At the end of March, Cameco (CCJ, CCO.TO) confirmed it was shutting down its Cigar Lake uranium mine in Saskatchewan’s Athabasca Basin due to the COVID-19 virus. Cameco pledged to pay its employees their normal salaries during the shutdown (which is a nice thing to do) for the entire (initial) four week shutdown of the mine. Before shutting down the mine, Cameco discussed the steps it was planning to take with Orano Canada (ex-AREVA) which operates the McLean Lake mill where the uranium mined at Cigar Lake was being processed.

This has an important implication for the uranium market and the (lack of) an equilibrium. Cigar Lake produces almost 20 million pounds of uranium per year and if we would now assume a total shutdown for a month and a timely reopening and 1-month ramp-up to the normalized production volumes (highly doubtful, but okay) producing just half of the normal volumes, the 1.5 month production loss would equal approximately 3 million pounds (again, that’s assuming the mine will indeed be reopened in 4 weeks and ramping up the operations goes well).

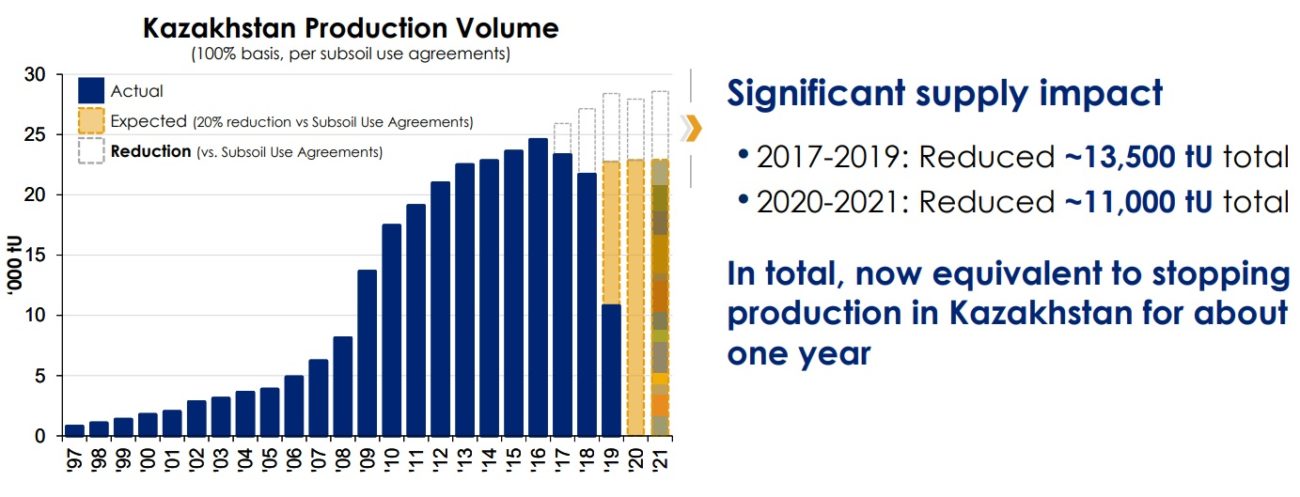

Cigar Lake was just one of the domino pieces that fell over the past two weeks; earlier this week, Kazatomprom (KAP.L) announced it would reduce the production rate by up to 4,000 tonnes this year (approximately 8.8 million pounds) which brings the combined output reduction to almost 11 million pounds. And these two mines aren’t the only ones taking measures as the Namibian mines (Rossing, Husab and Langer Heinrich) were shut down by the government due to the COVID-19 virus.

We almost don’t dare to say it out loud anymore after having been wrong numerous times. But the perfect storm that’s currently hitting the uranium market could finally get things moving. On the one hand, the demand remains stable as nuclear reactors are essential parts of society’s energy needs and won’t be shut down for just a few weeks while on the other hand the supply is dropping fast, further increasing the gap between primary supply of uranium and the demand. In Q2 2020, approximately 12-15 million pounds of uranium will be removed from the supply side of the market, and that’s an additional 12-15 million pounds that utilities will have to draw down from the existing inventories thereby accelerating the depletion of said inventories.

This could be the prelude of Uranium’s day in the spotlight, and even companies in the exploration stage could benefit from renewed attention for the uranium sector. Skyharbour Resources (SYH.V) should have wrapped up its drill program (announced on February 13th) by now and we are expecting to see assay results by the end of the month. As you may remember from our previous report on Skyharbour (which you can re-read HERE), its two joint venture partners on two other properties should also be in a position to release news. Azincourt Energy (AAZ.V) also completed a drill program while Orano Canada also started exploration activities in March in preparation of a potential drill program next winter.

Disclosure: The author has a long position in Skyharbour Resources. Skyharbour is a sponsor of the website.