At our most recent visit to the PDAC conference in Toronto (and some smaller conferences right before the PDAC started), we had the impression more companies are now focusing on copper as their new main commodity. Unfortunately we failed to see any new advanced stage copper stories (most were early stage exploration companies), and this reconfirms Kutcho Copper (KC.V) is in an excellent position to take advantage of the increasing copper deficit in the world.

The anticipated resource update has now been published, and Kutcho should be publishing the results of its feasibility study in the next few months, establishing itself as a near-term copper developer.

The resource update is excellent news

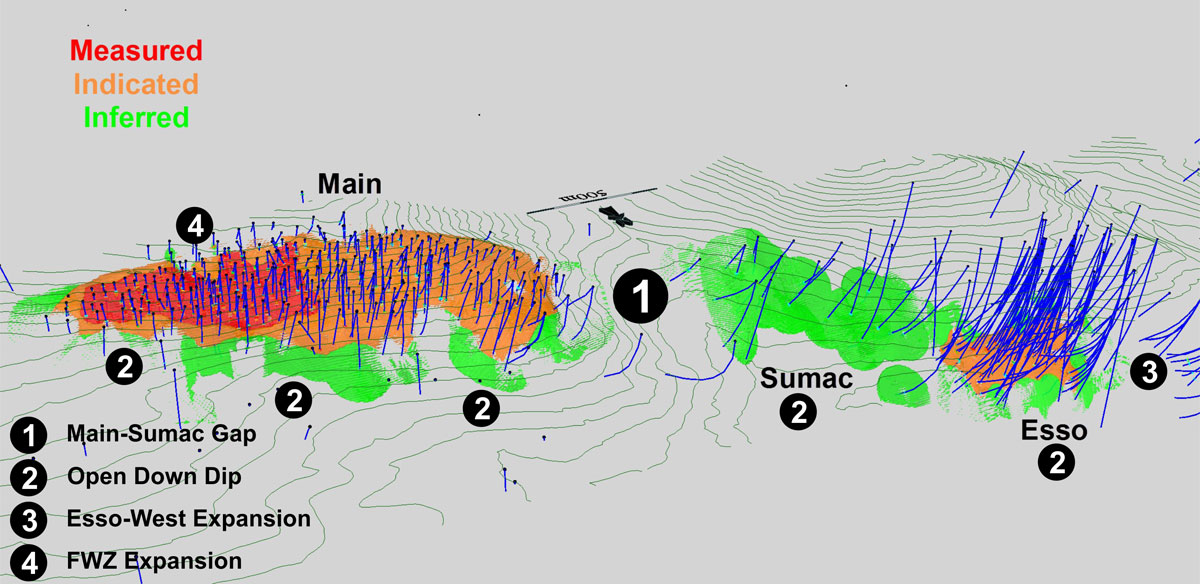

Kutcho Copper has now put all the drill data from the 2018 exploration program in a new geological model, and this resulted in an updated resource estimate that now contains 28 million tonnes of mineralized rock, of which 17.3 million tonnes (just over 60%) is part of the measured and indicated resource categories.

The Main Deposit remains with a total resource of almost 17 million tonnes, with 85% of those tonnes in the measured and indicated resources. With an average grade of 1.74% copper, 2.38% zinc, 0.43 g/t gold and 29 g/t silver, the Main zone will be the ‘moneymaker’ for Kutcho Copper as this deposit will also host the vast majority of the reserves. Kutcho Copper’s 2018 drill program did a good job in increasing the confidence in the geological model as the orebody at the Main zone seems to be very contiguous and continuous, making the planning of the mining activities a bit easier and more efficient.

The higher amount of tonnes in the resource estimate will very likely also have a positive impact on the reserves of the mine, and the corresponding mine life. In the pre-feasibility study, approximately 62.5% of the measured and indicated resources were converted into a probable reserve, however, this was predominantly due to the fact that Kutcho was able to increase the total resource by lowering the cutoff grade, but the company had to leave the reserve statement unchanged which reduced the conversion percentage. After the recent drill programs and the interim update on the metallurgical test work, we would anticipate this percentage to increase as more tonnes will be brought in the mine plan. If we would use a conversion ratio of 80% which would be a more reasonable and realistic conversion percentage (considering Kutcho will be able to tap into the entire measured and indicated resource to calculate the reserves), we think it’s reasonable to see 14 million tonnes of reserves in the mine plan. That would be a 30-35% increase compared to the mine plan in the pre-feasibility study.

What about the inferred resource?

Additionally, the inferred resource (10.7 million tonnes at an average grade of 1.67% CuEq) won’t be part of the feasibility study (only reserves will be considered for the mine life), and could provide additional tonnage to ‘feed the mill’ by expanding the mine life of the mine. At a production rate of 3,500 tonnes per day, every additional 1.3 million tonnes that could be brought in the mine plan would keep the mill going for an additional year, and it will be up to Kutcho’s technical team to figure out which zones could meet the minimum criteria to be mined.

An average grade of 1.67% CuEq does sound low, but there will be higher grade and lower grade zones in that inferred resource, and some parts could be viable. If we would use the parameters used by the company to determine its cutoff grade ($34/t mining, $18/t processing and $10/t in G&A) and the applicable recoverable and payable ratios of the commodities, the 1.67% CuEq would have a recoverable value of US$100-105/t while it would cost Kutcho approximately $62/t to mine and process the rock. And just to put your mind at ease: Kutcho Copper has been using a 1.2% copper-equivalent grade as cutoff grade.

Mining stuff with an average grade of 1.67% CuEq won’t make Kutcho Copper much money, but once all initial capex has been recouped it could make sense to keep the mine open for as long as feasible. If anything, milling a few years of low-grade material towards the end of the mine life could help Kutcho to fund the closure costs.

A quick look at the 2017 pre-feasibility study

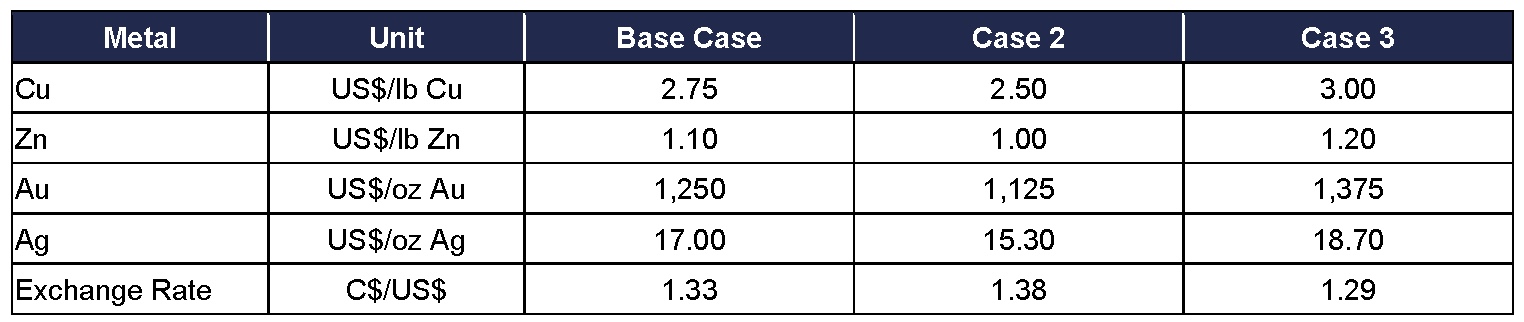

And let’s have another look at that pre-feasibility study. Kutcho Copper’s base case used a copper price of $2.75/pound, a zinc price of $1.10/pound and prices of $1250 and $17 per ounce of gold and silver. A conservative approach and given the strength of the copper market lately, a case could be made to have a closer look at ‘Case 3’ which incorporates a $3 copper price and a $1.20 zinc price.

The gold and silver prices are currently substantially lower than in the company’s scenario but considering only 124,000 ounces gold and 11.6 million ounces of silver were expected to be recovered in the pre-feasibility study and considering the deal with Wheaton Precious Metals whereby WPM will purchase 2/3rd of the gold and silver at a substantial discount, the precious metals prices won’t matter that much, as we should apply a discount on the PM revenue anyway.

Metal Price Assumptions – Source: JDS 2017

Metal Price Assumptions – Source: JDS 2017

So, based on the inputs of ‘Case 3’, the after-tax Internal Rate of Return is estimated at 31%, while the after-tax NPV8% would increase to C$316M. Keep in mind this is based on an USD/CAD exchange rate of 1.29, and applying the current spot USD/CAD exchange rate of 1.33 would increase the after-tax NPV8% to C$325M.

And again, this is based on the parameters used for the pre-feasibility study. With a larger resource estimate and a plan to increase the daily throughput, the IRR and NPV will very likely change a bit, but this should have a positive impact on the economics.

The next steps: met work and the feasibility study

Now the resource estimate has been completed and Kutcho’s consultants are working on a mine plan and the corresponding mine reserves, the next catalyst will be the completion and publication of more detailed metallurgical test results. Kutcho has already provided an interim update on this metallurgical test program which appears to confirm the potential to further improve and optimize the recovery rates.

According to the interim update, using a simplified reagent suite could cut the initial capex and the operating costs per tonne, but result in the same recovery rate and concentrate quality as used in the base case scenario in the pre-feasibility study. Additionally, it looks like the new flow sheet is successful in removing as much zinc from the copper concentrate as possible, which indicates more zinc will report to the zinc concentrate. This should have a (small) positive impact on the amount of payable pounds of zinc which could help to reduce the production cost of the copper due to a higher by-product revenue. The final results of the metallurgical test work should be released later this quarter, but we hope to see some more interim updates.

The results of the metallurgical test work will obviously be incorporated in the feasibility study, which should be published in the third quarter of this year. Considering the pre-feasibility study was completed by respectable firms, we don’t anticipate seeing any issues in the definitive feasibility study.

Of course, some things will change as Kutcho Copper will very likely increase the daily throughput from 2,500 tonnes per day in the PFS as the larger resource (which will very likely also result in a larger reserve) does warrant an ‘upgrade’ to 3,000 or 3,500 tonnes per day. This will result in a higher capex but should have a small positive impact on the operating cost per tonne as well, while the production increase will make Kutcho a more meaningful copper and zinc producer making the potential offtake parties even more interested in securing the concentrate.

The copper market: a brief update

Brokerage firms usually provide a macro-economic update on a quarterly basis so we will probably have to wait until April before seeing their updates, but we would like to take a minute to review the take of Canaccord Genuity and Haywood Securities on the copper market in general.

In its outlook for 2019, Canaccord remains very bullish on the future of copper. Acknowledging 2018 was a lost year (the copper price fell by almost 20% during calendar year 2018), Canaccord pointed out the physical market encountered a shortage of refined metal despite ‘a moderating Chinese demand and robust mine supply’ and that has now been confirmed by the International Copper Study Group which released its own report at the end of February.

In that report, the study group had a look at the refined copper production and consumption levels in the first xxeleven months of 2018 (the full-year overview should be published soon). It confirmed Canaccord’s findings as the ICSG estimated the refined copper production to have increased by 1.5%, but this wasn’t sufficient to keep up with the increasing demand for refined copper products, as the demand increased by 2.2%.

The higher demand was exclusively caused by China which saw its import levels of refined copper increase by 20%, probably due to the lack of availability of scrap material inside the country. The 5.5% higher copper demand from China actually compensated for the 1% demand decrease for refined copper products in the rest of the world. So let’s not kid ourselves, the copper market is still very much focused on the Chinese consumption levels of the base metal.

And indeed. Going back to the numbers published by the International Copper Study Group, there was an anticipated deficit of 395,000 tonnes of copper (almost 900 million pounds) in the first eleven months of 2018. This number appears to be realistic as the inventory levels (shown on the previous image) fell by that approximate amount of tonnes as well…

Long story short; we tend to agree the situation on the copper market deserves some attention, and smelters should get increasingly interested in securing a steady and reliable supply of copper concentrate to keep their facilities up and running.

And that’s all Kutcho Copper could ask for: the world clearly needs additional sources of copper and with an advanced stage project in British Columbia – which means the concentrate won’t have to travel too far to reach its probable destination (China/South Korea/Japan) – Kutcho Copper is in an excellent position to negotiate offtake agreements for its different concentrates.

Conclusion

During the last PDAC conference earlier this month, we noticed how several companies are trying to ‘rebrand’ themselves as copper companies, and we noticed the majority of those companies are focusing on early-stage projects that still have to go fully through the ‘discovery’ phase. Most of the new ‘copper hopefuls’ don’t even have a resource estimate and may miss the cycle.

That’s why Kutcho Copper has a clear advantage over most other copper companies. Now that the resource has been updated, its consultants can get working on building the new mine plan that will culminate in the publication of a feasibility study (which should be ready by in the third quarter). Considering the pre-feasibility study in 2017 already shows the excellent economics of the Kutcho copper project, we expect the feasibility study to be in line with those findings: a healthy Net Present Value and a robust Internal Rate of Return at a copper price of $2.75-3.00 per pound. That’s all we ask for.

Disclosure: Kutcho Copper is a sponsoring company. We have a long position. Please read the disclaimer