The world population is increasing, and all of those people will have to be fed. Back in the 2000’s, it became clear the world wasn’t prepared for feeding an additional several billion of people within the next decade, and a ‘rush to fertilizers’ began. If you can’t expand the farmlands, the only other solution would be to become more efficient, and that’s why the entire commodity sector started looking at the production of fertilizer to increase the efficiency of the farmers and thus increase crop yields.

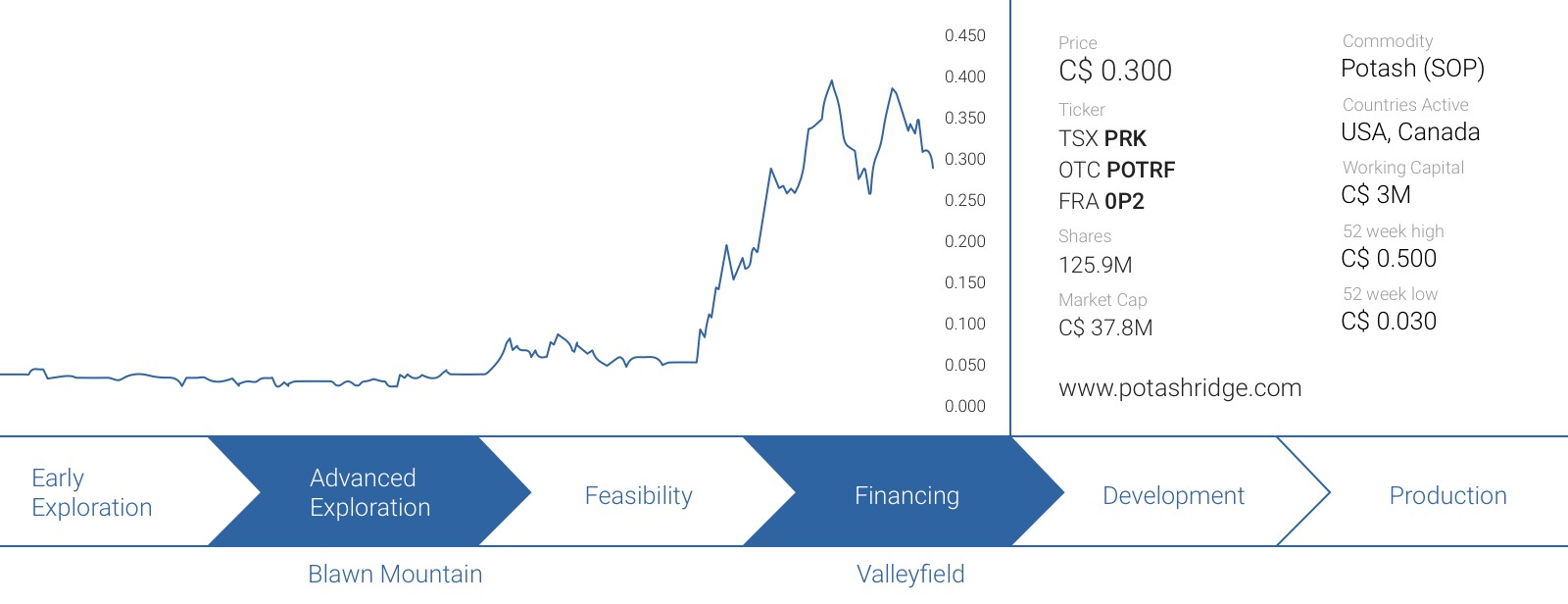

In this report we will explain why not all kinds of potash have been created equal, and why it’s not that easy to find a good producer of Sulphate of Potash (‘SOP’) whereas there seems to be an oversupply of the ‘normal’ potash (hereafter: Muriate of Potash or ‘MOP’). Potash Ridge Corp (PRK.TO) is aiming to become a dominant producer of SOP in North America, and is trying to reach that status by using a two-pronged approach. It will first start a relatively small Mannheim plant in Québec, becoming the first producer of SOP via the Mannheim Process in North America. This offers a pathway to production with relatively low Capex (less than $60M) and short pay back period. Simultaneously, they will advance one of the largest undeveloped SOP projects, in Utah, with a phased development approach vs a larger upfront Capex.

This project, Blawn Mountain, has the potential to be the lowest cost producer of SOP in the world, as the production cost is expected to be just $180/t whilst the all-in cost should remain limited to less than $250/t. This indicates Blawn Mountain could have a huge operating margin of in excess of $500/t!

What is SOP and why is it important to distinguish it from MOP?

The market does use the word ‘potash’ for both SOP and MOP (as both are potassium-based fertilizer products), but there’s a huge difference between both kinds of potash. It’s pretty easy to find and mine MOP, and even though the initial capex for most large MOP mines is pretty high (usually in excess of $1B and very often $2B+), the world currently is in an oversupply situation as a lot of new MOP projects were started during the Potash-boom, when the MOP price reached a price level of almost $1000/t.

The MOP producers were printing money back then, but the over-investment in the sector is now coming back to haunt them. That’s why we’re not particularly interested in a mainstream product that currently is in an oversupply situation. But as we said in the introduction, not all kinds of potash have been created equal and even though the MOP market is in a huge oversupply situation, virtually no new SOP projects (Sulphate of Potash) have been brought into production, despite a continuously increasing demand.

Sulphate of potash consists of potassium and sulphur, and that’s a highly sought after combination for several crops that can’t deal with the high chloride levels in MOP. Think about tomatoes, nuts, … . All these products can only handle SOP as fertilizer product. Of course, the total market of SOP is much smaller compared to MOP (the annual market for SOP is approximately 5M tonnes per year versus 55 million tonnes per year in the MOP market), and that’s exactly what might cause a SOP supply deficit as the demand is continuing to increase. But what’s even more important is the fact the North American market is currently being served by just one supplier, and the lack of real competition might put Potash Ridge on the map right away.

Valleyfield will host the first SOP plant – explaining the process

So you have MOP in an oversupply situation whilst the SOP market is running a very tight ship and seems to be heading towards a supply deficit, which really emphasizes the business case for Potash Ridge. Valleyfield, named after the location in Québec just 50 kilometers from Montréal where the plant will be built, most definitely will be an interesting project for the company considering it will use the Mannheim-process to convert the (currently) dirt-cheap MOP into SOP.

This might sound like alchemy, but the process and procedure is actually pretty straightforward. You need just two inputs in the plant (MOP and sulphuric acid), which could then be converted into two end products, Sulphate of Potash (SOP) and Hydrochloric acid (HCl). And that’s where the first tumble block comes to light. Not just any company can build a Mannheim plant, as the hydrochloric acid as by-product is something that has to be taken care of and that’s not always simple, considering hydrochloric acid is quite a dangerous product as it’s corrosive to the skin and eyes and causes burn wounds.

And the Mannheim process isn’t exactly rocket science, considering this process has been used for in excess of a century, and almost half of the current world production of SOP is being generated with this Mannheim process. Several other companies have done this before (with for instance Tessenderlo Chemie (EBR: TESB) as one of those existing SOP producers).

The first economic study was positive, but there’s more

Potash Ridge has engaged SNC Lavalin to look at all possibilities for the SOP plant in Valleyfield, and SNC has created an economic model to find out whether or not a plant would make sense. The study has not been released to the public as Potash Ridge chose to just release a brief summary of the study, but the short summary contains a lot of valuable information about the viability of this project.

SNC estimated Potash Ridge should be able to build a 40,000 tonnes per year operation for a total capex of less than C$50M (and yes, this number does include the hydrochloric acid and sulphuric acid equipment), of which approximately 20% would be contributed by third parties. Based on SNC’s assumptions, the after-tax NPV10% of the project would be C$67M.

Fine, great. The company’s market capitalization currently is approximately C$37M so you’d indeed assume Potash Ridge is now fully valued based on the NPV of the Valleyfield project. That being said, we do see a lot of ‘hidden value’ in Potash Ridge. Not only do you also get exposure to the large scale Blawn Mountain mine project, we also think SNC has used quite conservative assumptions in its economic study. It used an SOP price of US$760/t and a MOP price of $380/t, whereas both prices are now approximately $800/t and less than $250/t (Potash Corp of Saskatchewan (POT) even sold potash for less than $200/t at the end of last year which means the input price of MOP is very conservative).

On top of that, a discount rate of 10% is also pretty conservative in the current low-yield environment. We would prefer to use a 5% or 6% discount rate which is more appropriate for a project in Québec, as the political risk is close to zero. After all, if Lundin Gold (LUG.T) gets away with using a 5% discount rate in Ecuador, there’s no reason why we can’t apply the same rate for a Québec based operation.

Using these updated inputs, the after-tax NPV10% changes completely. Assuming a total tax pressure of 35% and an accelerated depreciation schedule in the first five years, assuming an MOP price of C$350/t, a processing cost of C$125/t and an SOP price of C$1050/t, the after-tax NPV5% comes in at C$94M, using an initial 12 year ‘plant life’ and a sustaining capex of C$2M per year. Keep in mind these are our own back-of-the-envelope calculations to show how the economics of Valleyfield change when you’re using different parameters.

That being said, as Valleyfield will be an industrial project with a theoretical perpetual operating life (mines can be depleted, but as long as Potash Ridge can buy MOP, it can continue to operate the plant for generations to come), it could also make more sense to use an NPV calculation based on perpetual cash flows, which would result in an after-tax NPV5% of approximately C$260M (using the normal free cash flow run rate of C$13M per year (as the formula is the after-tax free cash flow divided by the discount rate) or an after-tax NPV8% of C$163M.

Blawn Mountain is the icing on the cake

Valleyfield will be Potash Ridge’s first operating site and allows the company to aim for a positive free cash flow within the next 18-24 months. That’s very nice, but PRK has another ace up its sleeve with the Blawn Mountain project in Utah, USA.

This project contains a large SOP resource and unlike the production plans at Valleyfield where the SOP will be ‘created’ by converting MOP and natural gas into SOP and Hydrochloric acid, Blawn is a ‘normal’ mining project where the SOP can be scooped out of the ground without the need for any additional external process.

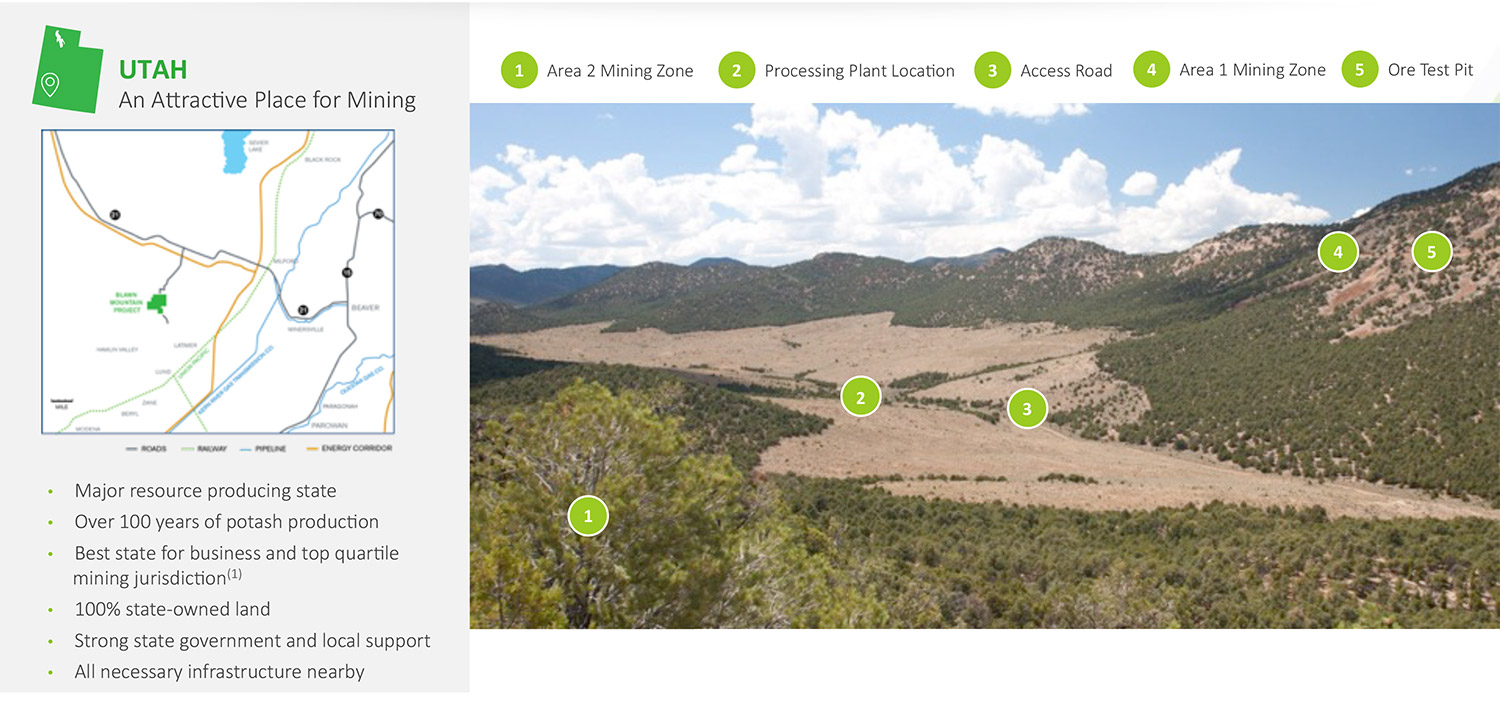

The project consists of in excess of 15,000 acres of state land, approximately 50 kilometers southwest of Milford and pretty close to the border with Nevada. Earth Sciences discovered the project in the late sixties during its quest to find more aluminium properties. But as the potash price was quite low, ESI didn’t bother to follow up on the discovery, despite having drilled in excess of 300 holes and the exploration results from these holes were confirmed by an additional 90 holes drilled by Potash Ridge.

Blawn Mountain is a ‘real’ mining project, and the PEA which studied a base case mining scenario to produce 645,000 tonnes of SOP per year estimated the initial capex at US$1.1B (with an additional $160M to be spent as sustaining capex). What’s really interesting here is the fact Potash Ridge will be able to sell the sulphuric acid as well, which reduces the direct operating cost to US$112/t, and the total cash production cost would come in at $218/t (with an average AISC of $230-235/t). As far as we know, this makes Blawn the lowest cost SOP mine in the world.

This study indicated an after-tax NPV8% of $1.5B using an SOP price of $649/t (on an FOB basis at the mine gate) which is pretty darn good, but as you can imagine, the initial capex of $1.1B is the main hurdle here. That’s the main reason why Potash Ridge is currently investigating the possibility to get Blawn Mountain going as a ‘staged’ project to reduce the initial capex, whilst increasing the annual output by continuously increasing the mining rate.

Conclusion

Potash Ridge could be seen as a two-step rocket as its first pillar is based on quick cash flow from a Mannheim-based SOP plant in Québec which could produce up to 40,000 tonnes of SOP per year. The cash flow generated in Québec will help Potash Ridge to develop the massive Blawn Mountain project which could supply in excess of 10% of the current world demand for SOP, at a very low all-in cost of less than $250/t, indicating the operating margin could very well be $500/t.

We are looking forward to see Potash Ridge securing the final permits for the Valleyfield project and if the permitting process could indeed be completed by the end of this year, the short 12 month construction period should allow Potash Ridge to be free cash flow positive in 2018, where after it will also be able to start thinking about increasing the production rate at Valleyfield, considering the project is scalable.

Potash Ridge Corp. is a sponsor of the website, we hold a long position. Please read the disclaimer