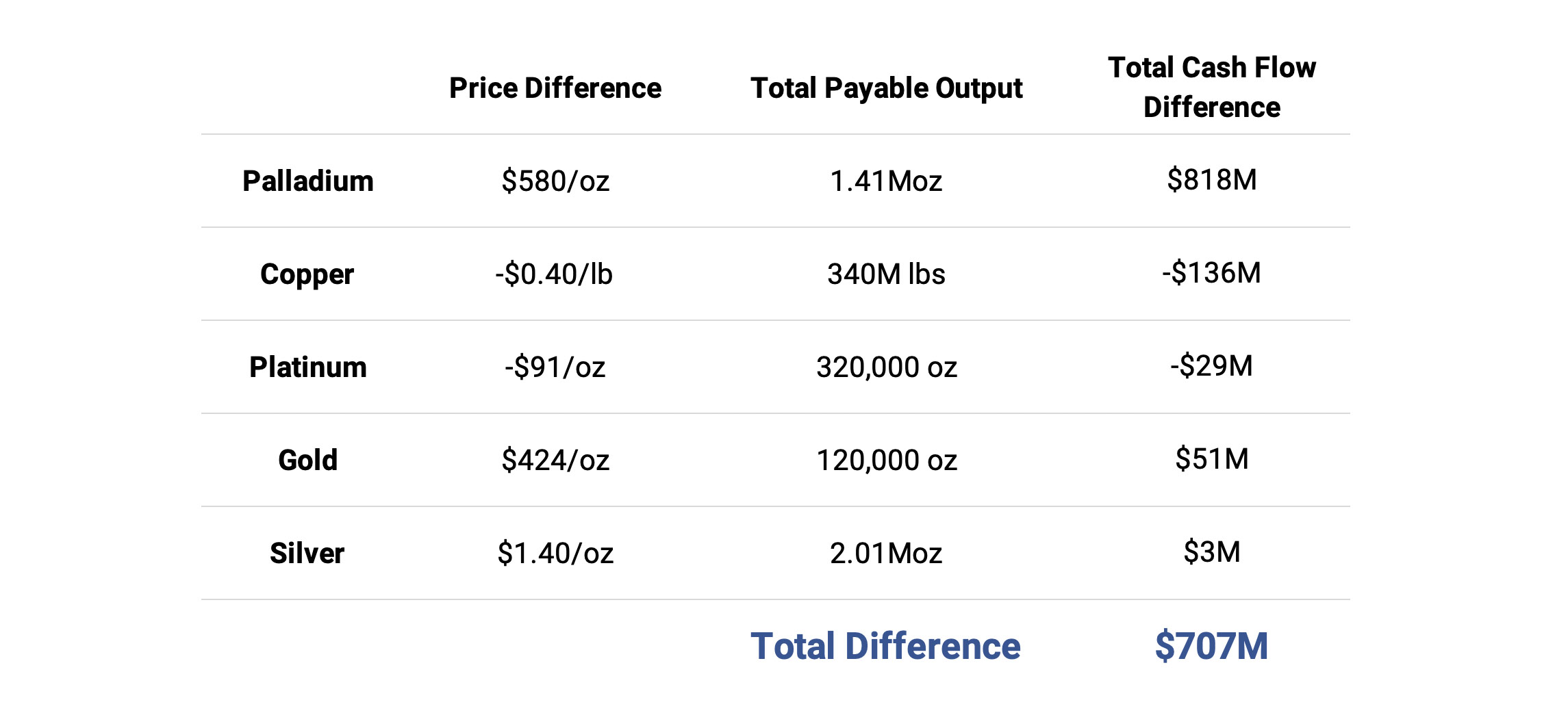

And just to make the comparison easier and to explain the impact the current metal prices have on the economics, the following table compares the metal prices used in the Preliminary Economic Assessment with the metal prices halfway June.

Platinum and Copper are trading about 10% lower than the price used in the PEA, but these are just by-products and the slightly lower price will have very little impact in the greater scheme of things. But to show how important the higher palladium price is, we have put a table together to show the impact of the difference in metal prices on the product mix. Important side-note: we obviously look at the payable metal output and not the total resource nor the amount of metals produced (as the payability ratio is less than 100%).

So applying the current metal prices would boost the cash flow of the project by US$707M, or almost C$1B. Keep in mind this is just a rough back of the envelope calculation. Additionally, the cash flow difference was calculated on a pre-tax and undiscounted basis. Adding in taxes and a 5% discount rate will likely reduce the impact on the NPV by more than 50% compared to the US$707M quoted above.

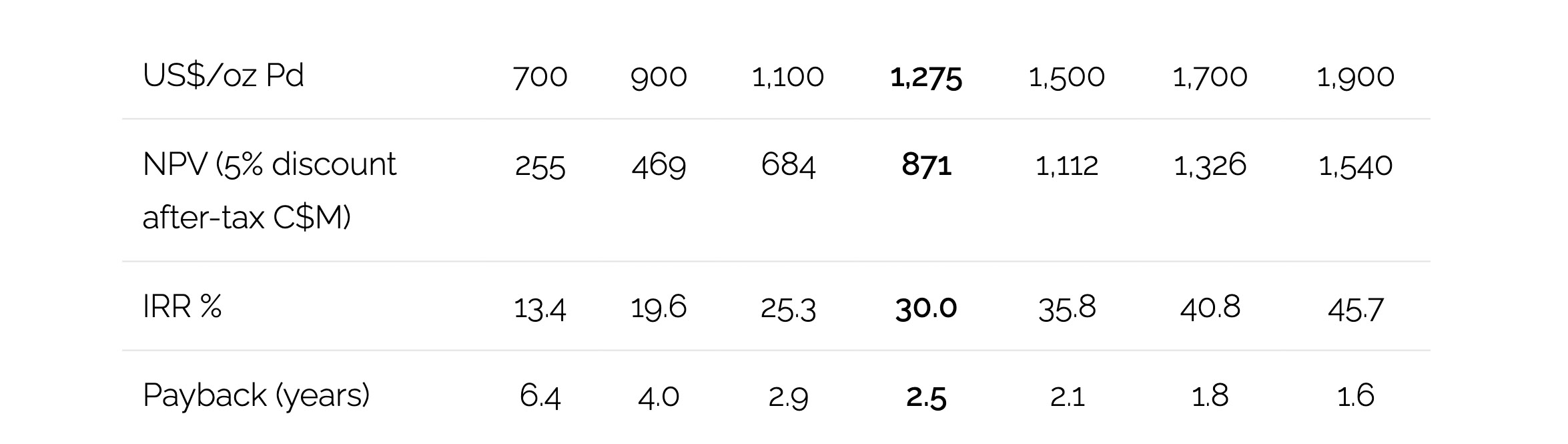

As palladium is by far the most important metal in the production mix, Generation’s sensitivity table also provides interesting details.

Keeping all commodity prices but the palladium price unchanged shows an after-tax NPV5% of C$1.33B based on a palladium price of $1700/oz, about 10% below the current price.

Sibanye’s claw-back right explained

There still appears to be some confusion as to how the Sibanye-Stillwater (SBSW) earn-back agreement works. Generation Mining remains on track to obtain its 80% stake in the project by the end of this year, and Sibanye has a one-time right to repurchase a 31% stake where after a 51/49 joint venture will be formed where Generation Mining becomes a minority partner. This one-time-right remains open for a period of 90 days starting on the day a production decision will be made (likely in H1 2021 upon the completion of a feasibility study).

To earn back the 31%, Sibanye will have to cover 31% of the capex whereafter it will obviously still have to contribute its 51% stake in the remaining capex. The capex in the PEA was estimated at C$431M, and 31% of this is C$134M. This means Sibanye will have to cover the first C$134M AND 51% of the subsequent C$297M (C$151M).

This means Generation Mining will only have to contribute C$146M of the C$431M capex (34% of the total capex) for 49% of the economic rights. This also allows us to re-calculate the attributable NAV in case Sibanye decides to execute the claw-back clause. In the base case with the C$871M NPV, the discounted sum of the cash flows is C$1.3B (you need to add the initial capex back the equation to figure out the total net cash flows). Generation Mining’s attributable share of the cash flows will be C$638M. However, Generation will only be required to fund C$146M of the capex which means the attributable NPV of the Marathon project will be C$492M for its 49% stake.

If we would look at the C$1.33B NPV in the $1700/oz palladium scenario, we can just add back the C$431M to end up at a total cash flow of C$1.76B of which C$862M is attributable to Generation Mining. Deducting the C$146M capex requirement results in an attributable NAV of C$716M to Generation Mining.

Of course, the aforementioned calculations only make sense if Sibanye effectively decides to increase its stake again to 51%. But it shows how strongly the agreement is in Generation’s favor.

The next steps for Generation Mining

Generation Mining is about to kick off the full feasibility study (which should be completed in Q1 2021, but let’s assume there will be delays and aiming for the first semester may be more realistic) and we have the impression newly appointed COO Drew Anwyll is very much applying a hands-on approach and the feasibility study may look nothing like the Preliminary Economic Assessment.

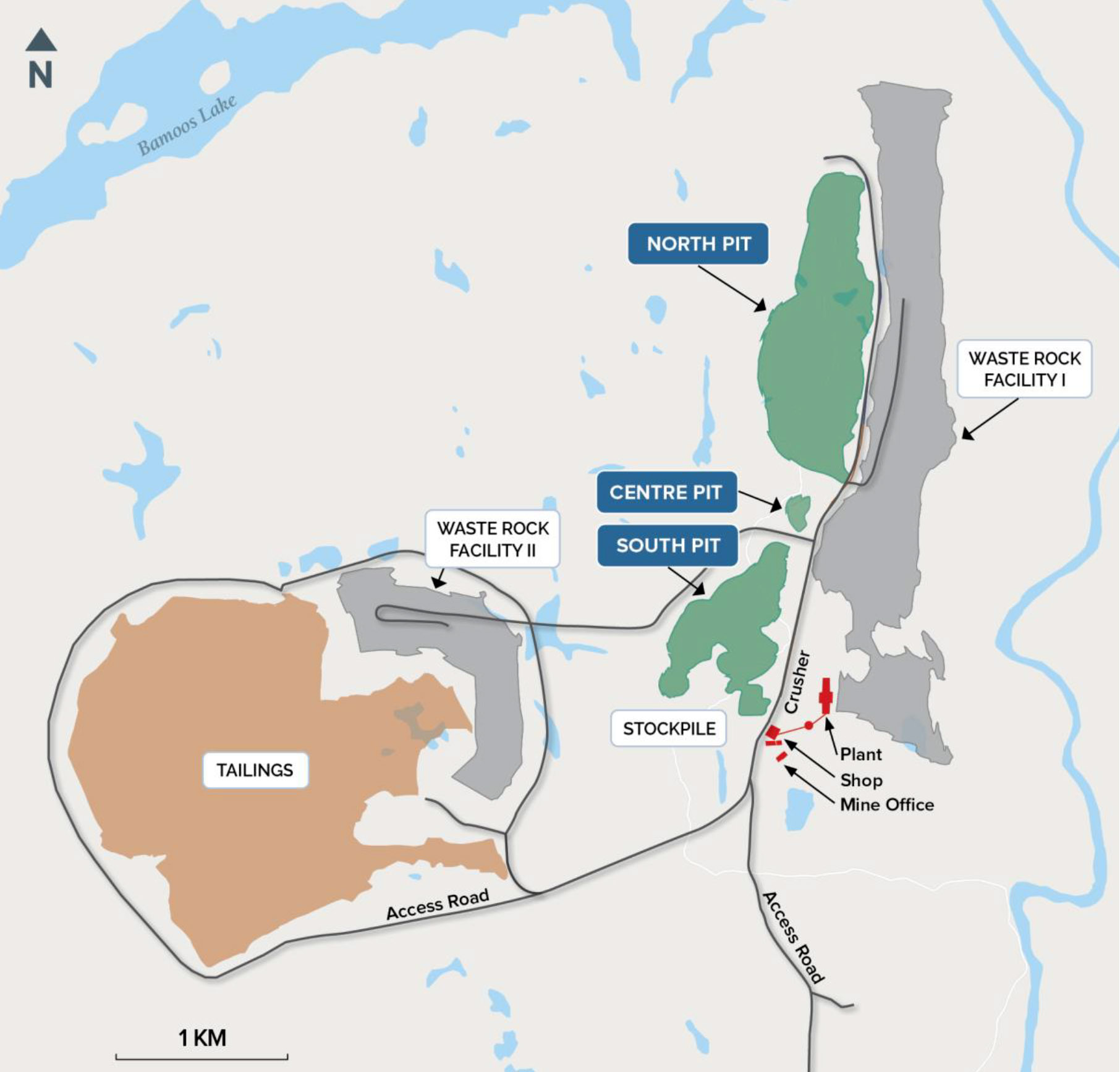

First of all, the consistently higher palladium price will allow Generation to reduce the cutoff grade and increase the number of tonnes in the conceptual pit area. This could result in having one large open pit rather than three separate pits. This creates an additional hurdle as Generation Mining is restarting the permitting process where the previous operator suspended the permitting activities about 7-8 years ago and as a lot of work has already been done, Generation Mining has to make sure it doesn’t make any critical changes to the mine plan which would require the company to submit an entirely new application.

That means the Geordie pit (13.85Mt indicated, 6.6Mt inferred at C$25/t cutoff) and the Sally pit (9.9Mt indicated and 1.3Mt inferred at a similar cutoff) will be excluded from the mine plan. Although the grades are decent, it makes no sense to jeopardize the ongoing permitting process for just a few dozen additional tonnes.

The additional consequence of rethinking the mine plan is that – also thanks to the higher palladium price – the three separate pits could now be combined into one large pit. As Generation Mining doesn’t want to mess around with the planned tailings facility (as it doesn’t want to restart the permitting process), the option to use the smaller southern pit for backfill is on the table.

As more rock will move from the waste category to ‘ore’ category (to be confirmed in the feasibility study), the mine life will very likely exceed the currently anticipated 14 years. Additionally, Generation Mining will very likely have to consider increasing the throughput of the plant. This will increase the capex to C$500-600M but should unlock additional economies of scale.

Conclusion

Generation Mining is a sponsor of this website and there will always be some bias. Yet it will be very difficult to find a palladium project out there in a Tier-1 mining jurisdiction that isn’t just very profitable at $1275 palladium (with a payback period of 2.5 years and an IRR of 30%) but also works at $900 palladium (with an IRR of just below 20% and a 4 year payback period). The Marathon PGM project obviously won’t be built should the palladium price retreat to less than $1000.oz, but the sensitivity analysis in the preliminary economic assessment shows the resilience of the project. Marathon appears to be one of the best-advanced stage PGM projects that could actually be built this decade.

Disclosure: The author holds a long position in Generation Mining. Generation Mining is a sponsor of the website.