Although we are getting close to wrapping up the second quarter of the year, we think it’s perhaps a good opportunity to take a moment and have another look at Heliostar Metals’ (HSTR.V) results for the first quarter of the year. As the company is strongly cash flowing at the current strong gold price, Charles Funk and his team are in an excellent position to continue to unlock value at Heliostar. The existing assets, recently acquired assets and potential new acquisitions will allow Heliostar to keep its pipeline filled.

In a previous update that was published in April, we reviewed the company’s acquisition of the Goldstrike project in Utah so we won’t spend that much time on that acquisition and project. Instead, we will focus on the cash flow generated by the operating assets and explain why a gold price of $4500/oz or $4000/oz has no material impact on the Heliostar thesis.

A quick review of the Q1 results

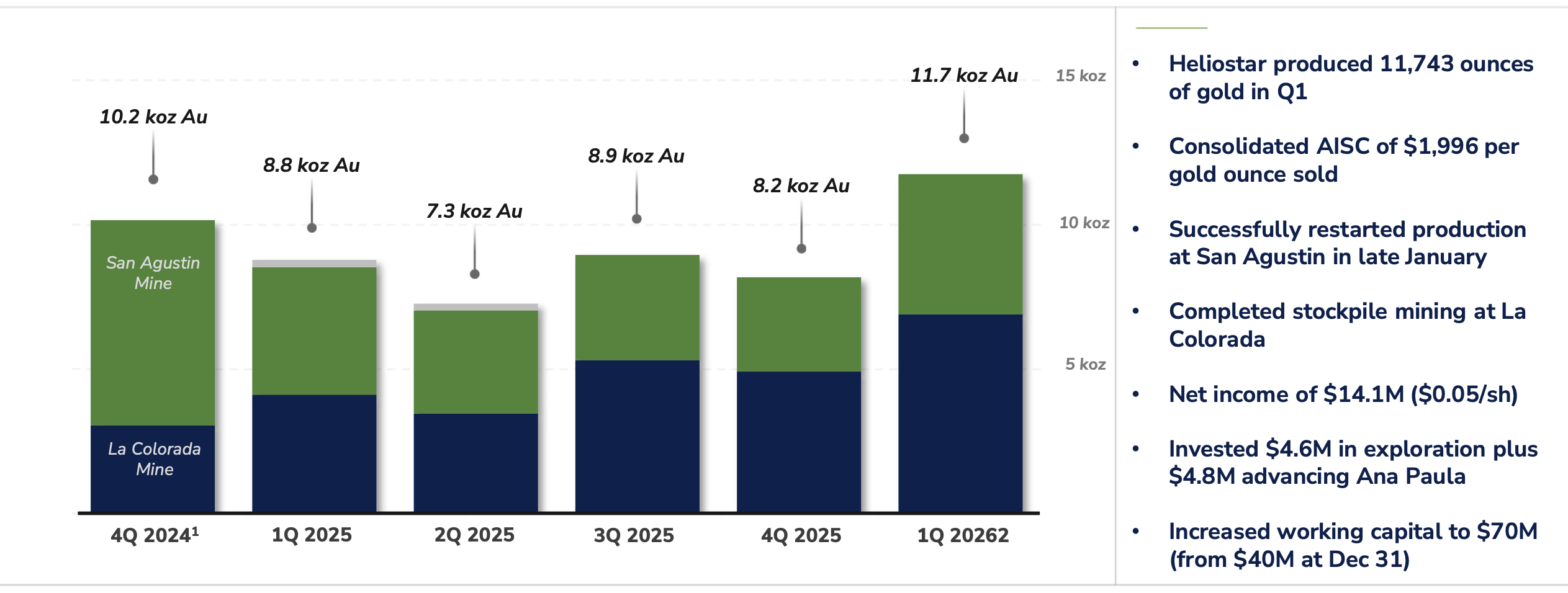

In the first quarter of this year, Heliostar Metals produced just under 11,750 ounces of gold, in combination with almost 44,000 ounces of silver. Unfortunately a substantial portion of the production was not sold during the quarter (only 9,980 ounces and 10,610 ounces respectively were sold), with the remainder held in inventory (and those ounces were likely sold off in the first few weeks of the current quarter). The company’s strong balance sheet allowed it to avoid selling metal into the brief downturn in metal prices near the end of the Q1.

As anticipated, the cash cost and the all-in sustaining cash costs decreased versus the one time high costs in Q4 to bring San Agustin online. They’re now at a more reasonable level of just under $2,000/oz on an AISC basis. The main driver of the production (and operating expenses) was the La Colorada mine in Mexico’s Sonora state which where Heliostar operates a 12,000 tonnes per day plant. These operations yielded 6,900 ounces of gold at an AISC of $1,703/oz with San Agustin providing the balance of the production. At San Agustin, the total production was 4,853 ounces of gold of which just over 4,400 ounces were sold at an AISC of $2170 per ounce sold.

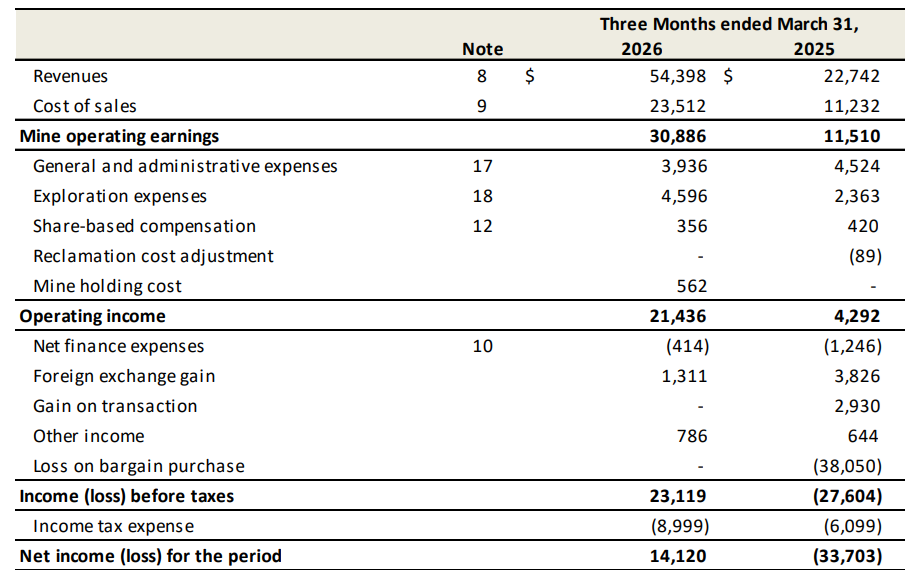

This resulted in a total generated revenue of US$54.4M and mine operating earnings of just under US$31M (it goes without saying that due to the low-cost nature of these projects, the margins are very good). The reported operating income was $21.4M and looking at the bottom line result, Heliostar reported a net profit of $14.1M or US$0.05 per share. At the current exchange rate, this represents approximately C$0.07 per share.

Two key elements to isolate from the income statement. First of all, the bottom line result included $4.6M of expensed exploration. Rather than capitalizing the exploration efforts, the company elected to expense them. There’s something to be said to expense the $3.3M that was spent on Cerro del Gallo, Unga and San Antonio, but it is interesting to see the $1.3M in exploration expenditures on the producing assets was expensed and not capitalized. While these assets are producing, the exploration efforts here were focused on new, incremental resource targets that still need to be worked into a future mine plan. The infill drilling at Ana Paula was expensed as the company is de-risking ounces already planned to be put into production (as shown in the PEA)

Secondly, the low operating expenses include a $5.8M contribution from changes in inventories from the one time sale of gold bearing carbon fines that had built up through 2025. While this did have an impact, we should not exaggerate that impact, especially given it’s approximately the same magnitude as the expensed exploration efforts. If you would remove both from the equation, the bottom line result would not be materially different.

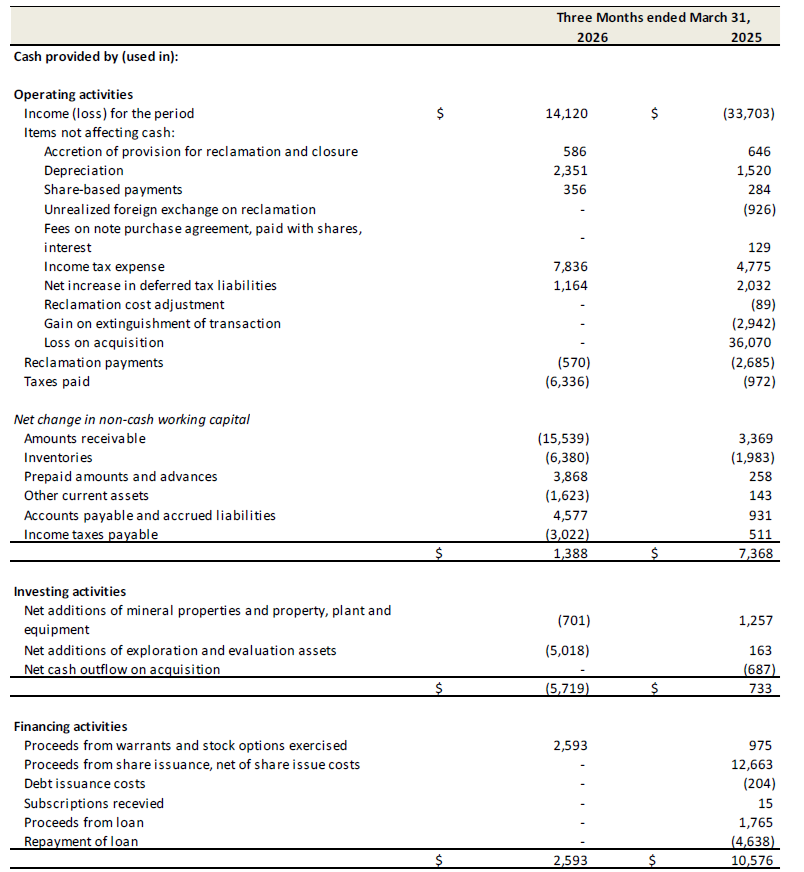

Given the very low-capex nature of the two existing mines, we were expecting Heliostar to continue to generate a substantial amount of free cash flow. While the reported operating cash flow (shown below) is just $1.4M, keep in mind this is entirely related to a build in the working capital position. There were a large number of ounces sold right at the end of the quarter for which cash had not yet been received by March 31st – about $11M worth. There was a net cash outflow of $18M that was invested in working capital elements, including $3M in taxes paid that were not owed based on the H1 results. And it goes without saying we should see a reversal of the working capital cash flows next quarter as for instance the increased amount of receivables will be converted in hard dollars.

The main takeaway: on a normalized basis, and excluding the impact of changes in the working capital (which we expect to be reversed anyway), the operating cash flow was $19.4M of which $0.7M was required for capital expenditures and an additional $5M was spent on capitalized exploration at Ana Paula.

So if you would take the capitalized exploration into consideration as well, Heliostar generated approximately $13.5M in net free cash flow, (which is approximately C$18.5M using the current exchange rate). And keep in mind this includes almost US$10M (C$13.5M) in exploration efforts which should add value to the existing assets.

The net cash didn’t increase (due to the aforementioned investments in working capital items) but the working capital position increased to approximately US$70M (about C$95M using a fixed exchange rate of 1.35 CAD per USD, and slightly higher at the current exchange rate of 1.42 CAD per USD).

La Colorada Exploration Targets

Despite the lower gold price, Heliostar will still provide superior cash flow

While the Q1 results were achieved based on an average gold price of $4750/oz, even at the current lower gold and silver prices, we would continue to see a very robust earnings and cash flow profile. After all, keep in mind a low single digit percentage of the gold and silver production was not sold during Q1 and thus was not included in the revenue calculation.

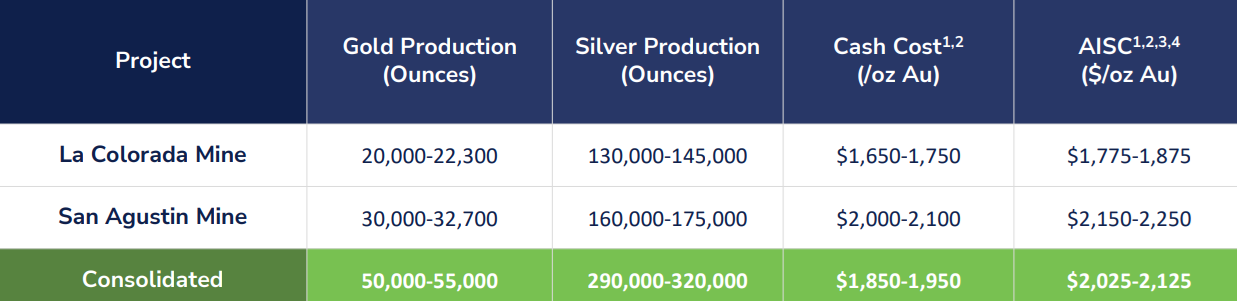

Let’s take a step back and have another look at the official guidance for this year.

As indicated above, the company plans to produce 50-55,000 ounces of gold and 290-320,000 ounces of silver at an anticipated AISC of $2025-2125 per ounce of gold (keep in mind a higher silver price compared to the company’s budget price of $47.50 will have a positive impact on the all-in sustaining cost per ounce of gold as the by-product revenue will come in higher). While the difference between a realized gold price of $4750/oz and $4000/oz will certainly make a difference, the main takeaway however is that Heliostar will still be hoarding cash thanks to its operational assets, and that cash will provide the required equity component (or at least a substantial part of the equity component) of its future growth projects.

The anticipated capex to lay back the La Colorado open pit can easily be covered by the current cash position, and future cash flows will only add to that cash pile. The Ana Paula initial capex is estimated at US$300M as per the November 2025 PEA, so assuming a 40/60 equity/debt financing structure would require Heliostar to put up US$120M in equity (read: retained earnings and available cash).

Ana Paula also has the potential to triple the company’s production rate, with an even higher torque on the cash flows (Ana Paula will produce twice as much as the two current operational mines, at an AISC that will be about 40-45% lower than what Heliostar is currently spending to produce an ounce of gold).

And then you are off to the races. Suddenly, with Ana Paula in production (and assuming the numbers from the 2025 study can effectively be achieved), Heliostar will be producing 150,000 ounces of gold at a blended AISC of $1500-1750/oz. Even if the AISC comes in at the higher end of that range, and even if gold retraces back to $3500/oz, the net margins (on a pre-tax and pre-overhead basis) would still be about $1750/oz, for a net cash flow of US$250M per year on the mine level. And even after deducting taxes and interest payments, Heliostar would still generate a triple digit amount of net free cash flow per year. And that’s what will fuel the next growth steps.

Heliostar started out as a three-step rocket with La Colorada, San Agustin and Ana Paula (subsequent to acquiring the Mexican assets after Ana Paula), but has evolved into what now appears to be a five-step rocket, where every milestone that is achieved will boost the next phase of the company’s growth profile.

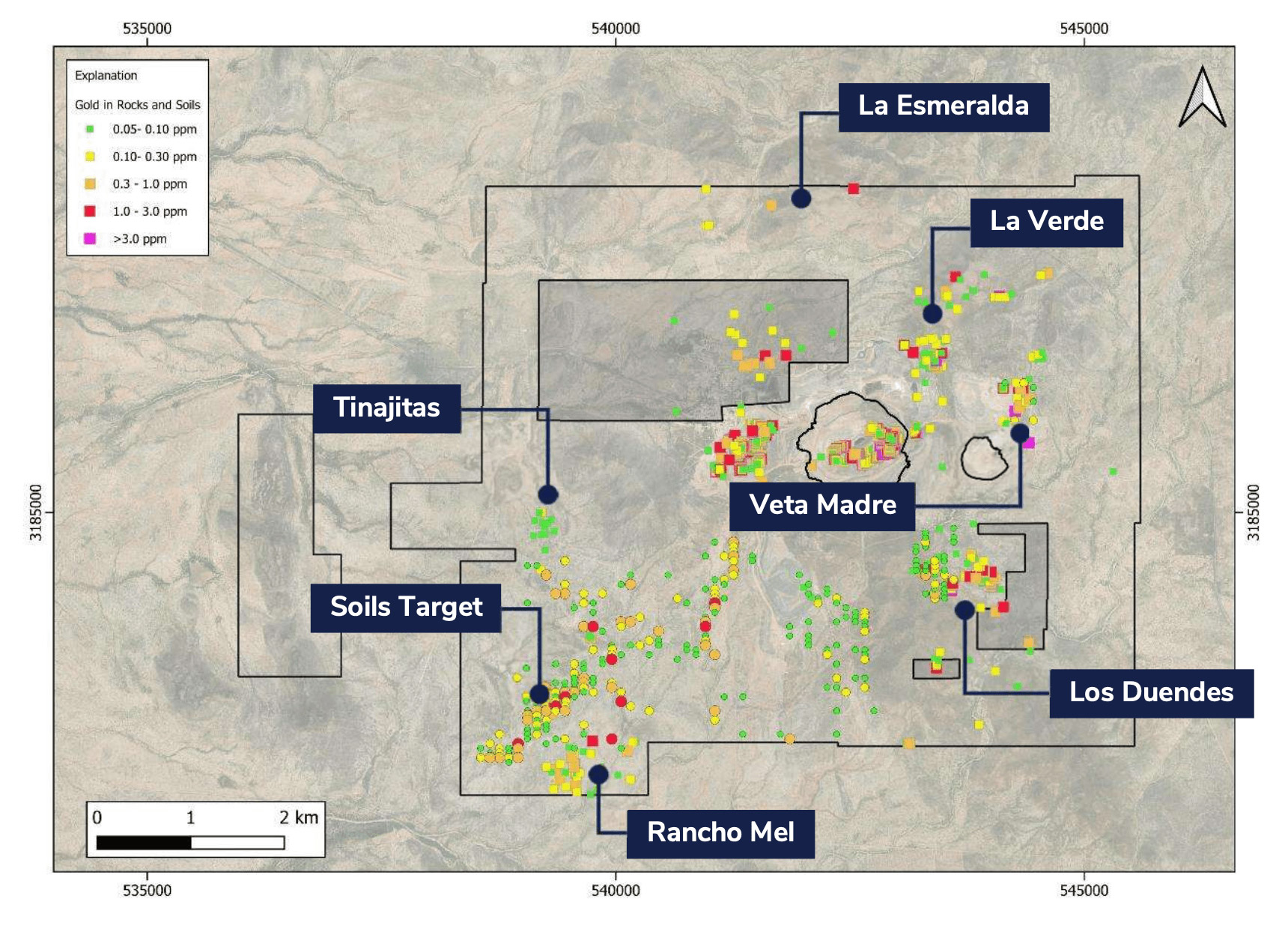

The Veta Madre pit expansion will boost the output at La Colorada

Last week, Heliostar Metals also announced it received the final documentation for the change of use of soils permit for the Veta Madre pit expansion at its La Colorada Mine. This approval comes on top of the environmental permits for the pit expansion and the leach pad expansion already granted. The newly issued permits and approvals support both the current design of the open pit but would also be valid for the potentially larger Veta Madre Plus pit.

Heliostar recently also completed in excess of 8,400 meters of drilling in 44 holes focusing on the Veta Madre resource and reserve and stepping out into new areas around the existing pit. Not only did the drill program intersect higher grade mineralization within the current Veta Madre reserve pit pushback, it also encountered mineralization that could see the pit expand even further to the South (this would be the Veta Madre Plus pit mentioned in the previous paragraph). Some of the higher grade results can be found in the bullet points below.

- Veta Madre drilling:

- 10.9 m grading 22.1 g/t gold from 187.7 m, including 1.3 m grading 174 g/t gold

- 40.8 m grading 2.23 g/t gold from 51.3 m, including 17.45 m grading 4.55 g/t gold

- 147.2 m grading 0.70 g/t gold from 32.65 m, including 10.7 m grading 1.98 g/t gold

- 20.65 m grading 3.35 g/t gold from 337.4 m

- 32.0 m grading 1.65 g/t gold from 52.5 m

- 52.35 m grading 1.23 g/t gold from 50.3 m

- Significant intervals of mineralization outside of the current Veta Madre reserve pit

- Final approvals for Veta Madre pit expansion received from the Mexican permitting agency

- Engineering of Veta Madre Plus pit is ongoing with waste stripping on track to start in early Q3 2026

The company is now working on an updated resource model at Veta Madre and engineering of the larger Veta Madre Plus pit.These updates will include the recent drill results as well as the higher gold price since the previous resource and technical report was issued. The updated model will not be published in a new technical report, but the impact of the expanded pit and mineralization will become evident in the company’s 2027 (and potentially 2028) guidance. As pre-stripping activities are expected to start in the next quarter, Heliostar Metals will have a pretty good idea on its timelines by the time the 2027 guidance will be released.

Further growth opportunities

And although the company’s asset development pipeline is already quite well filled, Heliostar continues to be on the lookout for opportunities as it does have the right team in place and sufficient financial firepower to advance projects.

With the recent acquisition of the Goldstrike project in Utah, Heliostar has clearly shown it is willing to take on this type of development project outside of Mexico as well.

And we believe this will be the main value creating engine of the company as despite seeing a gold price that remains strongly above $4000 per oz, this type of projects are still available at a very reasonable cost with plenty of opportunity for the company’s technical team to add value. However with an already robust development project pipeline that stretches well into the 2030s, we expect the company to focus more on adding production assets.

Conclusion

When Heliostar acquired the Ana Paula project as its flagship asset, it was an interesting story. Adding two operating assets to the project mix has changed the picture pretty drastically considering both assets are generating more cash flow than Heliostar can currently spend. This will allow the company to strengthen its balance sheet by adding cash to its treasury ahead of its next (wave of) development efforts.

From a financial perspective, the company has never been in such good shape. Which means Heliostar now is an ‘execution’ story.

Disclosure: The author has a small long position in Heliostar Metals. Heliostar Metals is a sponsor of the website. This post is for educational purposes only; be mindful investing in junior mining stocks is risky and you may lose your entire investment if things go wrong. Please read our full disclosure.